Learning Outcomes

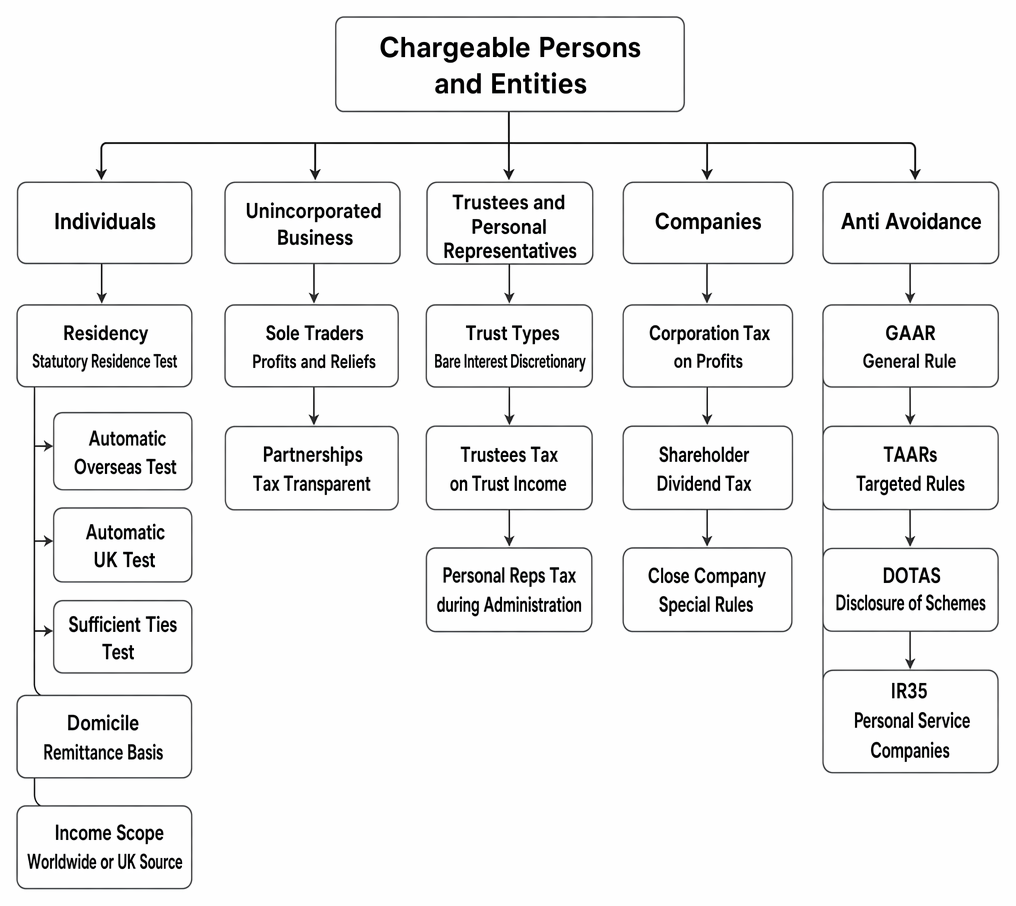

This article outlines the different persons and entities that are subject to income tax in the UK. It covers the basis of charge for individuals, including the importance of residency status and the role of the Statutory Residence Test (SRT), and contrasts this with the taxation of unincorporated businesses like sole traders and partnerships (including limited liability partnerships (LLPs), which are tax transparent in most cases). The liability of trustees across key trust types and personal representatives is addressed, alongside the distinction between income tax and corporation tax for companies. It also clarifies points where corporate partners and corporate trustees are taxed under the corporation tax regime rather than income tax. Understanding these distinctions, the scope of UK-source versus worldwide income, and how profit shares in partnerships flow through to individual partners is essential for identifying the correct taxpayer and the scope of their liability for the SQE1 assessment.

SQE1 Syllabus

For SQE1, you are required to understand the different types of persons and entities chargeable to income tax and the basis of their liability. This involves distinguishing between individuals, unincorporated businesses, trusts, and companies, with a focus on the following syllabus points:

- Identifying the main categories of persons and entities subject to UK income tax.

- Understanding the significance of residency and domicile status for individuals' tax liability, including the SRT and UK-source versus worldwide income.

- Recognising how sole traders and partners are taxed on their business profits, and that LLPs are generally tax transparent for income tax.

- Distinguishing the income tax liability of trustees across bare, interest in possession, and discretionary trusts, and the position of personal representatives.

- Understanding the fundamental difference between income tax (for individuals, individual partners, trustees, PRs) and corporation tax (for companies and corporate partners).

- Appreciating that corporate partners and corporate trustees are chargeable to corporation tax, not income tax, on their profits.

- Noting the current tax-year basis for assessing trading income and how loss relief principles operate for unincorporated businesses.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following entities typically pays Corporation Tax on its profits in the UK?

- a) Sole trader

- b) General partnership

- c) Private limited company

- d) Trustee of a discretionary trust

-

An individual's liability to UK income tax on their worldwide income primarily depends on which of the following statuses?

- a) Nationality

- b) Domicile

- c) Residency

- d) Citizenship

-

True or False? Partners in a general partnership are taxed individually on their respective shares of the partnership profits.

Introduction

Understanding who is liable to pay income tax is a fundamental aspect of UK tax law. Different rules apply depending on whether the taxpayer is an individual, a partnership, a trustee, or another type of entity. For the SQE1 assessment, you must be able to identify the chargeable person or entity in a given scenario and understand the basis on which their income tax liability arises. This article provides an overview of the key distinctions.

Chargeable persons and entities for UK income tax, including individuals, partnerships, trustees, companies, and anti-avoidance provisions.

Key Term: Income Tax

A tax levied by the UK government on the income of individuals and certain other legal entities, including trustees and personal representatives. Key Term: Chargeable Person

An individual or entity liable to pay income tax under UK legislation. The main categories are individuals (including sole traders and individual partners), trustees and personal representatives. Key Term: UK-source income

Income treated as arising in the UK for tax purposes (for example, UK employment income for duties performed in the UK, profits of a trade carried on wholly or partly in the UK, and rental income from UK land).

Income liable to income tax includes, broadly, employment income, trading (self-employment) income, property income, savings income (interest), and dividend income. The extent of the charge (worldwide or UK-source only) depends principally on residence status; domicile can further affect the taxation of foreign income for certain UK residents.

Individuals

Individuals are the most common category of taxpayer subject to income tax. Their liability depends significantly on their residence and domicile status, and on whether the income is UK-source or foreign-source.

Residency Status

An individual's residence status determines the scope of their UK income tax liability.

Key Term: Residency

An individual's tax status based on their connection to the UK during a tax year, determined by the Statutory Residence Test (SRT). UK residents are generally taxed on their worldwide income. Non-UK residents are typically taxed only on their UK-source income. Key Term: Statutory Residence Test (SRT)

A legislative framework used to determine an individual's UK tax residence status based on days spent in the UK and other connecting factors ('ties'), including automatic overseas tests, automatic UK tests, and sufficient ties tests.

The SRT comprises:

- Automatic UK tests (for example, being present in the UK for 183 days or more in a tax year; having the only home located and used in the UK; or working full-time in the UK for sufficient periods).

- Automatic overseas tests (for example, being present in the UK for very limited days where particular conditions apply and working full-time overseas).

- Sufficient ties tests where neither automatic test is met, combining day counts and UK ties such as accommodation, family, and substantive UK work.

Two additional points that commonly arise:

- Split-year treatment may apply in scenarios of arrival in or departure from the UK mid-year, dividing the tax year into a UK-resident part and a non-resident part for income tax purposes.

- Double tax treaties may affect the final outcome where dual residence arises; treaty “tie-breaker” rules can allocate residence to one state, altering the scope of UK taxation on foreign income.

Key Term: UK-source employment and trading income

Employment income relating to duties performed in the UK and profits of a trade carried on wholly or partly in the UK; both are generally chargeable to UK income tax irrespective of the taxpayer’s residence.

Domicile Status

Domicile is a concept distinct from residence, relating to an individual's long-term 'home'. While UK resident individuals are usually taxed on worldwide income, those who are UK resident but not domiciled in the UK ('non-doms') may, subject to conditions, claim to be taxed on the remittance basis for foreign income and gains. This means they are only taxed on foreign income/gains brought into ('remitted') the UK, rather than on the arising basis. The remittance basis can have significant consequences and historically could involve an annual charge after a sustained period of UK residence, so care is needed before making (or maintaining) such a claim.

Key Term: Domicile

A general law concept indicating an individual's permanent home, the country they consider their homeland. It is distinct from nationality or residence. Key Term: Remittance basis

An optional basis for certain UK resident, non-domiciled individuals, under which foreign income and gains are taxable in the UK only if remitted to the UK. Claiming the remittance basis can affect entitlement to allowances and may involve charges depending on the length of UK residence.

Worked Example 1.1

Freya is a German citizen who came to the UK for a two-year work contract. In the 2023/24 tax year, she spent 210 days in the UK. She retains a home in Germany and intends to return there after her contract ends. Is Freya likely to be liable for UK income tax on income she earns from investments held outside the UK?

Answer:

Yes, Freya is likely a UK resident for the 2023/24 tax year under the SRT because she spent more than 183 days in the UK. As a UK resident, she is generally liable for UK income tax on her worldwide income, including the foreign investment income. Her non-UK domicile status might allow her to elect for the remittance basis, but this would need further investigation based on her specific circumstances and potential charges.

Worked Example 1.2

Raj lives in India and visits the UK frequently for business. In 2024/25 he spends 60 days in the UK, performs some duties here over multiple trips, and invoices UK clients. He is non-UK resident. What UK income is chargeable?

Answer:

As a non-UK resident, Raj is taxed on UK-source income only. UK employment duties performed in the UK are taxable in the UK. Profits from a trade carried on wholly or partly in the UK are UK-source and chargeable. His foreign investment income is outside UK income tax if unconnected with UK-source income. Treaty relief may apply to moderate or relieve double taxation.

Worked Example 1.3

Laura is UK resident but not domiciled in the UK. She receives foreign dividends and interest that she keeps entirely offshore. Later, she transfers a portion to a UK bank. Which amounts are within the UK charge?

Answer:

On the remittance basis (if validly claimed), Laura is taxed on foreign income to the extent she remits it to the UK. Foreign amounts retained offshore are not taxed in the UK under the remittance basis. Once she transfers funds derived from foreign income into the UK, the remitted amount becomes taxable in the UK.

Unincorporated Businesses

Unincorporated businesses, such as sole traders and partnerships, are not taxed as separate entities. Instead, the individuals who own the business are taxed. Corporate partners are charged to corporation tax on their profit shares.

Sole Traders

A sole trader is an individual running a business on their own account. They are treated as self-employed for tax purposes and must register with HM Revenue & Customs (HMRC) and file returns under self-assessment.

Key Term: Sole trader

An individual conducting business on their own account. The trade’s profits are charged to income tax on the individual.

- Tax Liability: Sole traders pay income tax on their business profits (calculated as trading income less deductible expenses and capital allowances). They also pay Class 2 and Class 4 National Insurance contributions (NICs), separate from income tax.

- Basis of assessment: Trading income is now assessed on a tax-year basis. Transitional rules applied around the change to the tax-year basis to move away from pure “current year” basis computations aligned to accounting dates; always check the applicable tax year position.

- Losses: Trading losses can be relieved in various ways (for example, against other income in the same or prior year subject to statutory conditions, carry-forward against future profits of the same trade, or special reliefs for terminal losses). The detailed mechanics are beyond the scope here, but the fact and availability of loss reliefs is important.

Partnerships

Partnerships (including general partnerships under the Partnership Act 1890 and Limited Liability Partnerships (LLPs) under the Limited Liability Partnerships Act 2000) are generally 'tax transparent'.

Key Term: Partnership

A relationship between persons carrying on a business in common with a view of profit (Partnership Act 1890). For tax, profits are allocated to individual partners who pay income tax on their shares. Corporate partners pay corporation tax. Key Term: LLP (Limited Liability Partnership)

An incorporated entity with separate legal personality. For UK tax, an LLP carrying on a commercial business with a view to profit is generally treated as a partnership, so members are taxed on their shares of profit (individual members under income tax; corporate members under corporation tax).

- Tax Liability: The partnership computes its profits under income tax rules, but the entity itself does not pay income tax. Each individual partner includes their share of the partnership profit (or loss) in their personal income tax calculation. Corporate partners are taxed under corporation tax on their shares. The LLP, while enjoying separate legal personality under company law, is generally tax transparent for income tax if carrying on a business with a view to profit.

- Profit Shares: Profit shares are determined by the partnership agreement or, by default, shared equally. Partners may receive priority profit shares, salaries (for accounting allocation only), or interest on capital; ultimately, each partner’s taxable share follows the allocation of taxable profits, not necessarily the cash received.

- Basis of assessment: As with sole traders, the tax-year basis applies to members’ trading shares. Transitional rules may be relevant where accounting dates do not align neatly with the tax year.

- Losses: Loss relief is available to individual partners subject to statutory restrictions and anti-avoidance limits (for example, restrictions on relief where trade is not commercial).

Worked Example 1.4

Amara and Ben are equal partners in an architectural firm with £200,000 taxable profits for the tax year. Amara is an individual; Ben is a company. How are the profits taxed?

Answer:

The firm is tax transparent. Amara includes her £100,000 share in her income tax computation. Ben’s corporate partner includes its £100,000 share in the company’s corporation tax computation. The partnership itself does not pay tax.

Worked Example 1.5

An LLP with three individual members makes a taxable profit of £150,000. The LLP agreement provides that Member A receives a fixed profit share of £60,000, with the balance split equally. What is the tax treatment?

Answer:

The LLP computes the taxable profit of £150,000. Member A is allocated £60,000; the remaining £90,000 is split equally (£30,000 each to Members B and C). Each individual member is taxed under income tax on their allocated share. The LLP does not itself pay income tax.Exam Warning: Do not confuse the tax treatment of partnerships and LLPs with that of companies. Partnerships and LLPs (where trading with a view of profit) are tax transparent; the partners/members pay tax on their shares. Companies pay Corporation Tax on their profits.

Trustees and Personal Representatives

Trustees and personal representatives may be liable to income tax on income arising from the assets they manage. The type of trust affects who is taxed and at what rates.

Key Term: Trustee

A person or entity holding assets ('trust property') for the benefit of others ('beneficiaries') under the terms of a trust. Key Term: Bare trust

A simple trust under which the beneficiary is absolutely entitled to both capital and income; the beneficiary is treated as receiving the income directly and is taxed accordingly. Key Term: Interest in possession trust

A trust where a beneficiary has a present right to trust income as it arises (for example, a life tenant). Trustees are chargeable on certain income; income paid to the beneficiary is then taxed on the beneficiary with credit as appropriate. Key Term: Discretionary trust

A trust where trustees have discretion over which beneficiaries receive income and when. Trustees are generally charged at trust rates on income retained or distributed, with beneficiaries typically receiving income with a tax credit attached that they may reclaim or set off depending on their personal rates. Key Term: Personal Representative

An executor appointed by will or an administrator appointed under law, responsible for administering a deceased person’s estate during the administration period.

- Trustees: Trustees pay income tax on income generated by trust assets (e.g., rental income, interest, certain dividends) at rates applicable to trusts (with special rules for dividends and savings income). The detailed bands and rates change periodically; the general position is that discretionary trust income is often charged at higher trust rates. For bare trusts, the beneficiary, not the trustee, is assessed. For interest in possession trusts, trustees may account for tax on income and beneficiaries are then taxed on income distributions, typically with credits.

- Personal Representatives: Personal representatives are liable to income tax on income arising in the administration period, generally at basic rates. Beneficiaries are taxed on income distributed to them from the estate according to their own rates. Special reporting and payment rules apply during the estate administration.

Worked Example 1.6

A discretionary trust receives £10,000 of bank interest and distributes £6,000 to beneficiary D, retaining the rest. Who is taxed?

Answer:

Trustees are liable for income tax at the trust rate on the interest. The £6,000 distributed to D typically carries a tax credit representing tax accounted for by the trustees; D will include the grossed-up amount in their income and can reclaim any excess credit (or pay further tax) depending on D’s personal tax position. The retained income remains taxed at trustee rates.

Companies

Companies incorporated under the Companies Act 2006 are distinct legal entities and are subject to a different tax regime.

Key Term: Company

A legal entity incorporated under the Companies Act 2006, having separate legal personality from its owners (shareholders) and managers (directors). Key Term: Corporation Tax

The tax levied on the profits and chargeable gains of companies and other corporate bodies resident in the UK.

- Tax Liability: Companies pay Corporation Tax on their profits (including trading profits, investment income, and chargeable gains), not income tax. Corporate partners in partnerships are likewise within corporation tax on their shares of profits.

- Shareholders: Individual shareholders pay income tax on dividends received from the company, subject to the dividend allowance and specific dividend tax rates.

- Directors/Employees: Directors and employees receiving salaries or benefits from the company pay income tax on these earnings through the PAYE system. NICs may also be due.

- Close companies: Certain anti-avoidance provisions apply (for example, tax charges on loans to participators) within the corporation tax regime. These points underline the distinction between income tax on individuals and corporation tax on companies.

Revision Tip: For SQE1, clearly distinguishing between entities liable for Income Tax (individuals, individual partners, trustees, PRs) and those liable for Corporation Tax (companies, corporate partners) is fundamental. Ensure you can identify the correct taxpayer in any given scenario.

Key Point Checklist

This article has covered the following key knowledge points:

- Income tax is primarily levied on individuals, including sole traders and individual partners; trustees and personal representatives are also chargeable persons.

- UK residence (determined by the SRT) generally brings worldwide income within UK income tax; non-residents are typically chargeable on UK-source income only.

- Domicile is distinct from residence. UK resident non-doms may claim the remittance basis for foreign income and gains, subject to conditions and consequences.

- Sole traders pay income tax on business profits and are assessed on a tax-year basis; loss reliefs exist in statute for trading losses.

- Partnerships and trading LLPs are tax transparent; individual partners pay income tax on their shares of profits, and corporate partners pay corporation tax on theirs.

- Trustees’ income tax liability depends on trust type (bare, interest in possession, discretionary). Personal representatives are taxed on estate income arising during administration, generally at basic rates.

- Companies are separate legal entities subject to Corporation Tax on their profits; shareholders pay income tax on dividends; directors/employees are charged under PAYE on employment income.

- Always identify the correct chargeable person: the individual partner, the trustee, the personal representative, or the company, as appropriate.

Key Terms and Concepts

- Income Tax

- Chargeable Person

- UK-source income

- Residency

- Statutory Residence Test (SRT)

- UK-source employment and trading income

- Domicile

- Remittance basis

- Sole trader

- Partnership

- LLP (Limited Liability Partnership)

- Trustee

- Bare trust

- Interest in possession trust

- Discretionary trust

- Personal Representative

- Company

- Corporation Tax