Learning Outcomes

This article outlines the legal requirements for forming general partnerships, limited partnerships, and limited liability partnerships (LLPs) in England and Wales, including:

- The principal statutory frameworks and default rules (Partnership Act 1890, Limited Partnerships Act 1907, Limited Liability Partnerships Act 2000, LLP Regulations 2001, and relevant Companies Act 2006 provisions applied to LLPs)

- Formation requirements for general partnerships and the step-by-step registration procedures for limited partnerships and LLPs at Companies House

- How liability of partners and members operates in each structure, including unlimited liability, limited liability, and the consequences of defective registration

- Key structural and practical differences between general partnerships, limited partnerships, and LLPs, enabling accurate selection of business medium in SQE1 problem questions

- Authority and agency in partnerships and LLPs, including “holding out”, apparent authority, and how these concepts affect third-party rights

- Filing and ongoing compliance obligations for LLPs and limited partnerships, and the role, powers, and responsibilities of designated members

- How outgoing and incoming partners’ or members’ positions are managed, including notice, novation, and allocation of existing debts

- Application of these principles to SQE1-style multiple-choice and scenario-based questions, with emphasis on spotting common traps and examiner favourites

SQE1 Syllabus

For SQE1, you are required to understand the legal requirements and practical implications of forming partnerships and LLPs, with a focus on the following syllabus points:

- The statutory definitions and formation requirements for general partnerships, limited partnerships, and LLPs

- The liability of partners and members in each structure

- The process and formalities for registration of limited partnerships and LLPs

- The distinction between incorporated and unincorporated business forms

- The default rules governing partnerships and LLPs in the absence of an agreement

- Authority and agency in partnerships and LLPs, including “holding out” and apparent authority

- Outgoing and incoming partners’ liabilities and notices under the Partnership Act 1890

- LLP designated members, filing obligations (accounts, confirmation statements, PSC), and the application of Companies Act provisions to LLPs

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the statutory definition of a general partnership under English law?

- Which business structures must be registered at Companies House?

- What is the liability position of a member in an LLP compared to a partner in a general partnership?

- What are the consequences if a limited partner in a limited partnership participates in management?

- True or false: A written partnership agreement is required to form a general partnership.

Introduction

When advising clients on setting up a business, it is essential to understand the legal requirements for forming partnerships and limited liability partnerships (LLPs). The main statutory frameworks are the Partnership Act 1890 for general partnerships, the Limited Partnerships Act 1907 for limited partnerships, and the Limited Liability Partnerships Act 2000 for LLPs. Each structure has different rules on formation, registration, and liability. This article explains the key legal requirements for each, focusing on what you need to know for the SQE1 exam. Be aware that certain Companies Act 2006 provisions apply to LLPs by virtue of the Limited Liability Partnerships (Application of Companies Act 2006) Regulations 2009 and that the Limited Liability Partnerships Regulations 2001 supply default terms where members have not agreed their own LLP agreement. Also note that a company can be a partner in a partnership or a member of an LLP.

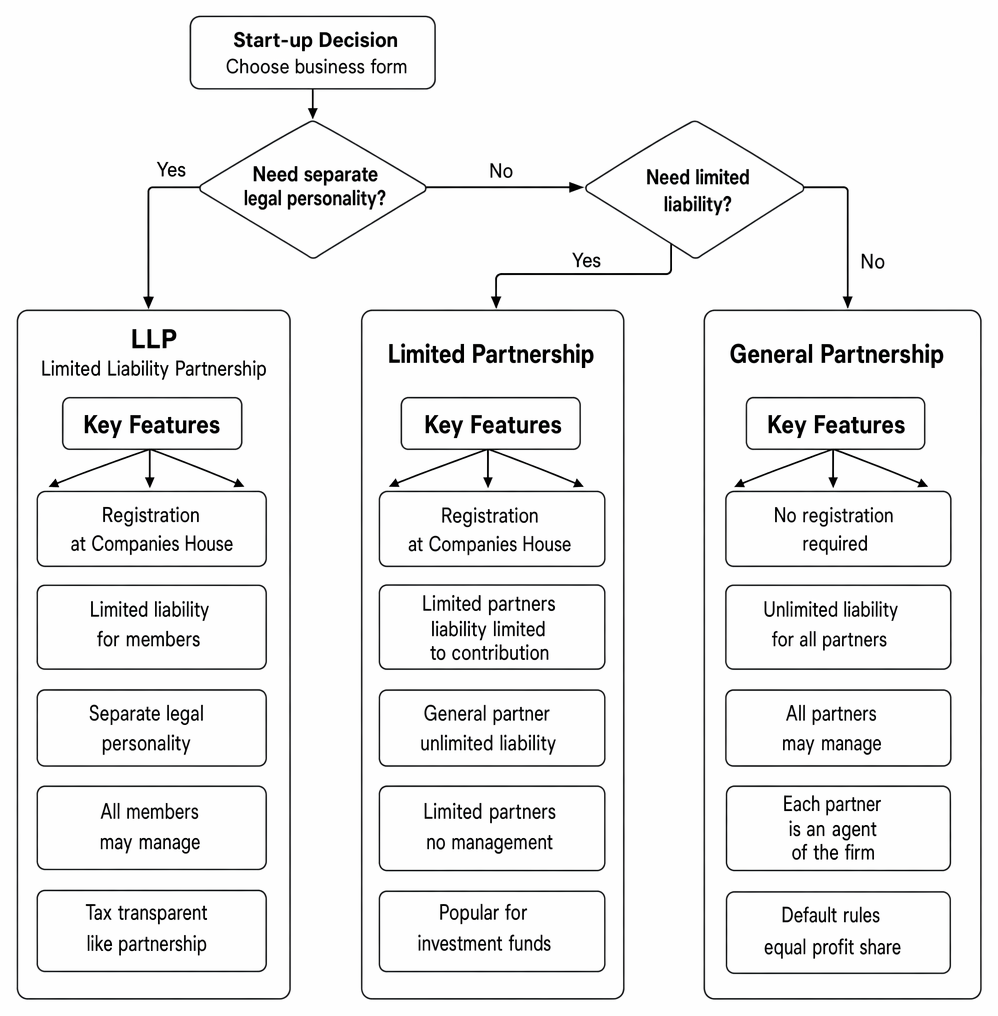

Decision tree summarising principal formation considerations and key legal characteristics of general partnerships, limited partnerships and LLPs.

Key Term: general partnership

A business relationship where two or more persons carry on a business in common with a view to profit, as defined in s.1 Partnership Act 1890.Test Tip: In SQE-style questions on Legal requirements, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Exam Warning: Do not rely on a familiar phrase from Legal requirements alone; check whether the facts satisfy every condition, exception, and timing requirement.

General Partnerships

A general partnership is an unincorporated business formed when two or more persons carry on a business in common with a view to profit. “Persons” includes individuals and companies. The partnership has no separate legal personality in England and Wales, so rights and liabilities ultimately lie with the partners. A partnership may use a “firm name” and can sue or be sued in that name procedurally, but this does not confer separate legal personality.

Formation

No formal registration or written agreement is required to form a general partnership. A partnership can arise by express agreement or by conduct. The existence of a partnership is a question of fact, based on whether the parties are genuinely carrying on a business together for profit.

Two elements commonly tested are “business in common” and “view to profit”. Informal collaborations may fall short if, for example, parties are merely co-owners of property or share gross returns without jointly carrying on a business. Receipt of a share of profits is prima facie evidence of partnership but is not conclusive where the payment is, for instance, wages, interest on a loan, or rent. In practice, exam scenarios often pivot on whether there is genuine joint activity and shared profits rather than mere revenue splitting.

Because formation is factual, a partnership can arise before formal launch or first trading day if the parties have already started working together on partnership business. Preparatory activity and planning may therefore be enough to bring the statutory definition into play where the other elements are present.

Where parties intend a partnership, a written agreement is strongly recommended to avoid leaving key terms to statutory defaults and to clarify capital contributions, profit shares, decision-making, and exit arrangements.

Key Term: partnership agreement

A document (written or oral) setting out the terms on which partners agree to run their business. Not legally required, but highly recommended.

If trading under a business name that is not simply the partners’ names, trading disclosure rules require certain information to be displayed on stationery and at business premises so third parties can identify who they are dealing with.

Default Rules

If there is no partnership agreement, the Partnership Act 1890 provides default rules, including:

- Profits and losses are shared equally

- All partners may participate in management

- No partner is entitled to a salary

- Ordinary business decisions are made by majority; changes to the nature of the business require unanimity

Further defaults worth knowing for SQE1 include:

- No new partner can be introduced without the consent of all existing partners

- Partners are entitled to access the partnership books and to render true accounts and full information to each other

- The firm must indemnify partners for liabilities incurred in the ordinary and proper conduct of business

- Partners who advance sums beyond their agreed capital are entitled to interest on those advances

- Expulsion of a partner requires a contractual power; there is no default power of expulsion

These defaults operate unless varied by agreement. Many partnerships vary profit shares, voting thresholds, and introduce powers such as expulsion or restrictive covenants in a tailored partnership agreement.

Liability

Partners in a general partnership have unlimited personal liability for the debts and obligations of the firm. Each partner is jointly liable for debts incurred while a partner and severally liable for wrongful acts.

Contractual liabilities of the firm are joint among partners; tort liabilities and breaches of trust by a partner in the course of business are joint and several. An incoming partner is not, by default, liable for debts incurred before admission unless there is a novation or agreement with creditors. A retiring partner remains liable for debts incurred while they were a partner; to avoid liability for future debts they must ensure proper notice is given to those with whom the firm has dealt.

Key Term: unlimited liability

The personal responsibility of partners for all debts and obligations of the partnership, exposing their personal assets.

Partners may also incur liability for “holding out” where a person is represented as a partner and third parties rely on that representation. Limiting personal exposure through insurance (e.g. professional indemnity) and clear notices on retirement is therefore critical.

Agency

Each partner is an agent of the firm and of the other partners for the purpose of the business. Any partner can bind the firm and the other partners when acting within the usual scope of the partnership business.

Agency authority can be actual (express or implied by the agreement) or apparent (where the firm’s conduct leads a third party reasonably to believe the partner has authority). Internal restrictions on a partner’s authority will not protect the firm against third parties who reasonably rely on apparent authority unless the third party knows of the restriction or the act is outside the usual scope of the business.

Key Term: agency

The legal relationship where one person (the agent) is authorised to act on behalf of another (the principal). Key Term: apparent authority

Authority a third party reasonably believes an agent has due to the principal’s representations or conduct, even if actual authority is lacking.

A departing partner should give actual notice to existing clients and suppliers to avoid continued apparent authority. For persons who have not previously dealt with the firm, an advertisement or general notice may be sufficient; however, the safest approach is direct notification to those with whom the firm has dealt.

Fiduciary Duties

Partners owe fiduciary duties to each other and to the firm. These include duties of good faith, to account for profits, and to avoid conflicts of interest.

Core obligations include:

- Duty to render true accounts and full information of all things affecting the partnership

- Duty not to make secret profits from partnership transactions

- Duty not to carry on a competing business; if a partner does so without consent, they must account to the firm for profits arising

- Duty to use partnership property for partnership purposes and account for any personal benefit obtained from its use

Breach commonly leads to equitable remedies such as an account of profits in addition to contractual remedies under the partnership agreement.

Outgoing and incoming partners

On retirement, a partner remains liable for obligations incurred prior to retirement unless released by creditors via a novation. To avoid liability for new obligations, actual notice must be given to persons who have previously dealt with the firm; for others, public notice may suffice. Internally agreed indemnities protect the retired partner only as between partners and do not bind third-party creditors.

Incoming partners do not assume liability for existing debts unless they agree with creditors to do so. Internally, the partnership agreement will often provide for how existing liabilities are borne and how capital is adjusted on changes in membership.

Worked Example 1.1

Scenario: Alice and Ben agree to run a bakery together. They do not sign any written agreement. After six months, the bakery owes suppliers £10,000. Ben has no personal assets, but Alice owns a house.

Question: Can the suppliers pursue Alice personally for the partnership debts? Answer:

Yes. In a general partnership, all partners have unlimited liability. Alice’s personal assets, including her house, are at risk for the debts of the partnership.

Limited Partnerships

A limited partnership is a special type of partnership created under the Limited Partnerships Act 1907. It must have at least one general partner (with unlimited liability) and one or more limited partners (with liability limited to their contribution).

Key Term: limited partnership

A partnership with at least one general partner (unlimited liability) and at least one limited partner (liability limited to their contribution), registered under the Limited Partnerships Act 1907. Key Term: limited partner

An investor-partner in a limited partnership whose liability is limited to the amount they contribute, provided they do not take part in management.

Formation and Registration

A limited partnership must be registered at Companies House by submitting Form LP5 and paying the fee. The registration must state the firm’s name, nature of business, principal place of business, names of all partners, and the amount contributed by each limited partner.

Registration is a condition of limited liability. If not registered, the partnership is treated as a general partnership and limited partners will have unlimited liability. Subsequent changes (e.g. change in general partners, limited partners, capital contributions, or the nature of business) must be notified to Companies House on the appropriate forms within the prescribed timescale. The limited partnership is not a separate legal entity in England and Wales.

General partners manage the business and are agents of the firm. A general partner can be a company, which is common in private equity or real estate structures to shield individuals from unlimited liability while ensuring managerial control.

Limited partnerships may use a firm name. If trading under a business name that does not disclose the partners’ identities, trading disclosure rules apply so third parties can identify the persons behind the firm.

Restrictions on Limited Partners

Limited partners must not participate in management. If a limited partner takes part in management, they lose their limited liability for the period of their involvement.

Other key limitations include:

- Limited partners do not have authority to bind the firm

- They cannot withdraw their contribution or receive back any part of it while debts or liabilities remain; if capital is returned, they may become liable to creditors up to the amount returned

- They typically have rights to receive a share of profits and to access certain information, but no default right to participate in day-to-day decisions

These restrictions protect third parties who contract with the firm in reliance on the separation between managing general partners and passive limited partners.

Worked Example 1.2

Scenario: Carla invests £50,000 as a limited partner in a property development limited partnership. She attends a meeting and signs a contract with a supplier on behalf of the partnership.

Question: What is the effect of Carla’s participation in management? Answer:

By participating in management, Carla loses her limited liability and is treated as a general partner for the period she was involved in management. She may be personally liable for partnership debts incurred during that time.

Limited Liability Partnerships (LLPs)

An LLP is a separate legal entity formed under the Limited Liability Partnerships Act 2000. It combines features of a company and a partnership.

Key Term: limited liability partnership (LLP)

An incorporated business structure with separate legal personality, where members have limited liability and the LLP can own property, enter contracts, and sue or be sued in its own name.

Formation and Registration of LLPs

To form an LLP, at least two persons (individuals or companies) must subscribe to an incorporation document. The incorporation document and Form LL IN01, together with the fee, must be submitted to Companies House. The LLP must have a registered office and a name ending with “Limited Liability Partnership” or “LLP”.

The incorporation document identifies the initial members and includes details equivalent to those required for companies on form IN01 (registered office, name, and certain particulars). Companies House issues a certificate of incorporation on registration. There is no requirement to file an LLP agreement.

LLPs must comply with filing obligations broadly similar to companies (e.g. annual accounts and confirmation statements, and PSC register requirements). The names regime and trading disclosures mirror the company regime: the LLP’s name must appear on business documents together with place of registration and number.

Where the members are individuals, they ordinarily register with HMRC as self-employed because the LLP is generally taxed transparently rather than as a separate taxable company.

Key Term: designated member

An LLP member with additional responsibilities for statutory filings and compliance (e.g. accounts, confirmation statements, notices to Companies House, and certain insolvency-related functions).

LLPs must have at least two designated members. If the LLP has only two members, both must be designated members. Designated members are responsible for filing accounts, appointing/removing auditors, submitting confirmation statements, notifying changes in membership, and ensuring compliance with applicable Companies Act provisions.

If membership falls to one person for more than six months, that person becomes jointly and severally liable for LLP debts incurred from the end of that six-month period. This rule incentivises prompt restoration of multiple membership.

Legal Status

An LLP is a body corporate with separate legal personality. It can own property, enter contracts, and sue or be sued in its own name. Members are agents of the LLP, not of each other.

Separate personality and limited liability reflect the principle established in Salomon v A Salomon & Co Ltd: once incorporated, the entity is distinct from its members. In practice, this means LLP assets are owned by the LLP; members have no proprietary interest in those assets. It also means the LLP can contract with its members in different capacities (e.g. as service providers or employees), provided this is consistent with the LLP agreement and the law.

Liability (LLP)

Members of an LLP have limited liability. They are not personally liable for the LLP’s debts beyond their capital contribution, except in cases of fraud or wrongful trading.

Limited liability is subject to statutory exceptions where members’ conduct has contributed to insolvency. In an insolvent LLP, the insolvency regime applicable to companies generally applies. Members (especially designated members involved in management) may face liability for misfeasance, fraudulent trading, or wrongful trading and may be disqualified under the Company Directors Disqualification Act 1986. Members may also incur personal liability if they have given personal guarantees to lenders or landlords.

Key Term: limited liability

The principle that a member’s liability for the debts of the LLP is limited to their agreed contribution.

Members’ Agreement

Although not legally required, it is strongly advised that members enter into an LLP agreement to set out their rights and duties, profit sharing, and management arrangements. In the absence of an agreement, default rules in the Limited Liability Partnerships Regulations 2001 apply (e.g., equal sharing of profits).

Common provisions include capital contributions, drawings, profit shares, admission and retirement procedures, decision-making thresholds, management structures, restrictive covenants, and dispute resolution. Without such an agreement, default rules will govern critical points such as equality of profit shares, joint management, and the absence of remuneration for acting in management.

Key Term: LLP agreement

A private contract between the LLP and its members (or among members) setting rights, duties, and management arrangements; default provisions in the LLP Regulations 2001 apply if no agreement exists.

Management

All members may participate in management unless the LLP agreement provides otherwise. There is no distinction between general and limited members as in a limited partnership.

Members of an LLP are agents of the LLP, and standard agency principles apply. Actual authority may be limited by the LLP agreement and internal mandates; however, the LLP may still be bound by members’ acts where apparent authority exists and third parties reasonably rely on it. Sound internal governance and clear communication of authority limits are therefore essential to manage external risk.

LLPs can own property and grant security. Like companies, LLPs may issue debentures and grant fixed and floating charges. Unlike LLPs and companies, general partnerships cannot grant floating charges.

Corporate compliance and filings

Designated members must ensure the LLP meets ongoing filing requirements similar to companies, including:

- Filing annual accounts within statutory time limits (timings are aligned with company filing deadlines for private entities)

- Filing annual confirmation statements to keep Companies House records up to date

- Maintaining statutory registers (including PSC where applicable) and notifying changes in membership and charges

Failure to comply is a criminal offence for the LLP and the designated members. Transparency obligations balance the advantages of limited liability for third parties dealing with the LLP.

Worked Example 1.3

Scenario: Dinesh and Emma form an LLP to provide consultancy services. After a year, the LLP is unable to pay its debts. Dinesh has invested £5,000; Emma has invested £10,000. There is no evidence of fraud or wrongful trading.

Question: Are Dinesh and Emma personally liable for the LLP’s debts? Answer:

No. Members of an LLP have limited liability. They are not personally liable for the LLP’s debts beyond their agreed contributions, unless they have engaged in fraud or wrongful trading.

Comparison Table: Partnerships, Limited Partnerships, and LLPs

| Feature | General Partnership | Limited Partnership | LLP |

|---|---|---|---|

| Legal personality | No | No | Yes |

| Registration required | No | Yes (Companies House) | Yes (Companies House) |

| Liability | Unlimited (all) | Unlimited (general); limited (limited partners) | Limited (all members) |

| Management | All partners | General partners only | All members |

| Separate assets | No | No | Yes |

Key Point Checklist

This article has covered the following key knowledge points:

- The statutory definition and formation requirements for general partnerships, limited partnerships, and LLPs

- Unlimited liability of partners in general partnerships; limited liability for limited partners and LLP members

- Registration is required for limited partnerships and LLPs at Companies House

- LLPs are incorporated bodies with separate legal personality; general and limited partnerships are not

- The importance of written agreements to avoid default statutory rules

- Authority and agency: partners are agents of the firm; LLP members are agents of the LLP; apparent authority can bind the firm/LLP despite internal restrictions

- Outgoing partners must give actual notice to persons who have previously dealt with the firm to avoid ongoing liability; novation is needed to release liability for existing debts

- Limited partners must not take part in management; otherwise they lose limited liability for the period of involvement and may be liable up to their full personal assets

- LLPs must have designated members and comply with filing obligations (accounts, confirmation statements, PSC where applicable); Companies Act 2006 provisions apply to LLPs via regulations

- LLPs and companies can grant floating charges; general partnerships cannot

Key Terms and Concepts

- general partnership

- partnership agreement

- unlimited liability

- agency

- apparent authority

- holding out

- limited partnership

- limited partner

- limited liability partnership (LLP)

- LLP agreement

- limited liability

- designated member

Additional detail for application

When faced with a problem question:

- Determine the business medium by the presence or absence of registration and separate personality. If the entity is registered as an LLP and has “LLP” in the name, treat it as a corporate body. If a partnership is unregistered and formed by conduct or agreement, apply the Partnership Act 1890.

- Identify agency issues. Has a partner or LLP member acted within the usual scope of the business? If apparent authority exists, the firm/LLP may be bound even if actual authority was lacking.

- Map liability. In a general partnership, partners are jointly liable for contractual debts and jointly and severally liable for torts; in an LLP, members’ liability is limited unless exceptions (e.g. wrongful trading) apply; in a limited partnership, ensure the limited partner did not manage and did not receive a return of capital while creditors remained unpaid.

- Check formalities. For limited partnerships and LLPs, consider whether statutory registration was properly completed and whether required filings were made on subsequent changes. For LLPs, consider designated members’ roles and the effects of non-compliance.

- Apply default rules only if there is no written agreement. If a partnership or LLP agreement exists, read any facts that indicate bespoke terms for profit-sharing, management, admission/retirement, or expulsion.

Key Term: holding out

Liability as a partner may arise where a person is represented as a partner and a third party relies on that representation when dealing with the firm.