Learning Outcomes

This article outlines the main anti-avoidance provisions relevant to UK corporation tax for SQE1 candidates, including:

- The scope and purpose of the General Anti-Abuse Rule (GAAR), the double reasonableness test, and how HMRC applies “just and reasonable” counteraction to deny abusive tax advantages.

- The distinction between GAAR and purposive statutory interpretation under the Ramsay principle, and how to decide which analysis to apply in exam scenarios.

- Targeted Anti-Avoidance Rules (TAARs), with emphasis on close company loans to participators (s.455), the 30-day replacement loan rule (s.464C), and the policy reasons behind them.

- The operation of transfer pricing under the arm’s length principle, including typical HMRC adjustments and the relevance of SMEs and double tax relief.

- Loan relationship and derivative contract “unallowable purpose” rules, focusing on when debits are disallowed because a main purpose is to obtain a tax advantage.

- Hybrid mismatch rules, their role in neutralising double deductions and deduction / no-inclusion outcomes, and common cross-border structures they target.

- The Controlled Foreign Companies (CFC) regime, gateways, exemptions, safe harbours, and how CFC charges are computed and attributed.

- Diverted Profits Tax (DPT), including its scope, higher rate, notification and charging procedures, and its interaction with transfer pricing and CFC rules.

- The combined use of GAAR, TAARs, and international measures in structuring exam answers that address profit shifting and base erosion comprehensively.

SQE1 Syllabus

For SQE1, you are required to understand the anti-avoidance provisions relevant to UK corporation tax, with a focus on the following syllabus points:

- The scope and operation of the General Anti-Abuse Rule (GAAR) and the double reasonableness test

- The role and application of Targeted Anti-Avoidance Rules (TAARs), including those on close company loans and transfer pricing

- International anti-avoidance measures, such as Controlled Foreign Companies (CFC) rules and the Diverted Profits Tax (DPT)

- The interaction between GAAR, TAARs, and international rules in countering tax avoidance schemes

- The practical consequences for companies and the approach of HMRC to abusive arrangements

- GAAR’s priority over other tax provisions and the “just and reasonable” counteraction mechanism

- Ramsay principles of purposive statutory interpretation alongside GAAR

- Loan relationship and derivative contract “unallowable purpose” rules

- Hybrid mismatch rules neutralising double deductions and deduction/no-inclusion outcomes

- Arm’s length principle in transfer pricing and SME considerations

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the purpose of the General Anti-Abuse Rule (GAAR) in UK corporation tax, and what is the double reasonableness test?

- How does the TAAR on loans to participators in close companies operate, and what is its intended effect?

- What is the Controlled Foreign Companies (CFC) regime designed to prevent, and how can it affect a UK parent company?

- When might the Diverted Profits Tax (DPT) apply to a multinational group, and why is its rate higher than the standard corporation tax rate?

Introduction

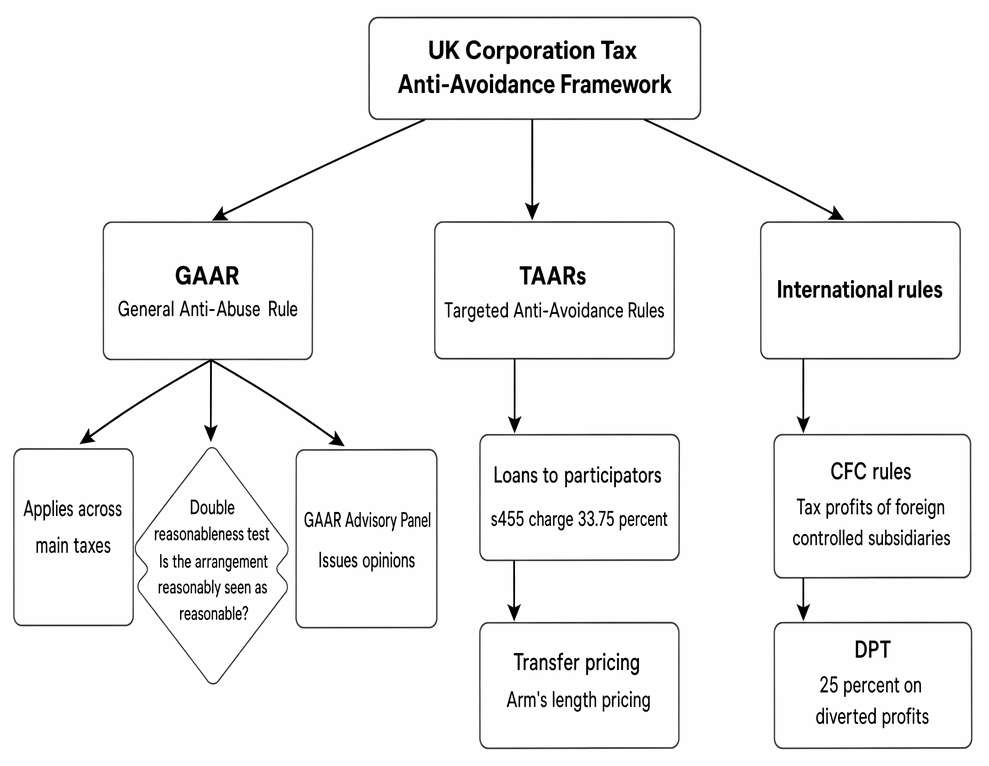

Corporation tax anti-avoidance provisions are a core part of the UK tax system, designed to prevent companies from reducing their tax bills through artificial or abusive arrangements. The main tools are the General Anti-Abuse Rule (GAAR), Targeted Anti-Avoidance Rules (TAARs), and international measures such as the Controlled Foreign Companies (CFC) regime and the Diverted Profits Tax (DPT). These rules work together to ensure that companies pay the correct amount of tax in line with the intention of the law. It is essential to distinguish lawful tax planning from abusive avoidance. GAAR targets arrangements that go beyond acceptable planning and empowers HMRC to counteract the resulting tax advantage with adjustments that are “just and reasonable”.

UK corporation tax anti-avoidance provisions are summarised under the headings of GAAR, TAARs and international anti-avoidance rules.

Key Term: Tax avoidance

Arranging affairs within the law to minimise tax liability. Lawful, but may be restricted by anti-avoidance provisions. Key Term: Tax evasion

Deliberately misapplying or misrepresenting the law to minimise tax liability. Illegal and subject to penalties.Test Tip: In SQE-style questions on Anti-avoidance provisions, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

The General Anti-Abuse Rule (GAAR)

The GAAR is a statutory rule that allows HMRC to counteract tax advantages arising from arrangements that are considered abusive.

Key Term: General Anti-Abuse Rule (GAAR)

A statutory rule that enables HMRC to deny tax advantages from arrangements judged to be abusive, based on a double reasonableness test.

GAAR applies across major taxes relevant to SQE1, including income tax, capital gains tax, inheritance tax, corporation tax, and stamp duty land tax. Its purpose is both deterrence and remedial counteraction: to discourage abusive schemes and, where implemented, to allow HMRC to make tax adjustments that are just and reasonable in all the circumstances. GAAR takes priority over other tax legislation relating to the relevant taxes, although in practice HMRC will often rely on specific TAARs first if they clearly apply.

Key Term: Ramsay principle

A purposive approach to interpreting tax statutes, allowing courts to look at the overall effect of pre-ordained, artificial steps and to tax transactions according to their commercial substance rather than their form.

The Ramsay approach and GAAR work in tandem: Ramsay guides interpretation of specific provisions purposively; GAAR provides a separate statutory tool against abuse even where a literal reading might otherwise produce a tax advantage.

The Double Reasonableness Test

The GAAR applies if an arrangement cannot reasonably be regarded as a reasonable course of action in relation to the relevant tax provisions, having regard to all the circumstances. This is known as the double reasonableness test.

Key Term: Double Reasonableness Test

The test under GAAR asking whether it is reasonable to regard the arrangement as a reasonable course of action, considering all circumstances.

In assessing this, indicators of abuse include contrived or abnormal steps, circularity, exploitation of legislative gaps, and arrangements lacking commercial substance apart from tax outcomes. If an arrangement is found to be abusive, HMRC can make adjustments to counteract the tax advantage. Counteraction is performed on a “just and reasonable” basis, which may include reallocating profits, denying reliefs, or recharacterising transactions.

GAAR Advisory Panel

The GAAR Advisory Panel provides opinions on whether arrangements are abusive, giving guidance to both taxpayers and HMRC.

Key Term: GAAR Advisory Panel

An independent panel that issues opinions on whether a tax arrangement is abusive under the GAAR.

Under GAAR procedures, HMRC will notify the taxpayer of proposed counteraction. Representations can be made and the Panel may opine on whether the arrangements are abusive; while not determinative, the Panel’s view carries weight. There are no direct penalties under GAAR itself, but failure to pay adjusted liabilities attracts penalties under general tax compliance rules. Additionally, “enablers” of abusive schemes may face separate penalties under other legislation.

Worked Example 1.1

A UK company sets up a subsidiary in a low-tax jurisdiction. The subsidiary has no staff or real activity but receives large royalty payments from the UK company, reducing UK taxable profits.

Question: Would this arrangement likely be caught by GAAR?

Answer:

Yes. While international structuring can be legitimate, if the subsidiary lacks substance and the arrangement is designed solely to avoid UK tax, it is likely to be considered abusive under the double reasonableness test.

Targeted Anti-Avoidance Rules (TAARs)

TAARs are specific statutory provisions aimed at particular types of tax avoidance. They operate alongside GAAR to address known avoidance risks.

Key Term: Targeted Anti-Avoidance Rule (TAAR)

A statutory rule aimed at countering specific tax avoidance strategies, such as loans to participators or transfer pricing.

Loans to Participators in Close Companies

A close company is a company controlled by five or fewer shareholders or by its directors.

Key Term: Close Company

A company controlled by five or fewer shareholders (participators) or by its directors. Key Term: Participator

A person with a share or interest in a company’s capital or income (e.g. shareholder), including certain associates. For close companies, TAARs often apply to participators and their associates.

If a close company makes a loan to a participator (such as a director-shareholder), a tax charge arises under s. 455 Corporation Tax Act 2010. The charge is intended to deter value extraction via loans instead of taxable distributions. The charge is currently 33.75% of the outstanding loan. Relief is available if the loan is repaid, usually through a mechanism that credits the company with the s.455 tax previously paid. However, additional TAARs prevent “bed and breakfasting” to secure relief.

One key TAAR (CTA 2010 s.464C) targets repayment followed by a replacement loan within a short period (usually within 30 days), denying relief except for any net reduction in the loan balance. A further rule can deny relief where the repayment is funded by a third party and there is an arrangement to re-lend shortly after. If the loan is written off or released, this generally triggers income tax on the participator as a distribution and may have separate employment tax consequences for director-employees. Beneficial loan rules can also impose income tax charges on director-shareholders who enjoy a cheap or interest-free loan.

Worked Example 1.2

XYZ Ltd, a close company, lends £50,000 to its director-shareholder. The loan is not repaid within nine months of the end of the accounting period.

Question: What is the tax consequence for XYZ Ltd?

Answer:

XYZ Ltd must pay a tax charge of 33.75% of the loan amount (£16,875) under s. 455. This charge is repayable if the loan is repaid, but it discourages tax-free extraction of value.

Worked Example 1.3

ABC Ltd makes a £80,000 loan to a participator. Shortly before the nine-month deadline, the participator repays £80,000. Thirty days later, ABC Ltd advances a new £75,000 loan.

Question: How does the s.464C TAAR affect s.455 relief?

Answer:

Relief is denied except to the extent of any genuine net reduction in the loan balance. Because the loan was replaced within 30 days, only the £5,000 net reduction qualifies. The company remains liable for the s.455 charge corresponding to the £75,000 effectively outstanding.

Transfer Pricing

Transfer pricing rules prevent companies from shifting profits by setting artificial prices in transactions with connected parties.

Key Term: Transfer Pricing

Rules requiring transactions between connected parties to be priced as if they were between independent parties (arm’s length), with HMRC empowered to adjust taxable profits. Key Term: Arm’s length principle

The standard requiring pricing and terms between associated enterprises to match those that would have been agreed by independent parties in comparable circumstances.

The UK transfer pricing regime (broadly under TIOPA 2010) applies the arm’s length principle to connected-party transactions. HMRC can make a primary adjustment to replace actual terms with arm’s length terms, increasing UK taxable profits if prices were understated or decreasing them if overstated. Corresponding adjustments may be available under double tax treaties to alleviate double taxation. While SMEs benefit from certain administrative easements, the arm’s length principle remains the benchmark.

Worked Example 1.4

A UK manufacturer sells components to its overseas subsidiary at below-market prices, leaving low profits in the UK and high profits offshore.

Question: How will transfer pricing apply?

Answer:

HMRC can adjust the intra-group price to an arm’s length level. This increases the UK company’s taxable profits. The overseas jurisdiction may provide a corresponding adjustment under the relevant double tax treaty to prevent double taxation.

Other corporate TAARs: loan relationships and hybrids

Companies are taxed on debits and credits arising from loan relationships and derivative contracts. Anti-avoidance rules target arrangements designed to secure tax advantages through financing structures.

Key Term: Loan relationship

A company’s rights and obligations under a money debt (e.g. borrowings and lending), taxed under the loan relationships regime in CTA 2009. Key Term: Unallowable purpose

A rule within the loan relationships and derivative contracts regimes that disallows debits (and can adjust credits) where a main purpose of the arrangements is to obtain a tax advantage. Key Term: Hybrid mismatch rules

Rules that neutralise tax advantages from arrangements exploiting differences between jurisdictions’ tax treatment (e.g. double deductions or deduction/no inclusion outcomes).

Under the “unallowable purpose” rule (CTA 2009), where one of the main purposes of a company’s loan or derivative arrangements is to secure a tax advantage, related debits may be disallowed or restricted. Hybrid mismatch rules (FA 2016) counter double-deduction and deduction/no-inclusion outcomes arising from hybrid entities or instruments, often in cross-border settings. Both sets of rules are frequently encountered in corporate finance structures and operate independently of GAAR.

Worked Example 1.5

UKCo borrows from an offshore group entity at a high interest rate and immediately on-lends to a connected company interest-free. The arrangement produces large UK interest debits but little commercial benefit.

Question: How might the unallowable purpose rule apply?

Answer:

HMRC may disallow some or all of the interest debits if a main purpose of the financing structure is to obtain a UK tax advantage rather than achieve genuine commercial outcomes. The debits would be restricted to reflect a justifiable commercial level.

Worked Example 1.6

A UK company issues a hybrid instrument treated as debt in the UK (yield deductible) but equity in the overseas jurisdiction (yield not taxed there). The arrangement produces a deduction/no inclusion outcome.

Question: What is the effect under hybrid mismatch rules?

Answer:

The rules neutralise the advantage, typically by denying the UK deduction. HMRC would adjust the company’s tax computation to eliminate the mismatch-based benefit.

International Anti-Avoidance Measures

Global groups often seek to reduce tax by shifting profits to low-tax countries. The UK has rules to counteract this.

Controlled Foreign Companies (CFC) Rules

The CFC regime targets profits diverted to foreign subsidiaries controlled by UK companies.

Key Term: Controlled Foreign Company (CFC)

A non-UK company controlled by UK persons, whose profits may be attributed to UK resident companies for tax purposes where artificially diverted from the UK.

If a CFC’s profits arise from artificial arrangements to avoid UK tax, those profits can be taxed in the UK. Modern CFC rules incorporate a “gateway” concept: profits are chargeable only if they pass through a charge gateway indicating artificial diversion. There are several exemptions and safe harbours, commonly including:

- Excluded or low-risk territories and activities

- Low profit and low profit margin conditions

- Effective tax rate tests

- Exempt periods to facilitate commercial restructuring

- Finance company exemptions subject to conditions

The CFC charge is assessed on UK resident companies with sufficient interests in the CFC. Transfer pricing principles often interact with CFC analyses, and double tax relief can apply where foreign taxes have been paid.

Worked Example 1.7

UK Parent owns 100% of Offshore Sub, which books substantial profits from licensing IP developed by UK Parent, with minimal staff and decision-making offshore.

Question: How could the CFC rules apply?

Answer:

If Offshore Sub’s profits are found to be artificially diverted from UK activities, they may pass the CFC charge gateway and be apportioned to UK Parent for UK tax, subject to any applicable safe harbours and double tax relief.

Diverted Profits Tax (DPT)

DPT is a separate tax at a higher rate designed to deter profit diversion from the UK.

Key Term: Diverted Profits Tax (DPT)

A UK tax, currently at 31%, on profits diverted from the UK by large multinational groups using artificial arrangements, with separate charging provisions and notification requirements.

DPT applies in two main cases. First, where a group avoids a UK taxable presence by using arrangements to sidestep a permanent establishment while carrying on activities in the UK. Second, where entities exploit tax mismatches and lack sufficient economic substance, resulting in diversion of profits from the UK.

Key Term: Permanent establishment (PE)

A fixed place of business through which an enterprise’s business is carried on, or a dependent agent habitually concluding contracts, giving rise to a taxable presence under UK law and treaties.

DPT is charged at a higher rate (currently 31%) than the main rate of corporation tax to incentivise compliance and discourage profit diversion. It has distinct procedural features: potential payers may need to notify HMRC and HMRC can issue charging notices with a review period during which companies can amend their corporation tax returns to align with transfer pricing, thereby avoiding the DPT charge.

Worked Example 1.8

A multinational group sells products in the UK through a local agent, but claims that profits are earned by an offshore company with no real UK presence.

Question: How might DPT apply?

Answer:

If the arrangement is found to artificially avoid a UK taxable presence, DPT can be charged at 31% on the diverted profits, even if corporation tax does not apply.

Worked Example 1.9

UKCo enters into arrangements with a low-tax affiliate that contractually owns IP, charges large royalties, and has minimal staff. UKCo’s UK operations effectively create and exploit the IP.

Question: Could DPT be relevant alongside transfer pricing?

Answer:

Yes. HMRC may first seek arm’s length adjustments under transfer pricing. If the arrangements also meet DPT conditions (e.g. tax mismatch and insufficient economic substance), DPT could be charged at 31% on diverted profits, unless UKCo amends its CT position during HMRC’s DPT review window.

How the Rules Interact

GAAR, TAARs, and international rules work together. A single arrangement may be challenged under more than one provision. For example, a profit-shifting scheme might be caught by transfer pricing rules, CFC rules, and GAAR if it is abusive. GAAR takes priority, but HMRC typically prefers to apply specific TAARs where available and only invoke GAAR for egregious abuse or residual cases.

Hybrid mismatch and loan relationship “unallowable purpose” rules can apply to the same financing arrangements that might also draw GAAR scrutiny. DPT sits alongside transfer pricing and CFC provisions as a deterrent and a backstop; companies are encouraged to self-correct to arm’s length outcomes to avoid DPT exposure. Care must be taken to avoid double counting; where adjustments under one regime increase UK tax, reliefs and credits (including for foreign taxes and corresponding adjustments) should be considered.

Exam Warning: Some arrangements may fall under both GAAR and a TAAR. HMRC may use all available tools to counteract tax avoidance. Always consider the interaction of rules in exam scenarios.

Case Law and Practical Application

Key cases illustrate how anti-avoidance rules are applied. The courts increasingly adopt purposive interpretation consistent with the Ramsay principle, analysing the commercial substance of transactions rather than their formal steps.

Worked Example 1.10

In HMRC v Hyrax Resourcing Ltd [2019], a scheme paid employees via offshore trusts, claiming payments were loans and not taxable.

Question: Was this arrangement effective?

Answer:

No. The tribunal found the arrangement was abusive and HMRC applied GAAR to counteract the tax advantage, treating the payments as taxable income. Other decisions in the anti-avoidance sphere show the broader purposive approach even outside GAAR, reinforcing that contrived steps and circular transactions are unlikely to succeed where their only real function is tax advantages. In practice, HMRC increasingly deploys transfer pricing, hybrid mismatch and loan relationship rules to counteract financing and IP structures, reserving GAAR for particularly artificial arrangements. For multinational groups, DPT has proven effective in encouraging timely self-correction and robust documentation.

Worked Example 1.11

A group implements a financing structure where a UK company deducts interest on a hybrid instrument while an affiliate claims a corresponding deduction abroad. The affiliate lacks substantive activities.

Question: Which anti-avoidance rules could apply?

Answer:

Hybrid mismatch rules neutralise the deduction/no-inclusion or double deduction outcome. If the structure also lacks economic substance and diverts UK profits, DPT may apply. If the arrangement is highly contrived, GAAR could be considered, but specific TAARs are likely to be applied first.

Key Point Checklist

This article has covered the following key knowledge points:

- The General Anti-Abuse Rule (GAAR) allows HMRC to counteract abusive tax arrangements using the double reasonableness test and “just and reasonable” counteraction.

- GAAR applies across major taxes and takes priority over other provisions, operating alongside purposive interpretation under the Ramsay principle.

- Targeted Anti-Avoidance Rules (TAARs) address specific avoidance risks, including loans to participators (s.455) with the 30-day replacement loan TAAR (s.464C) and transfer pricing under the arm’s length principle.

- Loan relationship and derivative contract “unallowable purpose” rules restrict deductions where a main purpose is to secure a tax advantage.

- Hybrid mismatch rules neutralise tax advantages arising from cross-border treatment differences (double deductions and deduction/no-inclusion).

- International measures, including CFC rules and DPT, prevent profit shifting and base erosion by multinational groups; DPT is charged at 31% and has distinct procedural features.

- GAAR, TAARs, and international rules can apply together; HMRC typically applies specific rules first and uses GAAR for residual abusive arrangements.

- Practical examples and case law demonstrate how these rules operate in real scenarios, with HMRC focusing on substance over form.

Key Terms and Concepts

- Tax avoidance

- Tax evasion

- General Anti-Abuse Rule (GAAR)

- Double Reasonableness Test

- GAAR Advisory Panel

- Ramsay principle

- Targeted Anti-Avoidance Rule (TAAR)

- Close Company

- Participator

- Transfer Pricing

- Arm’s length principle

- Loan relationship

- Unallowable purpose

- Hybrid mismatch rules

- Controlled Foreign Company (CFC)

- Diverted Profits Tax (DPT)

- Permanent establishment (PE)