Learning Outcomes

This article outlines the main categories of loss recoverable in the tort of negligence: physical damage, economic loss, and psychiatric harm. For the SQE1 assessments, you will need to distinguish between these types of loss and understand the specific legal principles governing their recoverability. This includes differentiating between consequential and pure economic loss, and between primary and secondary victims in psychiatric harm cases. Your understanding will enable you to apply these rules to SQE1-style single best answer questions. In addition, you should be able to relate the recoverability of loss to general negligence principles of duty, breach, causation and remoteness (including “but for” and foreseeability), appreciate how the eggshell skull rule can increase the scope of recoverable damage, identify the sudden shock and proximity requirements in psychiatric harm, and recognise when a defendant may be liable for pure economic loss in negligent misstatement or service provision scenarios due to assumption of responsibility and reasonable reliance.

SQE1 Syllabus

For SQE1, you are required to understand how different types of loss are categorised and treated within the tort of negligence. This knowledge is fundamental for advising clients on the potential recoverability of damages, with a focus on the following syllabus points:

- The distinction between physical damage to person or property and other forms of loss.

- The difference between consequential economic loss (generally recoverable) and pure economic loss (generally irrecoverable, subject to exceptions).

- The specific requirements for establishing liability for psychiatric harm, including the distinction between primary and secondary victims and the relevant control mechanisms.

- How these principles apply in practice to factual scenarios.

- The role of causation and remoteness across all types of loss (including the “but for” test and foreseeability of damage).

- The sudden shock requirement and the need for proximity in time, space and perception in secondary victim claims.

- The scope of negligent misstatement liability, focusing on assumption of responsibility, reasonable reliance, and the effect of disclaimers.

- The treatment of rescuers, anxiety-only claims, and property-only psychiatric harm cases, and where these succeed or fail.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which type of loss is generally NOT recoverable in the tort of negligence?

- a) Personal injury.

- b) Damage to the claimant's property.

- c) Pure economic loss.

- d) Consequential economic loss.

-

A claimant suffers psychiatric harm after witnessing a horrific accident caused by the defendant's negligence but was not themselves in any physical danger. Which category of victim are they likely to be classified as?

- a) Primary victim.

- b) Secondary victim.

- c) Bystander victim (not a legal category).

- d) Consequential victim.

-

True or false? Financial loss directly resulting from physical damage to the claimant's property is classified as pure economic loss.

Introduction

In the tort of negligence, establishing that the defendant owed a duty of care, breached that duty, and caused damage is essential. However, not all types of damage or loss suffered by a claimant are treated equally by the law. The courts have developed distinct rules based on the type of loss sustained. For the SQE1 assessment, you need to identify the type of loss presented in a scenario and apply the correct legal principles to determine recoverability.

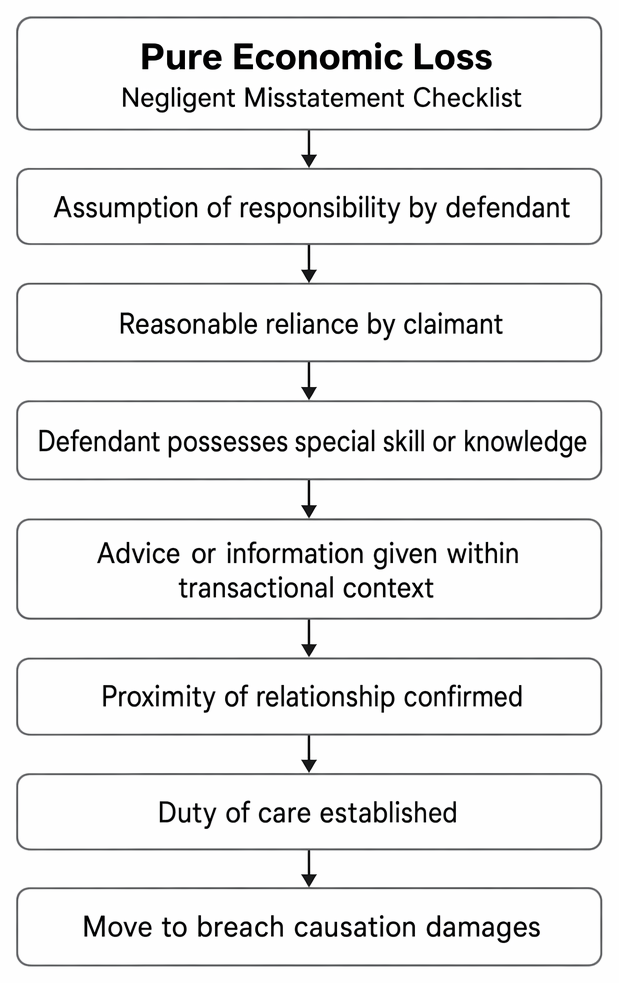

Pure economic loss in negligent misstatement is presented as a checklist of the elements relevant to establishing a duty of care.

The main categories of loss are:

- Physical damage (to the person or property).

- Economic loss (financial loss).

- Psychiatric harm (recognised mental injury).

This article explores each category, highlighting the key rules and distinctions essential for your exam preparation. Across all categories, causation and remoteness principles must be satisfied: the breach must be a factual cause of the loss (“but for” the breach, the loss would not have occurred), and the type of damage must be reasonably foreseeable (The Wagon Mound (No 1) [1961] AC 388). Vulnerabilities of the claimant are taken as they are found under the eggshell skull rule, which can increase the extent of recoverable damage even when the extent was not foreseeable.

Physical Damage

This is the most straightforward type of loss. It encompasses:

- Personal Injury: Physical harm to the claimant's body, ranging from minor injuries to serious disablement or death. This includes consequential financial losses like lost earnings or medical expenses.

- Property Damage: Damage to or destruction of the claimant's tangible property (e.g., car, house, goods). This includes consequential financial losses, such as the cost of repairs or lost profits resulting directly from the property damage.

Generally, if a claimant suffers physical damage due to the defendant's negligence, and the requirements of duty, breach, and causation are met, the loss is recoverable, subject to the rules on remoteness (The Wagon Mound (No 1) [1961] AC 388). The foreseeability required is of the kind of damage, not its precise mechanism. For example, if physical injury from a road collision is foreseeable, the defendant can be liable even where the particular consequences suffered by the claimant are unusual or severe because of a pre-existing condition.

Key Term: Eggshell Skull Rule

A defendant must take the claimant as they find them. If the claimant has a particular susceptibility that makes the injury more serious or causes unexpected consequences, the defendant is liable for the full extent of that injury, even if the extent was not foreseeable.

In assessing recoverability of physical damage, the court will consider:

- Causation in fact (“but for” the breach, would the damage have occurred?).

- Intervening acts (only if there is a new, independent cause that breaks the chain of causation).

- Remoteness (is the type of damage reasonably foreseeable?).

Where physical damage is established, consequential financial losses (lost earnings, cost of care, repair costs) are usually recoverable as consequential economic loss.

Worked Example 1.1

Lia has a mild, undiagnosed blood disorder. A negligent driver bumps her car at low speed. Lia suffers unusually severe internal bleeding and requires prolonged hospital treatment and time off work.

Answer:

Personal injury is a type of damage that is readily recoverable in negligence provided duty, breach, causation and remoteness are satisfied. Given that physical injury from a car collision was foreseeable, the eggshell skull rule means the defendant is liable for the full extent of Lia’s injuries and consequential losses even though the severity was not foreseeable.

Economic Loss

Economic loss refers to financial detriment suffered by the claimant. Tort law draws a key distinction between consequential economic loss and pure economic loss.

Consequential Economic Loss

This is financial loss that is a direct consequence of physical damage to the claimant's person or property.

Key Term: Consequential Economic Loss

Financial loss that results directly from physical injury to the claimant or physical damage to the claimant’s property.

Examples include lost earnings due to personal injury, or lost profits because a damaged machine cannot operate. Consequential economic loss is generally recoverable in negligence, provided it is not too remote.

Pure Economic Loss

This is financial loss that is not consequent upon physical damage to the claimant's own person or property.

Key Term: Pure Economic Loss

Financial loss suffered by a claimant that does not flow directly from physical injury to their own person or physical damage to their own property.

Pure economic loss includes:

- Loss caused by damage to the property of a third party (e.g., loss of profit due to power cut caused by damage to a cable owned by the electricity company - Spartan Steel & Alloys Ltd v Martin & Co (Contractors) Ltd [1973] QB 27).

- Loss arising from acquiring a defective product or property (e.g., the cost of repairing a defective item itself, or the reduction in its value - Murphy v Brentwood District Council [1991] 1 AC 398).

- Other financial loss unrelated to physical damage (e.g., loss on an investment made after relying on negligent advice).

General Rule: Pure economic loss is generally not recoverable in negligence. The courts restrict liability to avoid imposing potentially "crushing liability" on defendants (Caparo Industries plc v Dickman [1990] 2 AC 605).

Exceptions: There are limited exceptions where a duty of care may be owed in respect of pure economic loss, primarily:

- Negligent Misstatement: Where there is a "special relationship" between the claimant and defendant involving an assumption of responsibility by the defendant and reasonable reliance by the claimant (Hedley Byrne & Co Ltd v Heller & Partners Ltd [1964] AC 465).

- Negligent Provision of Services: Extended from negligent misstatement, where professionals providing services assume responsibility towards those foreseeably relying on their work (e.g., Henderson v Merrett Syndicates Ltd [1995] 2 AC 145; White v Jones [1995] 2 AC 207).

Key Term: Negligent Misstatement

Liability arising from a careless statement or advice causing pure economic loss where a special relationship exists, often demonstrated by assumption of responsibility by the defendant and reasonable reliance by the claimant. Key Term: Assumption of Responsibility

A defendant may owe a duty for pure economic loss if they undertake responsibility toward the claimant, expressly or impliedly, in circumstances where the claimant’s reliance is reasonable.

Disclaimers may negate assumption of responsibility if clearly communicated and effective. In consumer contexts, the fairness controls under the Consumer Rights Act 2015 apply; in business contexts, exclusion clauses may be scrutinised under the Unfair Contract Terms Act 1977. Whether a disclaimer is effective is context-sensitive.

Duty in negligent misstatement also requires that reliance was both actual and reasonable. The defendant must foresee that the claimant, or a group to which the claimant belongs, would rely on the statement for the particular purpose (cf. Caparo and auditors’ duties to investors at large).

Exam Warning: Be careful to distinguish between consequential economic loss (generally recoverable) and pure economic loss (generally irrecoverable). Identify whether the financial loss stems directly from damage to the claimant's own person or property. If not, it is likely pure economic loss, and recovery will depend on establishing an exception like negligent misstatement.

Worked Example 1.2

A contractor negligently severs a power cable belonging to an electricity board. A steel factory loses power for 14 hours. During that period, it suffers:

- physical damage to steel in the furnace (scrapped stock),

- profit lost on that scrapped steel,

- profit that would have been made on future melts that could not be processed during the outage.

Answer:

The physical damage to the steel is recoverable as property damage. The lost profit on the scrapped steel is recoverable as consequential economic loss. The future profits on the melts that could not be processed are pure economic loss caused by damage to a third party’s cable and are not recoverable (Spartan Steel).

Worked Example 1.3

A homeowner discovers eleven years after purchase that the house’s raft base was defective. There is extensive cracking. The local authority had negligently approved the base design. The homeowner sells at a substantial loss and seeks to recover that reduction in value.

Answer:

The reduction in sale value or cost of repair to the defective building itself is treated as pure economic loss where there has been no damage to other property or personal injury. A duty to avoid such loss is generally not owed in negligence (Murphy v Brentwood DC). The claim fails.

Worked Example 1.4

A bank provides a favourable credit reference about a company to an advertising agency. The agency relies on it and extends credit to the company, which collapses. The bank had added a clear disclaimer that it accepted no responsibility for the reference.

Answer:

Pure economic loss caused by negligent misstatement can be recoverable where there is an assumption of responsibility and reasonable reliance (Hedley Byrne). A clear disclaimer may negate assumption of responsibility and defeat the claim. Whether the disclaimer is effective depends on clarity, communication, and relevant statutory controls.

Psychiatric Harm

Psychiatric harm refers to medically recognised psychiatric illnesses (e.g., post-traumatic stress disorder (PTSD), pathological grief, severe depression) caused by the defendant's negligence. Mere grief, distress, or anxiety is generally not sufficient.

Key Term: Psychiatric Harm

A medically recognised psychiatric illness sustained by the claimant as a result of the shock of an event caused by the defendant's negligence. Key Term: Sudden Shock

A sudden, horrifying event or its immediate aftermath that violently agitates the mind; psychiatric illness caused by gradual accumulation of stress is generally not actionable for secondary victims.

The law imposes strict control mechanisms to limit liability, primarily distinguishing between primary and secondary victims (Alcock v Chief Constable of South Yorkshire Police [1992] 1 AC 310). The requirement of “sudden shock” is applied to secondary victims. There must be proximity in relationship, time and space, and perception. The immediate aftermath requirement may extend beyond the scene where the claimant encounters a seamless sequence of events (see McLoughlin v O’Brian [1983] 1 AC 410; Galli-Atkinson v Seghal [2003] EWCA Civ 697), but watching on television normally fails (Alcock).

Primary Victims

These are individuals directly involved in the incident caused by the defendant's negligence, who were within the zone of foreseeable physical danger (or reasonably believed themselves to be).

Key Term: Primary Victim

A person who suffers psychiatric harm resulting from reasonable fear for their own physical safety caused by the defendant’s negligence, being within the zone of potential physical danger.

Rule: A primary victim can recover damages for psychiatric harm provided that physical injury was reasonably foreseeable, even if no physical injury actually occurred (Page v Smith [1996] AC 155). It is not necessary to show that psychiatric harm itself was foreseeable. The defendant must take the victim as they find them (eggshell skull rule applies).

Worked Example 1.5

Ahmed is involved in a minor car collision caused entirely by Ben's negligent driving. Ahmed is physically unharmed but, due to the shock of the near-miss, develops severe PTSD, diagnosed by a psychiatrist. Physical injury to Ahmed was reasonably foreseeable given the nature of the collision.

Can Ahmed claim for his PTSD?

Answer:

Yes. Ahmed is a primary victim as he was directly involved and physical injury was foreseeable. Provided his PTSD is a medically recognised psychiatric illness caused by the shock of the incident, he can recover damages, even if psychiatric harm was not specifically foreseeable (Page v Smith).

Secondary Victims

These are individuals who suffer psychiatric harm as a result of witnessing harm to others or fearing for the safety of others, but who were not themselves within the zone of physical danger.

Key Term: Secondary Victim

A person who suffers psychiatric harm as a result of witnessing injury to others or fearing for the safety of others, caused by the defendant’s negligence, but who was not within the zone of foreseeable physical danger themselves.

Rule: Recovery for secondary victims is tightly controlled by the Alcock criteria. The claimant must prove:

- Foreseeability of Psychiatric Harm: It was reasonably foreseeable that a person of 'normal fortitude' would suffer psychiatric illness in the circumstances.

- Proximity of Relationship: A close tie of love and affection with the immediate victim of the accident (presumed for spouses, parents/children; must be proven otherwise).

- Proximity in Time and Space: Presence at the scene of the accident or its immediate aftermath.

- Proximity of Perception: Witnessing the event or its aftermath with their own unaided senses (not via television, unless live broadcast of identifiable individuals in exceptional circumstances).

All four criteria must be met.

Worked Example 1.6

Chloe witnesses her sister being seriously injured in a horrific accident caused by David's negligence. Chloe was standing safely on the pavement across the street. She develops a recognised psychiatric illness as a result of the shock.

Can Chloe claim as a secondary victim?

Answer:

Potentially. Chloe must satisfy the Alcock criteria. Psychiatric harm to a person of normal fortitude witnessing such an event is likely foreseeable. As sisters, a close tie of love and affection may need to be proven (it's not automatically presumed like parent/child). Chloe was present at the scene (proximity in time/space) and witnessed it with her own senses (proximity of perception). If she can prove the close tie, her claim may succeed. Secondary victim claims often turn on proximity. If the claimant arrives at a hospital some hours later and sees the victim, the chain may be too remote unless the visit forms an uninterrupted, proximate sequence with the accident.

Worked Example 1.7

Omar arrives at the accident scene minutes after his partner’s collision and sees her trapped in the vehicle; he then follows the rescue to the hospital and witnesses resuscitation attempts. He develops a recognised psychiatric illness.

Answer:

This can fall within “immediate aftermath” where the claimant experiences a seamless, proximate sequence from accident scene to hospital (McLoughlin; Galli-Atkinson). If the Alcock criteria are satisfied (including close ties and perception with unaided senses), recovery may be possible.

Rescuers and other categories

Rescuers are not automatically primary or secondary victims. To recover, a rescuer must either be within the zone of physical danger (primary victim) or satisfy the Alcock criteria (secondary victim). Merely witnessing distress and helping, without danger to oneself, is not enough (White v Chief Constable of South Yorkshire Police [1999] 2 AC 455).

Property-only psychiatric harm has, in limited circumstances, been recognised (Attia v British Gas plc [1988] QB 304), where a claimant suffers a medically recognised psychiatric illness after witnessing the destruction of their own home. Anxiety alone without psychiatric illness is insufficient; anxiety about future disease does not constitute damage (Rothwell v Chemical & Insulating Co Ltd [2007] 3 WLR 876).

In some cases, unwitting participants who reasonably believe they caused another’s death or injury can recover (Dooley v Cammell Laird & Co Ltd [1951] 1 Lloyd’s Rep 271), though claims fail where belief is not reasonably held (Monk v PC Harrington Contractors Ltd [2008] EWHC 1879).

Assumption of responsibility can arise in special relationships where psychiatric injury is foreseeable (e.g., custodial settings). For example, placing a vulnerable prisoner in a cell with a suicidal inmate can give rise to a duty to prevent reasonably foreseeable psychiatric harm (Butchart v Home Office [2006] EWCA Civ 239).

Worked Example 1.8

Two off-duty volunteers arrive after a crowd crush and help with triage. They are never in danger themselves but later develop psychiatric illness due to what they saw.

Answer:

As rescuers not in danger, they are neither primary nor secondary victims unless they meet Alcock proximity requirements. Mere rescue involvement without danger does not confer primary victim status (White). Recovery is unlikely unless the strict secondary victim criteria (including proximity of relationship to an injured person) are met.Revision Tip: Remember the strict Alcock control mechanisms for secondary victims. In scenarios, check each element carefully: relationship proximity, time/space proximity, and perception proximity. Failure on any one point means the claim fails.

Key Point Checklist

This article has covered the following key knowledge points:

- Tort law distinguishes between different types of loss: physical damage, economic loss, and psychiatric harm.

- Physical damage includes personal injury and property damage, along with consequential financial losses.

- The eggshell skull rule applies to personal injury: the defendant is liable for the full extent of injury even if the severity was not foreseeable.

- Economic loss is financial loss. Consequential economic loss (flowing from physical damage to the claimant's person/property) is generally recoverable. Pure economic loss (not flowing from such damage) is generally irrecoverable, barring exceptions like negligent misstatement.

- Negligent misstatement liability requires assumption of responsibility and reasonable reliance. Disclaimers may negate responsibility if effective.

- Psychiatric harm must be a medically recognised illness caused by sudden shock.

- Primary victims (in the zone of physical danger) can recover if physical injury was foreseeable.

- Secondary victims (witnesses not in danger) must satisfy the strict Alcock criteria relating to foreseeability of psychiatric harm and proximity (relationship, time/space, perception).

- Rescuers are only primary victims if exposed to danger; otherwise they must satisfy the Alcock controls to recover.

- Anxiety about future disease without psychiatric illness is not actionable; limited recognition exists for psychiatric harm caused by witnessing destruction of one’s own property.

Key Terms and Concepts

- Consequential Economic Loss

- Pure Economic Loss

- Psychiatric Harm

- Primary Victim

- Secondary Victim

- Eggshell Skull Rule

- Negligent Misstatement

- Assumption of Responsibility

- Sudden Shock