Learning Outcomes

This article explains the distribution of profits and capital maintenance under the Companies Act 2006, including:

- How “distribution” is defined in Part 23 CA 2006 and how to identify transfers caught by the regime, using the “relevant accounts” as the legal basis for any payment

- How to distinguish realised from unrealised profits for s 830 CA 2006, including the treatment of revaluation gains, accumulated losses, and reserves when calculating distributable profits

- The additional net assets test for public companies under s 831 CA 2006 and its interaction with undistributable reserves

- The procedures for final and interim dividends, covering board and shareholder authority, timing, record dates, and when each type of dividend becomes a debt or can be revoked

- The legal framework for off‑market purchases of own shares and private company buybacks funded from capital, including statutory steps, Companies House filings, solvency statement, auditor’s report, and creditor protection

- The mechanics and exam‑relevant distinctions between reductions of capital supported by a solvency statement (private companies) and court‑approved reductions (all companies)

- The civil and potential criminal consequences of unlawful distributions for shareholders, directors, and auditors, and the courts’ substance‑over‑form approach to recharacterising disguised returns of value.

SQE1 Syllabus

For SQE1, you are required to have a practical understanding of the rules concerning the distribution of company profits and the maintenance of capital, including identifying lawful methods of returning value to shareholders—particularly dividends—and understanding the procedures and restrictions involved (such as those relating to share buybacks and reductions of capital under the Companies Act 2006), with a focus on the following syllabus points:

- the definition and calculation of distributable profits

- the requirement that any distribution must be justified by “relevant accounts”

- the procedures for declaring and paying lawful dividends

- the consequences of making unlawful distributions

- the doctrine of capital maintenance and its purpose

- the rules and procedures governing share buybacks (out of profits and capital)

- the procedures for effecting a lawful reduction of share capital

- the prohibition on financial assistance for public companies.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A private limited company has accumulated realised profits of £50,000 and accumulated realised losses of £20,000. Can it lawfully pay a dividend of £40,000?

- a) Yes, because it has positive accumulated profits.

- b) No, because the proposed dividend exceeds its net accumulated profits.

- c) Yes, provided the directors recommend it and the shareholders approve by ordinary resolution.

- d) No, because dividends can only be paid out of current year profits.

-

Which of the following is generally required for a private company to declare a final dividend?

- a) A special resolution of the shareholders.

- b) A board resolution only.

- c) A board recommendation followed by an ordinary resolution of the shareholders.

- d) Unanimous consent of the directors.

-

Can a private limited company finance the purchase of its own shares entirely out of capital if it has no distributable profits?

- a) Yes, without restriction.

- b) Yes, but only if approved by a special resolution and following strict procedures including a solvency statement.

- c) No, a buyback must always be funded at least partly from distributable profits or a fresh issue of shares.

- d) No, private companies cannot buy back their own shares out of capital.

Introduction

A primary objective for many companies is to generate profit for their owners, the shareholders. Returning value to shareholders often takes the form of dividend payments. However, the law imposes strict controls on distributions to protect the company's creditors. Creditors rely on the company's capital base as the fund from which they expect to be paid. If companies could freely return capital to shareholders, this fund could be easily diminished, leaving creditors exposed, especially in insolvency.

Part 23 of the Companies Act 2006 (ss 829–853) contains the framework regulating distributions. The term “distribution” is broad and includes dividends, certain buybacks or redemptions of shares, and other transfers of value by a company to its members. A distribution may only be made out of profits available for the purpose and must be justified by “relevant accounts”. In practice, the capital maintenance rules operate alongside the distribution provisions to ensure the company’s capital is preserved unless the Act provides a specific route for its return.

This article focuses on the main method of distributing profits – dividends – outlining the legal tests for determining distributable profits and the procedures for payment. It then examines the fundamental principle of capital maintenance, which restricts the return of capital, exploring the key exceptions: the purchase by a company of its own shares (share buyback) and formal reductions of share capital.

Key Term: Dividend

A payment made by a company to its shareholders, usually out of its profits, distributed typically in proportion to their shareholdings. Key Term: Distribution

Any transfer of value by a company to its members as defined in Part 23 CA 2006, including dividends and certain share buybacks or redemptions, subject to statutory tests and justification by relevant accounts.Test Tip: In SQE-style questions on Distribution of profits and gains, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Dividends

The payment of a dividend is the most common method by which a company distributes its profits to shareholders.

Distributable Profits

The basis of dividend law is the requirement that distributions can only be made out of profits available for the purpose, as defined by the Companies Act 2006 (CA 2006).

Key Term: Distributable Profits

A company’s accumulated, realised profits, so far as not previously utilised by distribution or capitalisation, less its accumulated, realised losses, so far as not previously written off in a reduction or reorganisation of capital duly made (s 830(2) CA 2006).

This definition has several key components:

- Accumulated: Profits and losses are considered over the entire life of the company, not just the last accounting period. Past losses must be offset against past or current profits before a distribution is lawful.

- Realised: Profits must be realised in cash or near‑cash form, consistent with generally accepted UK accounting principles. Profits arising merely from the upward revaluation of assets (for example, property revaluations in the balance sheet) are generally unrealised and cannot be distributed.

- Losses: Both realised profits and realised losses must be accounted for.

Key Term: Realised Profits

Gains recognised in the company’s accounts that have been realised in cash or other assets readily convertible into cash with reasonable certainty, determined in accordance with generally accepted UK accounting principles.

This ensures that dividends are paid from genuine trading surpluses and not from the company's capital base. In addition, any distribution must be justified by “relevant accounts” (s 836 CA 2006). For most private companies, the relevant accounts will be the last annual accounts or, if those are out of date for the proposed distribution, properly prepared interim accounts.

Public companies are subject to an additional safeguard: they must not make a distribution unless their net assets are at least equal to the aggregate of their called‑up share capital and undistributable reserves, and the distribution must not reduce net assets below that level (s 831 CA 2006).

Key Term: Undistributable Reserves

Reserves that cannot be distributed, including the share premium account, the capital redemption reserve, and reserves required by law or the articles to be maintained (see s 831(4) CA 2006). Key Term: Capital Redemption Reserve

A statutory reserve created when a company redeems or buys back its own shares out of distributable profits; it is treated as undistributable (ss 687–689 CA 2006). Key Term: Relevant Accounts

The company’s last annual accounts or, where needed, properly prepared interim accounts used to determine whether a proposed distribution is supported by distributable profits (s 836 CA 2006).

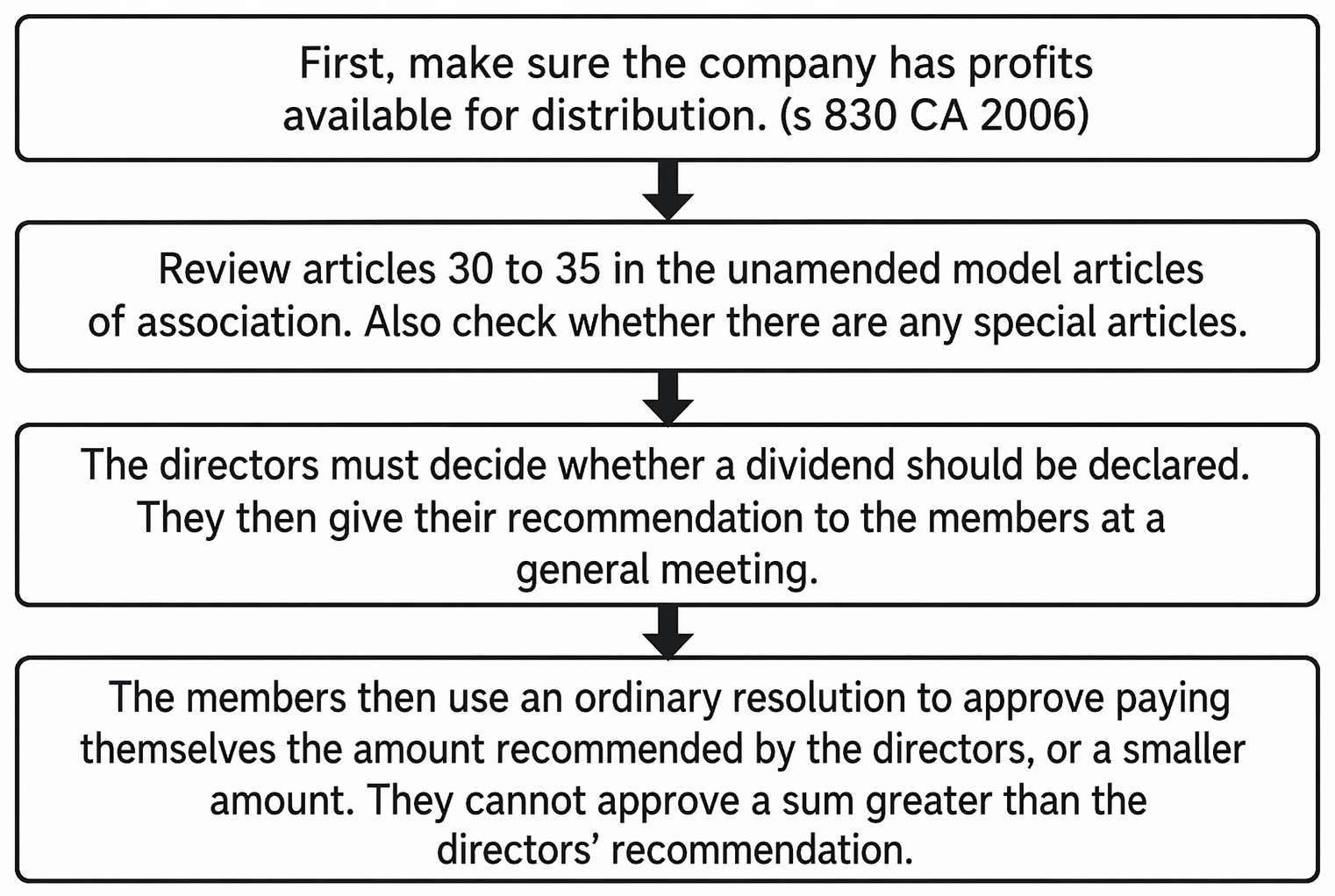

Procedure for Declaring and Paying Dividends

The company's articles of association usually dictate the precise procedure. The Model Articles (MAs) for private companies limited by shares provide a common framework:

-

Final Dividends:

- The directors recommend the amount of the final dividend (MA 30(1)(a)). They must satisfy themselves that the company has sufficient distributable profits and that the distribution is supported by relevant accounts.

- The shareholders declare the dividend by ordinary resolution (MA 30(2)). Importantly, shareholders cannot declare a dividend higher than the amount recommended by the directors, although they can approve a lower amount or declare no dividend at all.

-

Interim Dividends:

- The directors may decide to pay interim dividends during the financial year if they are satisfied that the company's financial position justifies it (MA 30(1)(b)). Shareholder approval is not required for interim dividends. Directors must still ensure sufficient distributable profits exist at the time of payment and that relevant accounts support the distribution.

Once declared, a final dividend becomes a debt owed by the company to the shareholders entitled to receive it. By contrast, interim dividends are ordinarily revocable until actually paid; they do not create a debt until payment is made unless the board makes an unconditional commitment to pay.

Key Term: Treasury Shares

Shares held by a public company following a buyback instead of immediate cancellation; private companies must cancel shares on acquisition and cannot hold shares in treasury.

Worked Example 1.1

Oak Ltd made a profit of £20,000 in its first year (Year 1). It made a loss of £30,000 in Year 2. In Year 3, it made a profit of £50,000. What are its total distributable profits at the end of Year 3?

Answer:

Accumulated realised profits = £20,000 (Year 1) + £50,000 (Year 3) = £70,000. Accumulated realised losses = £30,000 (Year 2). Distributable Profits = £70,000 - £30,000 = £40,000. Oak Ltd can lawfully distribute up to £40,000 as dividends.

Worked Example 1.2

Delta Ltd wishes to buy back 5,000 £1 shares from shareholder X for £10 per share (£50,000 total). Delta Ltd has distributable profits of £60,000. What shareholder resolution(s) are required?

Answer:

Since Delta Ltd has sufficient distributable profits (£60,000) to cover the entire buyback cost (£50,000), the buyback can be funded entirely out of profits. Therefore, only an ordinary resolution under s 694 CA 2006 is required to approve the terms of the buyback contract. A special resolution for payment out of capital is not needed.

Worked Example 1.3

Birch Plc shows called‑up share capital of £2,000,000 and undistributable reserves of £500,000. Its net assets are £2,700,000. Can Birch Plc lawfully pay a dividend of £300,000?

Answer:

Under s 831 CA 2006, a public company’s net assets must not fall below called‑up share capital plus undistributable reserves as a result of the distribution. The floor is £2,500,000 (£2,000,000 + £500,000). Current net assets are £2,700,000. A £300,000 dividend would reduce net assets to £2,400,000, below the floor, so the dividend would be unlawful.

Consequences of Unlawful Dividends

Paying a dividend otherwise than out of distributable profits (an 'unlawful' or 'ultra vires' dividend) has serious consequences:

-

Shareholder Liability: Shareholders who receive a distribution knowing, or having reasonable grounds to believe, that it is unlawful, are liable to repay it (or the unlawful part of it) to the company (s 847 CA 2006). Bona fide recipients without such knowledge are generally not liable under s 847, but other restitutionary remedies may be relevant in extreme cases.

-

Director Liability: Directors who authorise an unlawful dividend may be liable for breach of their duties, including the duty to exercise reasonable care, skill, and diligence (s 174 CA 2006) and potentially the duty to act within powers (s 171 CA 2006). They may be required to personally repay the unlawful amount to the company (for example, Bairstow v Queens Moat Houses plc [2001]). Liability is fault‑based; a director who has taken reasonable care to ensure the preparation of accounts that show a lawful dividend may avoid personal liability (see Burnden Holdings (UK) Ltd v Fielding [2019]).

-

Auditor Liability: If an unlawful distribution is made based on erroneous accounts, the company’s auditor, if negligent in failing to detect the error, can be liable to the company for losses (for example, Leeds Estate Building and Investment Co v Shepherd (1887)).

The courts focus on substance over form: transactions dressed up to appear lawful may be recharacterised by the court if their real effect is to make an unlawful distribution (Progress Property Co Ltd v Moorgarth Group Ltd [2010]).

Creditors generally do not have standing to restrain a proposed unlawful distribution, but other insolvency remedies may be available (for example, a winding‑up petition if the company is unable to pay its debts).

Capital Maintenance

The rules on distributable profits are part of a wider legal doctrine known as capital maintenance.

Key Term: Capital Maintenance

The fundamental company law principle that a company's share capital must be maintained as a permanent fund available to creditors and cannot be returned to shareholders except through specific, legally sanctioned procedures.

This principle protects creditors who rely on the company's capital base when deciding whether to grant credit. If companies could return capital freely, the creditors' buffer could vanish. The main exceptions where capital can be lawfully returned are share buybacks and formal reductions of capital.

It is also important to note that the general statutory prohibition on a public company giving financial assistance for the acquisition of its shares remains (ss 678–679 CA 2006). Private companies are no longer generally subject to the prohibition, but public companies must still ensure that their resources are not used to assist the purchase of shares in a way that prejudices creditors.

Share Buybacks (Purchase of Own Shares)

A company purchasing its own shares reduces its capital and assets. Therefore, it is generally prohibited (s 658 CA 2006) unless done in accordance with the strict procedures laid out in Part 18 of the CA 2006.

Key Term: Share Buyback

A transaction where a company repurchases shares from its own shareholders, subsequently cancelling them (usually), thus reducing its issued share capital. Key Term: Permissible Capital Payment (PCP)

The amount of capital that a private company may lawfully use to fund a buyback once it has exhausted available distributable profits and the proceeds of any fresh issue (ss 709–710 CA 2006).

Funding the Buyback

The source of funds is critical and strictly regulated:

- Distributable Profits: This is the preferred and primary source. A buyback funded entirely from distributable profits does not deplete the company's capital (s 692(2)(a) CA 2006).

- Proceeds of a Fresh Issue of Shares: A company can issue new shares specifically to fund a buyback (s 692(2)(a) CA 2006). The capital base is maintained as new capital replaces the capital returned.

- Out of Capital (Private Companies Only): Private companies have a limited power to finance a buyback out of capital under ss 709–723 CA 2006. This is only permitted if distributable profits are insufficient (s 710). The procedure is significantly more complex and designed to protect creditors.

Key Term: Solvency Statement (Buyback)

A statutory declaration by all directors (made no more than one week before the special resolution) that the company is able to pay its debts and will remain solvent for the next 12 months, supported by an auditor’s report (s 714 CA 2006). Making the statement without reasonable grounds is a criminal offence.

Private companies must cancel shares they purchase (s 706 CA 2006) and cannot hold them as treasury shares. Public companies may, in certain circumstances, hold repurchased shares as treasury shares and reissue them, but that option is not available to private companies.

Key Term: Off‑Market Purchase

A buyback that is not conducted on a recognised investment exchange; typical for private companies where the terms are set out in a contract approved by shareholders (s 694 CA 2006). Key Term: On‑Market Purchase

A buyback executed by a listed public company through a recognised investment exchange under separate rules; not applicable to private companies.

Procedure: Off‑Market Purchase (Private Companies)

The following steps are required for a buyback funded from distributable profits or a fresh issue:

-

Articles Check: Ensure the articles do not prohibit or restrict buybacks (s 690(1)(b)). If they do, they must be amended by special resolution.

-

Funding Check: Verify sufficient distributable profits or proceeds from a fresh issue are available. Shares must be fully paid (s 691(1)).

-

Contract Approval: The buyback contract terms require shareholder approval by ordinary resolution before the contract is entered into (s 694).

- Voting Restriction: The selling shareholder(s) cannot vote on the OR if the resolution would not have passed without their votes (s 695). This applies to votes cast in respect of the shares being bought back.

- Contract Availability: A copy of the contract (or a written memorandum of terms if not in writing) must be available for inspection by shareholders for at least 15 days before the GM and at the meeting itself (or circulated with a written resolution) (s 696).

-

Payment: Generally, payment must be made on purchase (s 691(2)).

-

Post‑Buyback:

- File Form SH03 (Return of purchase of own shares) at Companies House within 28 days (s 707).

- File Form SH06 (Notice of cancellation of shares) at Companies House within 28 days (s 708). The shares are treated as cancelled upon acquisition (s 706).

- Update the register of members.

- Keep a copy of the contract available for inspection for 10 years (s 702).

Procedure: Payment Out of Capital (Private Companies)

This procedure involves additional steps on top of those for a purchase out of profits:

Final dividend procedure is shown, from directors’ recommendation and ordinary resolution to payment, subject to s 830 CA 2006.

- Use Profits First: Capital can only be used to the extent distributable profits are insufficient (s 710). The amount paid from capital is the PCP.

- Directors’ Solvency Statement: All directors must make a statutory declaration of solvency not more than one week before the shareholders pass the special resolution (s 714). This states that the company can pay its debts and will remain solvent for the next 12 months. Making this statement without reasonable grounds is a criminal offence.

- Auditor's Report: The solvency statement must be accompanied by a report from the company's auditor confirming it is not unreasonable (s 714(6)).

- Shareholder Special Resolution: In addition to the OR approving the contract, shareholders must pass a special resolution approving the payment out of capital (s 716). This SR must be passed within one week after the solvency statement is made. The selling shareholder(s) votes are disregarded if the SR would not pass without them (s 717).

- Publicity for Creditors: Within one week of the SR, the company must publish a notice in the London Gazette and either a national newspaper or give written notice to all creditors (s 719). This alerts creditors to the proposed use of capital.

- Filing at Companies House: The SR, solvency statement, and auditor’s report must be filed at Companies House within the prescribed period (s 720B and s 30).

- Creditor/Member Objection: Creditors or dissenting shareholders have a five‑week period following the SR to apply to court to cancel it (s 721).

- Payment Timing: Payment out of capital cannot be made earlier than five weeks or later than seven weeks after the SR is passed (s 723). This allows time for objections.

Worked Example 1.4

Elm Ltd proposes a £120,000 off‑market buyback. It has £80,000 distributable profits and no proceeds from a fresh issue. Can Elm Ltd fund the remaining £40,000 from capital, and what additional approvals are required?

Answer:

Yes. Under s 710 CA 2006 Elm Ltd must use its £80,000 distributable profits first. The remaining £40,000 is the PCP. The company must approve the buyback contract by ordinary resolution (s 694) and pass a special resolution authorising payment out of capital (s 716), supported by a directors’ solvency statement (s 714) and auditor’s report. It must then comply with the Gazette and creditor notification requirements and timing constraints (ss 719 and 723).

Reduction of Share Capital

A company can reduce its share capital using the procedures in ss 641–653 CA 2006. This is another way capital might be returned to shareholders or used to eliminate losses shown in the accounts.

Key Term: Reduction of Share Capital

A formal procedure under the Companies Act 2006 allowing a company to reduce its issued share capital, often involving returning capital to shareholders or cancelling unpaid capital.

There are two main procedures:

-

Special Resolution supported by Solvency Statement (Private Companies Only): This simplified route (ss 641(1)(a), 642–644) avoids court involvement. The directors must make a solvency statement confirming the company's ability to pay its debts currently and for the next 12 months. The solvency statement must be made not more than 15 days before the special resolution. Shareholders then pass a special resolution. The solvency statement and SR must be filed at Companies House. Making a solvency statement without reasonable grounds is a criminal offence.

-

Special Resolution confirmed by Court Order (All Companies): This route (ss 641(1)(b), 645–651) requires court confirmation after the shareholders pass a special resolution. The court must be satisfied that the interests of creditors are adequately protected. Creditors have the right to object, and the court may require security or other measures to protect them.

A reduction of capital is often used to eliminate accumulated losses to restore the company’s ability to pay dividends in the future or to return surplus capital to shareholders. It must be reflected in the company’s statement of capital and filings.

Exam Warning: Do not confuse a share buyback with a reduction of capital. While both can result in capital being returned to shareholders, they are distinct procedures with different requirements. A buyback involves purchasing existing shares, often from a specific shareholder, whereas a reduction typically applies across a class of shares or cancels unpaid capital. In a private company buyback, a solvency statement and auditor’s report are required only where capital is used; in a reduction of capital (private company solvency statement route) every director must sign the solvency statement and the 15‑day timing rule applies.

Summary

Table: Distributions and Capital Maintenance Procedures

| Procedure | Main Purpose | Funding Source(s) | Key Shareholder Approval | Court Involvement Required? |

|---|---|---|---|---|

| Dividend (Final) | Distribute profits | Distributable Profits | Ordinary Resolution | No |

| Dividend (Interim) | Distribute profits | Distributable Profits | None (Director decision) | No |

| Share Buyback | Return value/provide exit for shareholder | Distributable Profits / Fresh Issue | Ordinary Resolution | No |

| Share Buyback (PCP) | Return value/provide exit for shareholder | Capital (Private Co's only, if profits insufficient) | OR (Contract) + SR (Capital) | No (unless creditor objects) |

| Reduction of Capital (Private Co) | Return capital / Write off lost capital | Reduction of Share Capital Account | Special Resolution (+ Solvency Statement) | No |

| Reduction of Capital (All Co's) | Return capital / Write off lost capital | Reduction of Share Capital Account | Special Resolution | Yes (Court Confirmation) |

Key Point Checklist

This article has covered the following key knowledge points:

- Distributions (including dividends) must be made only out of distributable profits and must be justified by relevant accounts.

- Distributable profits are accumulated realised profits less accumulated realised losses; revaluation gains are generally not distributable.

- Public companies are subject to an additional net assets test under s 831 CA 2006.

- Final dividends typically require director recommendation and shareholder OR; interim dividends can usually be paid by directors alone and are revocable until paid.

- Unlawful distributions trigger liability for knowing recipients and can expose directors (and auditors, if negligent) to repayment obligations.

- The capital maintenance doctrine protects creditors by restricting returns of capital to shareholders.

- Share buybacks are a permitted exception, funded primarily by distributable profits or a fresh share issue, requiring OR approval of the contract and filings (SH03/SH06).

- Private companies can fund buybacks out of capital using the PCP procedure, which involves a solvency statement, auditor’s report, creditor/public notice, and a special resolution.

- Reductions of capital are permitted via SR plus solvency statement (private companies) or SR plus court confirmation (all companies), with creditor protections.

- Public companies are prohibited from giving financial assistance for the acquisition of their shares; private companies are generally not.

Key Terms and Concepts

- Dividend

- Distribution

- Distributable Profits

- Realised Profits

- Undistributable Reserves

- Capital Redemption Reserve

- Relevant Accounts

- Capital Maintenance

- Share Buyback

- Permissible Capital Payment (PCP)

- Solvency Statement (Buyback)

- Off‑Market Purchase

- On‑Market Purchase

- Reduction of Share Capital

- Treasury Shares