Learning Outcomes

This article outlines the assessment of costs in civil litigation under the CPR, including:

- The three principal methods of costs assessment (fixed, summary, detailed), their procedural triggers, and how to identify the correct method in typical SQE1-style fact patterns under the CPR and relevant Practice Directions

- The standard and indemnity bases of assessment, how proportionality operates on the standard basis, and the practical effect of the “any doubt” rule favouring either the paying or receiving party

- Preparation for summary assessment, the structure and timing of compliant statements of costs (N260), typical interim costs orders, and how these influence immediate recoverability of costs

- The detailed assessment process from notice of commencement to final certificate, including bills of costs, points of dispute and replies, provisional assessment, and the consequences of default or interim certificates

- Factors influencing the amount recoverable on assessment, including approved costs budgets (Precedent H), conduct, complexity, value, importance, and location, and how these are applied in exam scenarios

- Common pitfalls and sanctions, such as late or absent costs budgets, non-compliant or late N260s, and failures to engage with costs management directions

- High-level costs implications of Part 36 offers and qualified one-way costs shifting (QOCS) in personal injury claims, enabling accurate prediction of likely costs outcomes

SQE1 Syllabus

For SQE1, you are required to understand the assessment of costs in civil litigation under the CPR, with a focus on the following syllabus points:

- the distinction between fixed costs, summary assessment, and detailed assessment of costs

- when each method of costs assessment applies and the relevant procedural steps

- the difference between standard and indemnity basis for assessing costs

- the factors the court considers when determining the amount of recoverable costs

- the practical implications of costs management and budgeting in litigation

- common interim costs orders and the role of the statement of costs (N260)

- provisional assessment (paper assessment) and points of dispute in detailed assessment

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the main difference between summary assessment and detailed assessment of costs?

- When are fixed costs most commonly applied in civil litigation?

- What is the effect of costs being assessed on the indemnity basis rather than the standard basis?

- What must a party do to prepare for a summary assessment of costs at an interim hearing?

Introduction

In civil litigation, the allocation and quantification of legal costs is governed by the Civil Procedure Rules (CPR) and associated Practice Directions. The court may assess costs using three principal methods: fixed costs, summary assessment, and detailed assessment. Each method has its own rules, procedures, and practical consequences. Understanding these mechanisms is essential for advising clients, complying with procedural requirements, and maximising or limiting costs recovery. Costs management through budgets and budgeting orders now features prominently in multi-track and (from 2023) intermediate-track claims, and failures can lead to severe sanctions.

Detailed assessment of costs under the CPR is outlined from commencement to final costs certificate, including provisional and oral assessment.

Test Tip: In SQE-style questions on Fixed, summary, and detailed assessment of costs, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Fixed Costs

Fixed costs are predetermined sums set by the CPR for certain types of claims and procedural steps. They provide certainty and efficiency, especially in straightforward or lower-value cases.

Key Term: fixed costs

Fixed costs are set amounts recoverable for specific steps or types of claims, as prescribed by the CPR, regardless of the actual costs incurred.

Fixed costs most commonly apply in:

- small claims track cases (legal costs are generally limited to fixed commencement costs and specified disbursements such as court fees and expert’s fees)

- certain fast track personal injury claims (e.g. road traffic accidents) and other categories under Part 45

- specified actions where the CPR or a Practice Direction prescribes fixed sums (including many enforcement steps)

From 1 October 2023 the fixed recoverable costs (FRC) regime was extended by amendments to CPR Part 45 (Section VI for the fast track and Section VII for the intermediate track) to cover most money claims up to £100,000. On allocation to the fast track or the intermediate track the court assigns the claim to a complexity band (bands 1 to 4 in the intermediate track; bands 1 to 4 in the fast track), and the recoverable costs for each stage of the claim are then fixed by reference to that band and to the agreed or judicially determined value of the claim. Important categories fall outside the extended FRC regime and continue to be assessed in the usual way: mesothelioma and other asbestos-related lung disease claims, complex personal injury claims valued above £25,000 where clinical negligence or non-standard features arise, housing disrepair claims against social landlords, claims involving vulnerable parties or witnesses who would be significantly disadvantaged, and most claims allocated to the multi-track. Candidates are not expected to memorise tariff figures, but should recognise when the extended FRC regime displaces conventional summary or detailed assessment and should be able to identify a claim that falls within or outside its scope.

The amount recoverable is not subject to judicial discretion or assessment, except in limited circumstances. Fixed costs cover only the items specified; disbursements such as court fees or expert fees may be recoverable in addition.

Worked Example 1.1

A claimant wins a fast track road traffic accident claim worth £8,000. The CPR prescribes fixed costs of £1,500 for the pre-issue stage, £1,000 for post-issue work, and £1,000 for advocacy at trial. What is the total recoverable in fixed costs (excluding disbursements)?

Answer:

The claimant can recover £3,500 in fixed costs, regardless of the actual legal fees incurred.

Summary Assessment

Summary assessment is a quick, on-the-spot determination of costs by the judge, usually at the end of a hearing or trial lasting no more than one day.

Key Term: summary assessment

Summary assessment is the process by which the judge determines and orders payment of costs at the conclusion of a short hearing, based on a statement of costs.

Summary assessment is most commonly used:

- at the end of fast track trials

- after interim applications or hearings lasting one day or less

Key Term: statement of costs (N260)

A statement of costs (Form N260) sets out work done, time and rates, counsel’s fees, and disbursements. It must be served on the other party and lodged with the court in time for summary assessment.

The party seeking costs must prepare and serve a statement of costs (usually Form N260) on the other party and the court, typically at least 24 hours before the hearing. The judge will consider the statement, hear any objections, and order payment of a reasonable sum. Typical orders include “costs in any event,” “costs in the case,” “costs reserved,” “no order as to costs,” “wasted costs,” and “costs thrown away,” each with distinct effects (see PD 44).

Practical points:

- N260 must be complete and comprehensible; failure to serve in time may cause the court to adjourn costs or order detailed assessment instead of summary assessment.

- Payment is commonly ordered within 14 days, with interest accruing thereafter if unpaid.

- Summary assessment is not normally conducted where the hearing exceeds one day, where the information is inadequate, or where the receiving party is legally aided.

Worked Example 1.2

At the end of a one-day interim application, the judge invites the parties to address costs. The successful party has served a statement of costs totalling £2,000. The judge considers the work reasonable and orders the losing party to pay £2,000 within 14 days.

Answer:

The judge has made a summary assessment of costs, and the losing party must pay the amount ordered.

Worked Example 1.3

A claimant succeeds on a contested interim application but served their N260 only on the morning of the hearing. The judge finds the schedule inadequate to assess costs fairly there and then.

Answer:

The judge may decline summary assessment and order that costs be subject to detailed assessment, or make a “costs in the case”/“costs reserved” order. Late or inadequate N260s risk losing the benefit of immediate recovery.

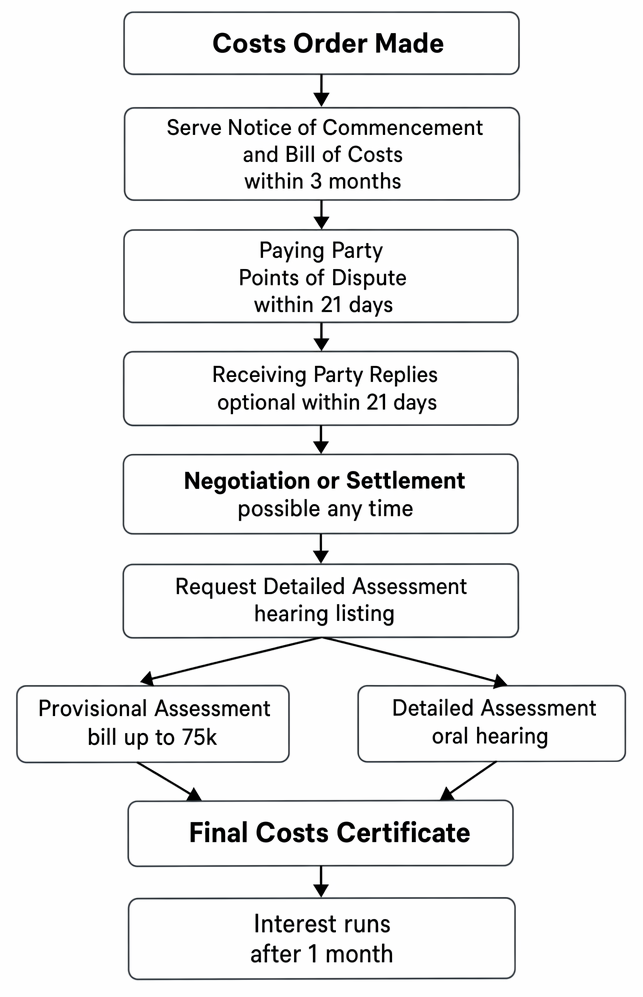

Detailed Assessment

Detailed assessment is a line-by-line scrutiny of a party’s bill of costs, usually conducted by a specialist costs judge after the conclusion of a multi-track trial or where summary assessment is not appropriate.

Key Term: detailed assessment

Detailed assessment is the process by which the court examines each item in a bill of costs to determine whether it was reasonably and proportionately incurred.

Detailed assessment is required:

- after multi-track trials (and intermediate-track trials where fixed costs do not apply)

- where the court orders costs to be assessed in detail

- for costs not subject to fixed costs or summary assessment

The process involves:

- the receiving party serving a notice of commencement and a detailed bill of costs on the paying party (within three months of the costs order)

- the paying party serving points of dispute within 21 days

- the receiving party replying to points of dispute if desired (usually within 21 days)

- if agreement is not reached, the court conducts assessment: paper (provisional) or oral hearing

Key Term: points of dispute

Points of dispute set out specific objections to items in the bill of costs. They should be clear, proportionate, and identify the basis for each challenge.

For bills of costs up to £75,000, the court may conduct a provisional assessment on paper without an oral hearing. Either party can seek an oral hearing within 21 days of the provisional decision, but if they fail to achieve an adjustment in their favour by at least 20%, they may be ordered to pay the costs of that hearing.

Modern practice expects electronic bills (Precedent S) for many cases, structured by phase, task, and activity (especially where budgeting applies). The court may also make a payment on account of costs following trial, with the precise amount to be determined later on detailed assessment.

Key Term: provisional assessment

Provisional assessment is a paper-based review by the court (usually for bills up to £75,000). Parties may request an oral hearing within 21 days, but must generally improve their position by at least 20% to avoid paying the costs of that hearing.

Worked Example 1.4

A claimant is awarded costs after a multi-track trial. Their bill of costs totals £120,000. The defendant disputes several items as excessive. At a detailed assessment hearing, the judge disallows £20,000 as unreasonable and orders the defendant to pay £100,000.

Answer:

The judge has conducted a detailed assessment and reduced the recoverable costs to £100,000.

Worked Example 1.5

The receiving party serves a bill totalling £58,000. Provisional assessment reduces the bill to £49,000. The paying party requests an oral hearing but achieves only a further £1,000 reduction.

Answer:

As the paying party did not improve its position by at least 20%, the court is likely to order the paying party to bear the costs of the oral hearing.

Standard and Indemnity Basis

The court will assess costs on either the standard or indemnity basis.

Key Term: standard basis

On the standard basis, only costs that are reasonable and proportionate are allowed, and any doubt is resolved in favour of the paying party. Key Term: indemnity basis

On the indemnity basis, only costs that are reasonable are allowed, and any doubt is resolved in favour of the receiving party. Proportionality is not required.

The standard basis is the default. Indemnity basis is used where the court disapproves of a party’s conduct (including, for example, unreasonable refusal to engage in ADR), or where there are contractual or other reasons. Part 36 costs consequences may direct indemnity basis for costs incurred after the expiry of the relevant period where the claimant obtains a judgment at least as advantageous as their offer.

On either basis, items can be disallowed if not reasonably incurred, or reduced if unreasonable in amount. On the standard basis, proportionality can further reduce otherwise reasonable costs.

Worked Example 1.6

A defendant has acted unreasonably throughout proceedings. The judge orders costs against the defendant on the indemnity basis. The claimant claims £50,000. The judge finds all items reasonable and allows the full amount.

Answer:

On the indemnity basis, the claimant recovers £50,000, as all costs claimed are reasonable and any doubt is resolved in their favour.

Worked Example 1.7

The claimant beats their own Part 36 offer at trial. The court applies the Part 36 costs consequences from the expiry of the relevant period.

Answer:

The claimant will ordinarily recover costs on the indemnity basis from expiry of the relevant period, together with interest on damages and on costs (subject to the justice of the case) and potentially an additional amount, capped by CPR 36.17.

Factors Considered in Assessment

When assessing costs, the court considers:

- the conduct of the parties before and during proceedings (including engagement with ADR)

- the value and complexity of the case

- the importance of the matter to the parties

- the skill, effort, and time involved

- approved costs budgets (in multi-track and intermediate-track cases)

- the place and circumstances in which work was done (regional rates and overheads)

Approved budgets influence recoverable costs. Where a costs management order is in place, the court will not depart from the last approved/ agreed budgeted costs on assessment unless satisfied there is a good reason to do so (for example, significant developments). Proportionality still applies to standard-basis assessment.

Key Term: costs budget

A costs budget (Precedent H) sets out incurred costs and estimates for future phases. Approved budgets guide recovery and require “good reason” for departure on assessment.

The court will disallow or reduce costs that are unreasonable or disproportionate.

Exam Warning: If a party fails to file a required costs budget on time in a multi-track case, the court may restrict recovery to court fees only unless relief from sanctions is granted. This can have severe consequences for costs recovery.

Worked Example 1.8

The claimant’s budget was due 21 days before the first case management conference but was filed late without good reason. The claim proceeds and the claimant wins at trial.

Answer:

Absent relief from sanctions, the claimant will be treated as having a budget limited to court fees only, drastically restricting recovery of costs despite success at trial.

Additional Practical Points on Costs

- Interest on costs: the court can award interest on assessed costs. In the High Court, interest is frequently awarded under s.17 Judgments Act 1838; for County Court judgments, interest is governed by s.74 County Courts Act 1984 and related Orders. Interest generally runs from the date of the costs order or judgment, subject to discretion.

- Payment on account of costs: after trial, courts often order a reasonable payment on account pending detailed assessment to avoid undue delay.

- Default and interim certificates: where points of dispute are not served in time, a default costs certificate can be obtained for the full amount claimed. Where much of the bill is agreed, interim certificates can be issued for the undisputed balance pending final assessment.

Summary

| Assessment Method | When Used | Who Assesses | Key Features |

|---|---|---|---|

| Fixed Costs | Prescribed claims/steps | N/A | Set by CPR; no discretion; certainty |

| Summary Assessment | Short hearings/fast track trials | Judge | Immediate; based on statement of costs |

| Detailed Assessment | Multi-track/complex cases | Costs judge | Item-by-item scrutiny; may be lengthy |

Key Point Checklist

This article has covered the following key knowledge points:

- Fixed costs are set amounts recoverable for certain claims or steps, regardless of actual costs.

- Summary assessment is a quick determination of costs by the judge at the end of a short hearing or fast track trial; a compliant N260 must be served in time.

- Detailed assessment is a thorough, item-by-item review of costs, usually after multi-track trials, following notice of commencement, points of dispute, replies, and assessment (including provisional assessment for bills up to £75,000).

- Costs are assessed on the standard basis (default, proportionality applies) or indemnity basis (no proportionality; any doubt favours the receiving party).

- Approved costs budgets (Precedent H) influence recovery; departure requires “good reason.”

- Typical interim costs orders include “costs in any event,” “costs in the case,” “costs reserved,” and “no order as to costs”; interest and time to pay (often 14 days) are common features.

- Part 36 offers have specific cost consequences; beating your own offer can trigger indemnity basis and interest consequences from the end of the relevant period.

- In personal injury, QOCS limits a defendant’s recovery of costs from a losing claimant, subject to exceptions (e.g. fundamental dishonesty).

- Failure to comply with procedural requirements (such as filing costs budgets or serving N260) can severely limit or postpone costs recovery.

- Default and interim costs certificates provide mechanisms to secure payment where appropriate; electronic bills (Precedent S) are commonly used for detailed assessment.

Key Terms and Concepts

- fixed costs

- summary assessment

- statement of costs (N260)

- detailed assessment

- points of dispute

- provisional assessment

- standard basis

- indemnity basis

- costs budget