Learning Outcomes

This article outlines ordinary partnerships under the Partnership Act 1890, including:

- The statutory definition and core characteristics of an ordinary partnership, and how to identify when a partnership exists as a matter of fact.

- The consequences of unincorporated status and lack of separate legal personality for ownership of assets, contracting, litigation, and granting security.

- The key default provisions of the Partnership Act 1890, their limitations, and how a bespoke partnership agreement can modify profit sharing, management, and exit arrangements.

- The principles governing partner liability for debts and wrongful acts, including joint and several liability, liability in tort, and liability of incoming and outgoing partners.

- The scope of partner authority to bind the firm, distinguishing actual and apparent authority, and the firm’s liability for misapplication of money or property.

- Fiduciary duties and statutory duties owed between partners, with typical remedies for breach and how these duties are supplemented by contractual terms.

- Practical steps and protective measures on retirement and dissolution, including notice requirements, indemnities, novation, and the application of s 44 PA 1890 to settlement of accounts.

- Common SQE1 examination issues and pitfalls relating to formation, authority, partner liability, and dissolution scenarios.

SQE1 Syllabus

For SQE1, you are required to understand ordinary partnerships under the Partnership Act 1890 and their business and organisational characteristics, with a focus on the following syllabus points:

-

Business and organisational characteristics (partnership)

-

Legal personality and limited liability

-

Procedures and documentation required to form a partnership

-

Partnership decision-making and authority of partners:

- Procedures and authority under the Partnership Act 1890

- Common provisions in partnership agreements

-

Relationship between partners and third parties (agency, authority, and liability under ss 5–18 PA 1890)

-

Practical considerations: tax registration for partners and core accounting concepts for partnerships

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Is a written agreement legally required to form an ordinary partnership?

- What is the term used to describe the liability of partners for the firm's debts?

- Can a partner be expelled from the firm by a majority vote if there is no partnership agreement?

- Does an ordinary partnership have a separate legal personality?

Introduction

An ordinary partnership is formed when two or more persons carry on a business together with the intention of making a profit. This is the definition provided by the Partnership Act 1890 (PA 1890), the primary legislation governing these structures.

Key Term: Partnership

A relationship between persons carrying on a business in common with a view of profit (s 1(1) PA 1890). It is an unincorporated business structure.

The existence of a partnership is a matter of fact. It does not require formal registration with Companies House or even a written agreement. If individuals act in a way that meets the statutory definition, a partnership may be implied by law. Sharing profits is strong evidence of a partnership, although not conclusive (s 2(3) PA 1890).

It helps to break down the statutory definition:

- Relation: partnerships are consensual arrangements founded on contract. Agreements can be written, oral, or implied by conduct. In the absence of an express agreement, the PA 1890 supplies default terms.

- Between persons: “persons” includes individuals and artificial legal persons (e.g. companies). There is no upper limit on the number of partners.

- Business in common: “business” covers every trade, occupation, or profession. Partners must be acting together, i.e. in common, rather than in parallel ventures.

- With a view of profit: there must be an intention to make a profit, even if no profit is actually made. Profit-sharing is prima facie evidence of a partnership, but some profit-sharing arrangements do not create a partnership (e.g. sharing gross returns without joint control, or receiving a share of profits as repayment of a debt or wages).

The PA 1890 includes further guidance (s 2) on circumstances which do not, of themselves, create a partnership, such as co-ownership of property or sharing gross returns without joint control and risk.

Test Tip: In formation questions, focus on the statutory definition in s 1(1) PA 1890 and then use s 2 indicators to test whether the facts really point to a partnership.

Formation and informal creation

Unlike companies or LLPs, ordinary partnerships can be created informally through oral agreement or simply by conduct. This simplicity makes it an accessible structure for starting a business quickly. Partners should still record key terms in writing to reduce ambiguity and avoid reliance on sometimes unsuitable default provisions.

Practical steps to commence trading usually include:

- Opening a firm bank account and agreeing signing arrangements.

- Registering with HMRC as a partnership and ensuring each partner registers for self-assessment.

- Considering VAT registration if turnover exceeds the threshold.

- Agreeing a business name and ensuring compliance with business names regulations.

Unincorporated status and lack of separate legal personality

A significant feature is that an ordinary partnership is unincorporated. It does not possess a separate legal personality distinct from the partners themselves. This means:

- The partnership cannot own property in its own name; assets are owned by the partners.

- Contracts are entered into by the partners.

- Legal actions involve the partners personally, not the firm as a separate entity.

Further implications:

- Partnerships cannot grant floating charges over circulating assets; only fixed charges are possible. This may limit borrowing options when compared to companies and LLPs.

- Goodwill and other intangible assets are owned by the partners collectively in their agreed proportions.

- “Partnership property” is a useful description of assets devoted to the firm’s business but, in England and Wales, ownership vests in the partners rather than a separate legal entity.

Key Term: Partnership property

Property brought into the partnership or acquired for the purposes of the partnership business, which is owned by the partners rather than by a separate legal entity.Exam Warning: Do not confuse an ordinary partnership with an LLP. An ordinary partnership is unincorporated and does not have separate legal personality for these purposes.

Partnership agreements and default rules

While not legally mandatory, a formal written agreement is highly advisable.

Key Term: Partnership Agreement

A formal document setting out the terms of a partnership. It usually deals with the relationship between the partners and their relationships with third parties.

In the absence of an agreement, the default provisions of the PA 1890 apply. These default rules cover profit/loss sharing (equal shares, s 24(1)), management rights (all partners may participate, s 24(5)), entitlement to remuneration (none, s 24(6)), introduction of new partners (requires unanimous consent, s 24(7)), and expulsion (not possible by majority, s 25). These default positions are often unsuitable for modern business arrangements, making a bespoke agreement important.

Common provisions partners include to avoid disputes or undesirable defaults:

- Commencement and duration: a clear start date; confirmation the partnership is not “at will”, and continuation provisions upon retirement, death, or bankruptcy of a partner.

- Capital and drawings: initial capital contributions; whether further capital can be required; drawings policy; interest on capital; and whether any partners receive a “salary” from profits before division.

- Partnership property: identification of assets treated as partnership property; treatment of goodwill; rules on use of personal assets for partnership purposes.

- Profit and loss allocation: tailoring income and capital profit shares to reflect work, seniority, or capital invested, instead of the statutory equal split.

- Management and decision-making: delineation of roles, voting thresholds, and matters requiring unanimity (e.g. changing the nature of the business, amending the agreement, admitting new partners).

- Authority limits: express restrictions on partners’ authority (e.g. borrowing caps), and procedures to notify third parties of such limits to mitigate apparent authority risk.

- Expulsion and removal: agreed grounds and enhanced majority thresholds (e.g. 75%) for expulsion; fair process.

- Retirement and buy-out: valuation methodology; timetable and payment terms; interest on deferred consideration; restrictive covenants; indemnities to protect the continuing firm and the retiring partner.

- Dispute resolution: internal escalation procedures, mediation and arbitration clauses.

- Accounts and information: preparation of accounts, access rights, and record-keeping.

Agreed terms can be varied only with the consent of all partners (s 19 PA 1890), unless the agreement itself provides for specific variation processes.

Test Tip: If a question says there is no partnership agreement, immediately consider the default rules in ss 24 and 25 PA 1890, especially equal profit shares, no entitlement to remuneration, unanimous consent for new partners, and no expulsion by majority.

Partner liability

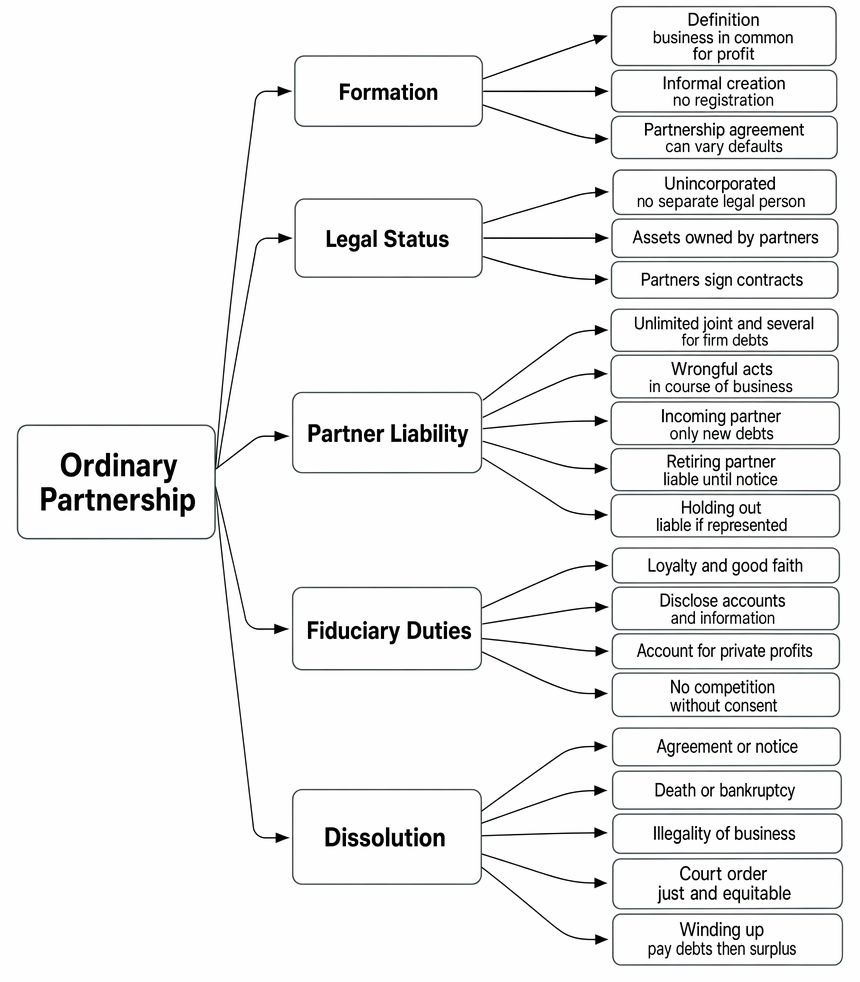

Summary of the principal characteristics of an ordinary partnership, including formation, legal status, liability, fiduciary duties, and dissolution under PA 1890.

Unlimited personal liability

Partners in an ordinary partnership face unlimited personal liability for the debts and obligations of the firm. There is no legal distinction between the business assets and the partners' personal assets.

Key Term: Joint and Several Liability

Creditors can sue all partners together (jointly) or any individual partner (severally) for the full amount of a partnership debt (s 9 PA 1890). Partners are also jointly and severally liable for wrongful acts committed by a partner in the ordinary course of business (ss 10-12 PA 1890).

This personal exposure is a major disadvantage compared to limited companies or LLPs.

Partners are agents of the firm (s 5 PA 1890). A partner’s acts, within the scope of their authority and the ordinary course of the firm’s business, bind the firm and all partners. If partners agree internally to restrict authority, those limits will not protect the firm against third parties acting in good faith unless those third parties have notice of the restriction.

Liability in tort extends to wrongful acts or omissions of a partner done in the ordinary course of the business, or with the authority of co-partners (s 10). The firm is liable where a partner misapplies money or property of a third party received in the course of business (ss 11–12).

Indemnities between partners mitigate internal risk: absent agreement to the contrary, the firm must indemnify each partner for payments made and liabilities incurred in the ordinary and proper conduct of the business (s 24(2)).

Authority of partners to bind the firm

A partner can bind the firm where:

- They have actual authority (express or implied) to enter the transaction; or

- They have apparent (ostensible) authority: to a reasonable third party, the partner appears to have authority, the act is in the ordinary course of the firm’s business, and the third party does not know of any lack of authority.

Examples of acts typically within apparent authority for many partnerships include ordering supplies, engaging employees, and entering routine service contracts. Borrowing or granting security may be outside apparent authority for some firms; careful drafting of authority limits and notifying key counterparties reduces risk.

Where a third party knows a partner lacks authority, the firm will not be bound. Conversely, if the third party reasonably believes the partner has authority and acts in good faith, the firm may be bound even if internal limits were breached.

Exam Warning: Internal restrictions in the partnership agreement do not automatically protect the firm against third parties. Always ask whether the third party had notice of the restriction.

Liability of incoming and outgoing partners

- Incoming partners: Are not automatically liable for debts incurred before they joined (s 17(1) PA 1890). Liability for pre-existing obligations requires express agreement (e.g. novation) with the relevant creditors; often, internal indemnities are used instead.

- Outgoing partners: Remain liable for debts incurred while they were partners (s 17(2) PA 1890). They can also be liable for debts incurred after they leave unless they give proper notice (s 36 PA 1890).

Notice requirements for retiring partners

To avoid liability for future debts, a retiring partner must give:

- Actual notice to those who have dealt with the firm before their retirement.

- Constructive notice (an advertisement in the London Gazette) to potential future creditors who have not dealt with the firm previously (s 36 PA 1890).

A retiring partner should also ensure:

- Removal of their name from the firm’s stationery, website, and any public directories.

- Notification to banks, landlords, key suppliers, and clients.

- Appropriate indemnities from continuing partners, and settlement of the outgoing partner’s share under the agreement.

Holding out

A person who is not a partner (or has retired) can still be liable for partnership debts if they represent themselves, or knowingly allow themselves to be represented, as a partner, and a third party gives credit to the firm based on that representation (s 14 PA 1890).

Key Term: Holding Out

Creating the appearance that someone is a partner when they are not, leading to potential liability if third parties rely on this representation to their detriment.

Worked Example 1.1

Anna, Ben, and Chloe run a graphic design business as an ordinary partnership with no written agreement. The firm owes £15,000 to a supplier. The partnership assets total £6,000. Anna has personal savings of £20,000, Ben has £5,000, and Chloe has no personal savings. How can the supplier recover the debt?

Answer:

The supplier can claim the £6,000 from the partnership assets. For the remaining £9,000, the supplier can sue Anna, Ben, and Chloe jointly or severally. Given their personal assets, the supplier is most likely to pursue Anna for the full £9,000. Anna would then have a right to claim contributions from Ben (£3,000) and Chloe (£3,000) based on their equal share of liability under the PA 1890 default rules, although Chloe's lack of assets might make recovery difficult.

Worked Example 1.2

A partner, Dan, signs a £50,000 three-year equipment lease in the firm’s name. The firm’s business is a small consultancy. The partnership agreement internally prohibits leases over £10,000 unless unanimously approved. The lessor had no notice of this restriction, and leasing office equipment is common in consultancies. Is the firm bound?

Answer:

Yes. Dan had apparent authority: leasing equipment is in the ordinary course of the consultancy’s business and the lessor did not know of any internal restriction. Internal authority limits do not protect the firm against a good faith third party without notice. The firm is bound, and Dan’s breach of internal limits is addressed between partners (e.g. indemnity or disciplinary action under the agreement).

Worked Example 1.3

Jo retires from a food service partnership. She tells two key clients and the bank, but no advert is placed in the London Gazette. A new customer places an order believing Jo is still a partner, based on the firm’s website listing. The firm defaults. Is Jo liable?

Answer:

Jo gave actual notice to existing counterparties but did not give constructive notice. For persons who had not previously dealt with the firm, constructive notice via the London Gazette protects Jo. Because the new customer reasonably relied on the website listing and Jo failed to ensure constructive notice and removal from public materials, Jo risks liability under s 36 and holding out (s 14), unless she can show the customer did not rely on that representation.

Duties between partners

Partners are in a relationship requiring mutual trust and confidence.

Key Term: Fiduciary Duty

A duty of loyalty and good faith owed by partners to each other and the firm.

Key statutory duties under the PA 1890 include:

- Duty to render true accounts and full information (s 28).

- Duty to account for any benefit derived without consent from any transaction concerning the partnership or use of partnership property, name, or business connection (s 29).

- Duty not to compete with the firm without consent (s 30).

These duties are supplemented by the general fiduciary obligation of good faith. Partners must avoid conflicts, disclose relevant information, and not secretly profit from partnership opportunities. Partners may also owe each other a separate duty of care and skill, although its precise scope is uncertain; the cases suggest a partner should not fall below the standard of a reasonable businessperson in the circumstances. Where a partner breaches these duties, remedies include an account of profits, damages for loss, and, in appropriate cases, injunctive relief. Partnership agreements often include more specific duties, such as requirements for full-time commitment to the business, non-compete and non-solicitation covenants, and detailed confidentiality obligations.

Examples:

- Using partnership information to pursue a side venture without consent will trigger an obligation to account to the firm for resulting profits (s 29).

- Carrying on a competing business without consent entitles the firm to claim profits earned from the competing activity (s 30).

Worked Example 1.4

Alex, a partner in an architecture firm, secretly uses the firm’s contacts and brand to secure a private design commission, invoicing through a personal company. The partnership agreement prohibits outside work without consent. What is the firm’s remedy?

Answer:

Alex must account to the firm for the benefit derived (s 29). This includes fees earned and any ancillary benefits obtained using partnership name, property, or business connections. The firm may also enforce contractual remedies in the agreement (e.g. expulsion or damages) and seek an injunction to restrain future breaches.

Dissolution and termination

A partnership can be dissolved (brought to an end) in several ways:

- By expiry of a fixed term or completion of a single venture, if agreed (s 32 PA 1890).

- By notice, if it is a 'partnership at will' (i.e., no fixed term agreed). Any partner can give notice at any time, dissolving the partnership immediately unless the notice specifies a later date (ss 26(1), 32(c) PA 1890).

- By the death or bankruptcy of a partner (s 33 PA 1890), unless agreed otherwise.

- By subsequent illegality making the business unlawful (s 34 PA 1890).

- By court order in specific circumstances, e.g., permanent incapacity of a partner, conduct prejudicial to the business, persistent breaches of the agreement, business operating only at a loss, or on 'just and equitable' grounds (s 35 PA 1890).

Key Term: Dissolution

The process by which a partnership formally ends, leading to the winding up of its affairs and distribution of assets.

After dissolution, partners have continuing authority only so far as necessary to wind up the affairs of the partnership and complete unfinished transactions (s 38). Proper notice of dissolution should be given to counterparties, along with a Gazette advertisement, mirroring retirement notice practices, to prevent liability for post-dissolution acts.

Partnership agreements typically include provisions to allow the partnership to continue despite the exit of a partner, detailing procedures for valuation and payment of the outgoing partner's share to avoid automatic dissolution under the PA 1890 default rules.

Distribution of assets on dissolution

Upon dissolution, partnership assets are used first to pay external debts, then advances made by partners, then partners' capital contributions. Any remaining surplus is distributed according to the profit-sharing agreement (or equally if no agreement exists) (s 44 PA 1890). If assets are insufficient, partners contribute to losses in their profit-sharing proportions.

The distinction between “advances” (loans made by partners to the firm) and “capital” is important. Advances are repaid after external creditors but before capital is returned. Proper accounting records for each partner (capital and current accounts) assist in applying s 44 and in calculating any settlement due on retirement or dissolution.

Worked Example 1.5

XYZ Partnership is dissolved. External creditors total £80,000. Partner loans (advances) total £30,000 (X £10,000; Y £20,000). Capital accounts: X £40,000; Y £30,000; Z £30,000. Partnership assets realise £120,000. Profit shares are equal. How are funds distributed?

Answer:

Apply s 44: pay external creditors (£80,000) first, leaving £40,000. Next repay partner advances: X £10,000 and Y £20,000, leaving £10,000. Then repay capital: X £40,000; Y £30,000; Z £30,000. Only £10,000 remains, so capital cannot be returned in full. The shortfall (£90,000 capital minus £10,000 = £80,000 deficit) is borne by partners in their profit-sharing proportions (here, equally). Each partner’s capital is reduced by £26,666.67, and the £10,000 is distributed equally (£3,333.33 each). Any remaining deficiency is contributed by partners according to the same proportions.

Summary

The lack of separate legal personality and the existence of joint and several liability are fundamental characteristics distinguishing ordinary partnerships from companies and LLPs. Formation may be informal, but the legal and commercial consequences are significant. In practice, a clear partnership agreement is essential to displace unsuitable default rules, regulate authority, and manage retirement and dissolution risk.

Key Point Checklist

This article has covered the following key knowledge points:

- An ordinary partnership arises when two or more persons carry on business in common with a view of profit (s 1(1) PA 1890).

- No registration or written agreement is legally required for formation, but a partnership agreement is highly recommended to vary unsuitable default PA 1890 provisions.

- Ordinary partnerships lack separate legal personality; partners own assets and liabilities directly.

- Partners have unlimited personal liability for partnership debts, which is joint and several.

- Partners owe fiduciary duties to each other, including duties of good faith, disclosure, and accounting for profits.

- Retiring partners remain liable for existing debts and can be liable for future debts if proper notice is not given (s 36 PA 1890).

- Authority of partners to bind the firm arises from actual or apparent authority; internal limits do not protect against third parties without notice.

- Partnerships can be dissolved by agreement, notice (if at will), death/bankruptcy of a partner, illegality, or court order, and accounts are settled in the order set out in s 44 PA 1890.

Key Terms and Concepts

- Partnership

- Partnership Agreement

- Partnership property

- Joint and Several Liability

- Holding Out

- Fiduciary Duty

- Dissolution