Learning Outcomes

This article explains accounting procedures and entries for maintaining accurate client ledgers and records under the SRA Accounts Rules, including:

- Applying double-entry bookkeeping correctly to all solicitor accounts events, mapping debits and credits to cash accounts and dual‑column client ledgers.

- Distinguishing client and business money in law firm scenarios and recording each stream accurately in ledgers, cash books, and bank accounts.

- Handling receipts and payments, including mixed receipts, with prompt allocation and compliant postings between client and business accounts.

- Executing client‑to‑business transfers after billing in line with Rule 4.3, and processing inter‑client and inter‑matter transfers without cash movement.

- Authorising withdrawals from client account only for permitted purposes, checking sufficiency of client‑specific funds, and correcting any deficits immediately.

- Designing and interpreting reconciliations and central records under Rule 8, so that client account, cash book, and ledger balances always agree.

- Calculating and posting interest on client money, including sums in lieu from pooled accounts and interest on separate designated deposit client accounts.

- Identifying and avoiding misuse of client account as a banking facility, and applying modified controls for joint accounts, clients’ own accounts, and TPMAs.

- Managing file closure and residual balances properly, documenting attempts to trace clients and using charitable payments only where conditions are satisfied.

SQE1 Syllabus

For SQE1, you are required to understand and apply accounting procedures and entries for maintaining accurate client ledgers and records under the SRA Accounts Rules, with a focus on the following syllabus points:

- Requirements for accurate, contemporaneous, and chronological accounting records under Rule 8, including detailed client and matter identification per SRA guidance, and the necessity of dual column ledgers for complex transactions.

- Utilisation and continuing management of client ledgers and cash accounts, with separation and correct posting in business and client columns, ensuring clarity of record for every transaction within both practice and client contexts.

- Operation of double-entry bookkeeping for all monetary events, with full comprehension of receipt and payment flows for both client and business money, and proper allocation of debits and credits in all affected ledgers (including for VAT and disbursements).

- Mandatory recordkeeping and reconciliation controls: including running balances per ledger and cash sheet, matter-level identification, maintained central bills register, five-week reconciliation cycles, system for detecting and handling breaches, and adapted rules for accounts operated jointly with clients or on their behalf.

- Treatment of mixed receipts under Rule 4.2: core options for banking, accounting for allocation, rationale and documentation for firm procedures, and comprehensive double-entry recording for all transfers.

- Law and practice of post-billing transfers (Rule 4.3): ensuring bills or written notification are delivered and funds are sufficient, with entries in both ledgers and bank accounts as required by SRA guidance.

- Inter-client and inter-matter transfer entries: methodical use of DR and CR within client ledger columns, strict compliance with the no-cash-movement rule, and retention of written authority and audit records.

- Approval and supervision of withdrawals: requirement for appropriate authorisation by designated staff (including COFA), procedures to ensure client-specific sufficiency of funds (Rule 5.3), and obligations when deficits or breaches are identified.

- Calculation and recording of interest on client money: drafting and maintaining a written interest policy, correct posting for general interest and SDDCA receipts, and specific double entries for “sum in lieu” payments made from the business account.

- Enforcement of Rule 3.3: recognition and avoidance of all forms of banking facility misuse, understanding SRA disciplinary standards and risks.

- Obligations for prompt return of client money (Rule 2.5), effective management of unreturnable residual balances (including charitable disbursement protocol), and all documentation and record retention requirements attached thereto.

- Day-to-day recordkeeping, reconciliation, and compliance duties for joint accounts, clients’ own accounts, and third-party managed accounts—identifying which full rules apply, and which do not, for each special case.

- Protocols for immediate and documented correction of any rule breaches—focus on timely replacement of misapplied funds, documentation of correction, and regular COFA review.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following statements about double-entry bookkeeping is correct?

- a) Every transaction requires a single entry in the relevant ledger.

- b) Every transaction requires two debit entries in different ledgers.

- c) Every transaction requires one debit entry and one corresponding credit entry in different ledgers.

- d) Every transaction requires two credit entries in different ledgers.

-

A firm receives £5,000 from a client generally on account of costs. What are the correct initial double entries?

- a) DR Client Ledger (Client), CR Cash Account (Client)

- b) DR Cash Account (Client), CR Client Ledger (Client)

- c) DR Client Ledger (Business), CR Cash Account (Business)

- d) DR Cash Account (Business), CR Client Ledger (Business)

-

According to the SRA Accounts Rules, how should client ledgers be identified?

- a) By a unique reference number only.

- b) By the client’s name only.

- c) By the client’s name and a description of the matter.

- d) By the matter description only.

Introduction

Correct handling and recording of client money is an essential professional responsibility for solicitors, as prescribed by the Solicitors Regulation Authority (SRA) Accounts Rules. Failure to keep accurate, contemporaneous, and segregated records of client and business money transactions can result in significant legal, regulatory, and ethical risks, including disciplinary action, personal liability under trust law, criminal sanctions if dishonesty or misappropriation occurs, and reputational damage not only to the practitioner or firm but to the legal profession as a whole. Above all, strict application of the Accounts Rules serves to protect client assets by ensuring absolute separation from business funds and preserving the financial security and traceability of money that solicitors hold in trust.

Robust compliance requires technical accounting discipline and vigilant application of regulatory rules. Every receipt, payment, or transfer affecting client or business funds must be accurately classified, correctly recorded, and entered without undue delay, establishing running balances for each client and matter at any given time. This continuous process supports critical internal safeguards such as five-weekly reconciliations (Rule 8.3), supports the oversight of the firm’s Compliance Officer for Finance and Administration (COFA), and guarantees swift action should discrepancies or breaches occur during regular audits by accountants or SRA investigation.

Key Term: SRA Accounts Rules

A set of regulatory standards issued by the Solicitors Regulation Authority that governs the handling, recording, and safeguarding of client money by solicitors and their firms. The Accounts Rules detail the separation, prompt banking, and documentation requirements for client and business funds, as well as specific procedures for dealing with breaches or exceptional situations. Key Term: double-entry bookkeeping

A system requiring every financial transaction to result in two separate entries: a debit (DR) in one account and a corresponding credit (CR) in another. This principle guarantees that the accounting equation (Assets = Liabilities + Equity) always balances, providing a self-checking mechanism that ensures the integrity and accuracy of recorded finances.

Double-Entry Bookkeeping Principles

Double-entry bookkeeping underpins the entire accounting structure of law firms and is mandated for all transactions involving client and business money under SRA requirements. The core axiom is that every financial event must be recorded with at least two equal and opposite entries—a debit and a credit—across different accounts or ledger columns. This principle underlies both the control framework for internal management and the external auditability of every transaction affecting client or business accounts.

- A debit (DR) records an increase in an asset (e.g., bank account), a reduction in a liability (e.g., amount owed to a client), or an increase in an expense.

- A credit (CR) records an increase in a liability (e.g., the firm’s obligation to a client), an increase in equity, or a reduction in an asset.

Each transaction’s dual effect is posted so that, in aggregate, the books always balance; every movement into one account must be matched by a corresponding movement out of another.

Key Term: debit (DR)

In legal practice accounts, a debit entry increases client or business assets (such as funds in a bank account) or recognises expenses incurred. DR entries are always to the left of an account or ledger column. Key Term: credit (CR)

In the legal context, a credit entry denotes an increase in the firm’s obligation to a client within the client ledger, or a reduction of the business/cash asset when shown in the cash account; always shown in the right-hand column.

Competent understanding of which side (DR or CR) is posted for any entry type is critical for compliance. This system is not just mechanical: it provides a transparent audit trail and supports the detection and prompt rectification of errors.

Key Term: journal entries

Summaries of double-entry postings for each transaction, explicitly stating which accounts or ledgers are affected, the amount involved, and delineating which entries are DR and which are CR. Journal entries provide a snapshot of the transaction flow for examination or audit.

A distinctive feature of law firm accounts is that most ledgers are constructed and viewed from the firm’s (the business’s) viewpoint, so the impact of each entry is always considered in terms of the firm’s liabilities and entitlements, not the client’s personal finances. This viewpoint is particularly important when interpreting the columns on the client ledger: credits in the client column mean the firm owes that amount to the client; debits reduce that obligation as funds are paid out appropriately.

Mapping debits and credits to the dual-column structure

- Cash account (client column): DR for receipts into client bank; CR for withdrawals from client bank.

- Cash account (business column): DR for receipts into business bank; CR for payments out of business bank.

- Client ledger (client column): CR when client money is received/held; DR when money is paid out on the client’s behalf or returned.

- Client ledger (business column): DR when the client is billed for profit costs and VAT (the client owes the firm); CR when the bill is settled (by payment into business bank or by transfer from client bank after the bill).

Worked Example 1.1

A firm receives £500 from Client A generally on account of costs. The firm also receives £200 from Client B in payment of a bill already issued. How are these receipts recorded?

Answer:

Client A (£500): DR £500 Cash Account (Client); CR £500 Client Ledger A (Client). Client B (£200): DR £200 Cash Account (Business); CR £200 Client Ledger B (Business).

Accounting Records in Law Firms

Law firms are unique among businesses, as they routinely handle significant sums of money belonging to clients or third parties (such as estate beneficiaries, lenders, or counterparties), rather than only dealing with their own business money. This reality places an absolute regulatory burden on legal practices to separate and meticulously record each movement of client money, maintaining an uninterrupted audit trail for every client and transaction.

Key Term: business money

Money belonging exclusively to the firm, including fees paid after billing and reimbursements for disbursements paid post-bill issuance. Key Term: client money

Funds received or held in connection with regulated legal services (including as trustee, agent, stakeholder, or donee of a power of attorney) that do not belong to the firm. Client money includes: (1) money for a client; (2) money for a third party relating to regulated services; (3) money held in a special capacity; (4) money for fees/disbursements prior to billing.

Rule 4.1 requires this client money to be kept entirely separate from business money at all times, typically via different bank accounts and dual column ledgers.

Key Term: client account

A bank or building society account in England and Wales, titled with the firm’s name and the word “client”, established specifically for the safeguarding and segregation of client money. This account must not be used to provide or approximate a banking service for clients or third parties; all funds must be linked to regulated legal work.

Ledgers and Cash Accounts

The architectural feature of legal accounts is the dual system of ledgers and cash accounts, constructed to clarify the flow and current standing of both client and business money. Each serves distinct but interrelated purposes.

Key Term: ledger

A structured record—manual or digital—in which a law firm enters monetary transactions as debits or credits, tracking the flow and balance of client and business money for each matter.

Law firms employ several ledgers. Transaction solely related to the business (such as payment of wages, rent, or firm income) are recorded in business-only ledgers (e.g., profit costs ledger, office expense ledger). These ledgers have no “client” column because they never record transactions involving client money.

However, client-related activities demand dual column ledgers—each with a “business” column and a “client” column—to allow for meticulous tracking of funds that may span both spheres.

Key Term: cash account

Also known as the cash book or cash sheet, this record traces all monetary inflows and outflows from the business and client bank accounts. In law firms, the cash account is structured with parallel columns—one tracking the firm's own bank (“business” account), the other for client bank account movements. Key Term: dual column ledger

A client ledger or cash account that presents both business and client columns side-by-side. Dual column ledgers enable law firms to display business money and client money separately within the same matter or cash record, maintaining clear segregation for regulatory compliance and audit purposes. Key Term: client ledger

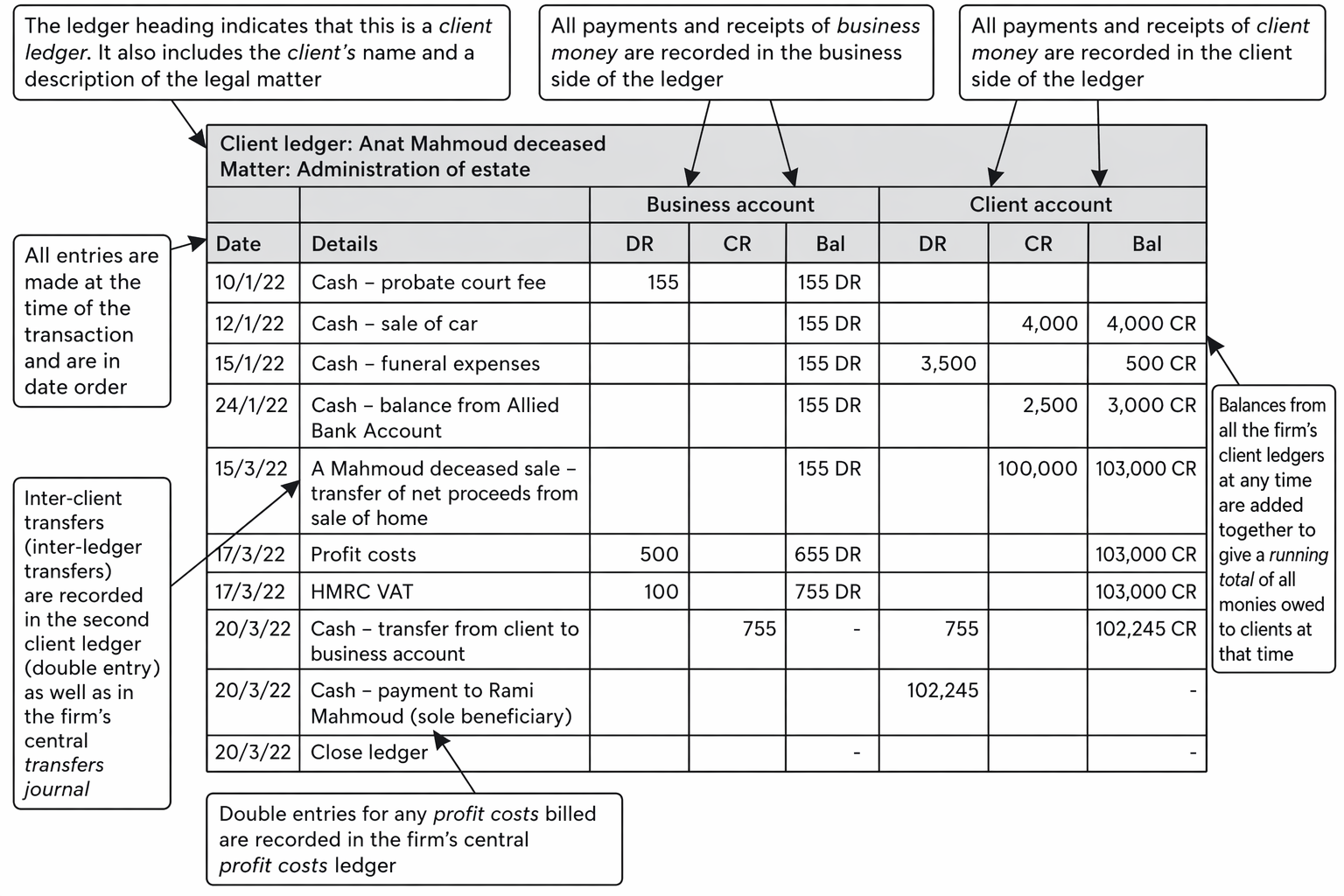

An individual client’s running account, recording (in dual columns) the movement and current balance of client money and, if appropriate, business money (such as profit costs owed or paid in a matter). Each client ledger must identify the client by name and the matter description.

Rule 8.1 mandates that every matter must have a clearly identifiable client ledger, stating the client’s name and a description of the matter sufficiently detailed to distinguish between multiple matters for the same client.

The accuracy, promptness, and completeness of postings are essential. Each entry must record the date, nature, and parties to each transaction, permitting running balances to be seen or easily calculated at any time. This supports both the practical needs of the solicitors and the regulatory and audit function of regulators.

Dual Column Ledgers and How They Are Used

In practice, all monetary transactions handled by law firms are recorded in dual column ledgers, ensuring that client and business transactions are separated and never commingled. The correct use of dual columns is not only a regulatory requirement, but also a practical necessity for reconciling accounts and protecting client assets.

Client and business money transactions are classified, banked, and posted by double entry, with client payments conditional on sufficient funds.

- In the client column, credit entries (CR) typically increase the amount the firm owes to the client (i.e., how much of the client’s money the firm holds), while debit entries (DR) indicate money paid out on the client’s behalf, reducing this balance.

- In the business column, debit entries (DR) usually recognise money the client owes to the firm—such as for fees or disbursements—while credits (CR) reduce these sums, such as when a bill is paid.

A correctly maintained client ledger will always display a credit balance in the client column for active client money; a debit balance (indicating funds paid out in excess of money held for that client) signals a breach requiring prompt correction.

Recording Receipts

The accurate and timely recording of money received is essential for fulfilling SRA requirements. The process for recording depends on whether the receipt is classified as client or business money, or a mixture.

- Receipts of client money (such as funds on account for costs/disbursements, sale proceeds, or balances received in trust) are entered as a DR (increase) in the cash account's client column. The matching entry is a CR in the client ledger's client column, showing the firm owes the money to the client or is holding it in trust.

- Receipts of business money (such as bill payments) are entered as a DR in the business column of the cash account, with a corresponding CR in the business column of the client ledger, reflecting the reduction of the client's debt to the firm.

Time is of the essence: client money must be paid into the client account promptly—practically the day of receipt or the next working day, save for reasonable exceptions (e.g., where an alternative written arrangement under Rule 2.3(c) applies).

Key Term: mixed receipt

A single payment that contains both client money (e.g., funds on account or transaction monies) and business money (e.g., settlement of a billed fee). Under Rule 4.2, the firm must allocate mixed receipts promptly to the correct bank account(s).

Worked Example 1.2

A firm needs to pay a court fee of £150 for Client C. The firm holds £500 for Client C in the client account. Separately, the firm pays its monthly electricity bill of £300. How are these payments recorded?

Answer:

Client C (£150): CR £150 Cash Account (Client); DR £150 Client Ledger C (Client). Electricity (£300): CR £300 Cash Account (Business); DR £300 Electricity Expense Ledger (Business).

Complex Transactions: Transfers and Mixed Receipts

Legal firms frequently manage transactions in which receipts comprise both client and business money, or in which money must be transferred between accounts following billing or inter-client instructions.

Mixed receipts (for example, a cheque or bank transfer that combines bill payment for profit costs and a further sum to hold on account) present particular challenges:

- If the bank will split the cheque (rare), each portion is posted to its respective account immediately.

- More commonly, the full amount is banked into the client account, and the business portion is transferred promptly to the business account, with supporting journal and ledger entries. Alternatively, some firms (by policy) initially bank mixed receipts to business account where business money predominates, then promptly transfer the client element to client account.

- The definition of "promptly" is not fixed but must be reasonable and consistent with SRA guidance and firm policy. Conservative practice is to process on the day or next working day; a two-week maximum was formerly specified and remains a safe internal policy parameter.

Key Term: inter-client transfer

An internal ledger-only transfer reallocating client funds from one client/matter to another at the client’s instruction. No cash account movement is made—just DR and CR postings in the affected client ledgers. Key Term: separate designated deposit client account (SDDCA)

A dedicated deposit account opened specifically for holding significant sums for an individual client or matter. Interest belongs to the client. Ledger recording may use separate deposit columns or dedicated deposit ledgers.

Worked Example 1.3

A client sends £1,000 by bank transfer: £600 is to settle a delivered bill (profit costs + VAT), and £400 is to be held on account of future costs. The firm’s policy is to pay mixed receipts into the client account first, then transfer promptly. What are the entries?

Answer:

Receipt into client bank: DR £1,000 Cash Account (Client); CR £1,000 Client Ledger (Client). Prompt transfer of £600 business element: CR £600 Cash Account (Client) and DR £600 Client Ledger (Client); DR £600 Cash Account (Business) and CR £600 Client Ledger (Business). £400 remains as client money.

Worked Example 1.4

Firm holds £800 client funds for Client D. A bill for £750 (profit costs + VAT) is delivered, and the sum is immediately transferred to the business account. What entries?

Answer:

Bill issue (no cash movement): DR £750 Client Ledger D (Business); CR £750 Profit Costs/HMRC VAT Ledgers (Business). Transfer of costs to business bank: CR £750 Cash Account (Client); DR £750 Client Ledger D (Client); DR £750 Cash Account (Business); CR £750 Client Ledger D (Business).

Worked Example 1.5

The firm acts for Client E in two matters: £1,500 client funds are held on “Matter 1” (sale). Client instructs a transfer of £300 to “Matter 2” (will). How are entries posted?

Answer:

DR £300 Client E Ledger (Matter 1 – Client column); CR £300 Client E Ledger (Matter 2 – Client column). No cash movement.

Worked Example 1.6

A £5,000 cheque on account of costs from Client F is paid into client account. Before clearance, £400 is paid out for a disbursement for Client F. The cheque bounces. What must the firm do?

Answer:

There is a deficit for Client F (breach of Rule 5.3). Replace immediately from business bank (Rule 6.1): DR £400 Cash Account (Client); CR £400 Cash Account (Business). Ledger narratives must document the breach and correction. When cleared funds are later received, reverse the temporary replacement. Key Term: client account reconciliation

A five‑weekly minimum process of matching client bank statements to the cash book and to the aggregate of all client ledger balances. Differences must be investigated and resolved immediately, with a signed reconciliation record (COFA or manager).

Mixed Receipts Expanded—policies and controls

Under Rule 4.2, any mixed receipt must be allocated promptly. Effective policies should:

- Declare where mixed receipts are initially banked (e.g., always into client bank).

- Set a short internal timescale for transfers (e.g., same day or next working day).

- Require contemporaneous cross-referencing narratives (bill number, matter ID).

- Mandate dual review or post-event sampling by accounts staff, escalated to COFA for outliers.

Accuracy and Compliance

Under Rule 8, law firms must keep ledgers and all supporting records accurate to the penny, contemporaneously and in chronological order, such that a running balance for each client and matter is always apparent or easily ascertainable. This is essential for meeting reconciliation requirements, managing risk, and demonstrating compliance to auditors and the SRA.

Reconciliation of client accounts (Rule 8.3) is mandated at least every five weeks, and must compare the balances on bank statements, cash sheets, and the sum total of individual client ledgers. Any discrepancies must be investigated and resolved immediately, with the reconciliation signed by a manager or COFA and retained.

Key Term: Compliance Officer for Finance and Administration (COFA)

The manager appointed to oversee compliance with the Accounts Rules: monitoring, reporting, rectifying breaches, maintaining central records, and enforcing authorisation controls over withdrawals.

Rule 8.4 requires a central electronic or written record of all bills and written notifications of costs as a cross-reference for audit and regulatory inspection. Records of rectified breaches, including associated documentation, must be retained for at least six years.

Key Term: central record of bills

The mandated register where all bills or written notifications of costs are recorded. It links accounting entries to the delivery of bills and is essential for audit and transfer of costs under Rule 4.3.

Recording Payments and Authorisation Controls

Before initiating any payment, the solicitor must verify the nature of the intended payment and confirm sufficient funds are held for the specific client (Rule 5.3). Withdrawals must be for a permitted purpose (Rule 5.1), and authorisation must follow documented procedures (Rule 5.2).

- Payments out of client account: CR cash account (client); DR client ledger (client).

- Payments out of business account: CR cash account (business); DR appropriate business ledger (e.g., expense ledger).

Worked Example 1.7

Client G has £2,300 in client account. The firm must pay counsel’s VAT-inclusive invoice of £1,200, addressed to the client (agency basis). What are the entries?

Answer:

Payment from client bank (agency method): CR £1,200 Cash Account (Client); DR £1,200 Client Ledger G (Client). No VAT posting to the firm’s VAT ledger because the invoice is not to the firm.Exam Warning:

- Never pay a third party from client bank if insufficient client funds exist for that specific client (Rule 5.3). Temporary use of other clients’ money is a serious breach.

- Do not pay from client account before funds have cleared when receipt is by cheque. If clearance is essential to meet a deadline, either wait or advance firm money (document as an advance to client that becomes client money upon transfer).

Bills, Abatement, Disbursements and VAT—core postings

When a firm issues a bill (profit costs + VAT), there is no cash movement. Post:

- DR client ledger (business column) for profit costs and VAT separately;

- CR profit costs ledger and CR HMRC-VAT ledger.

If the bill is reduced (abated), reverse the relevant elements:

- CR client ledger (business) for the abatement amounts;

- DR profit costs ledger and DR HMRC-VAT ledger accordingly.

For disbursements:

- Agency method (invoice to client): pay VAT-inclusive amount from client bank if funds available; record only on client lines (no firm VAT impact).

- Principal method (invoice to firm): pay from business bank; post VAT to HMRC-VAT ledger (input tax); recharge the client on the next bill (profit costs ledger not used for the disbursement recharge—use a separate “Disbursements Recharged” income line if maintained).

Worked Example 1.8

The firm acts on a commercial lease. Land Registry fee invoice £270 is in the firm’s name (principal method). The firm pays it now and will recharge on the next bill. What entries?

Answer:

Payment from business bank now: CR £270 Cash Account (Business); DR £225 Disbursements Paid (Business); DR £45 HMRC-VAT (input VAT). On recharging within the bill: DR Client Ledger (Business) £225 (disbursement net) and DR Client Ledger (Business) £45 (VAT) with matching credits to Disbursements Recharged (Business) £225 and HMRC-VAT (output VAT) £45.

Client-to-Business Transfers After Billing (Rule 4.3)

Where client money held is to be used to pay the firm’s costs, the firm must first give a bill (or other written notification of costs). The transfer must then:

- Match the specific sum in the bill/notification;

- Be covered by client funds held for that client/matter;

- Be promptly posted with cash and ledger entries in both columns.

Worked Example 1.9

Client H has £1,800 in client bank. A bill of £1,500 (profit costs + VAT) is issued, and the firm transfers the sum to the business bank. Post the entries.

Answer:

Bill issue: DR £1,500 Client Ledger H (Business); CR Profit Costs/HMRC-VAT Ledgers (Business). Cash transfer: CR £1,500 Cash Account (Client); DR £1,500 Client Ledger H (Client); DR £1,500 Cash Account (Business); CR £1,500 Client Ledger H (Business).

Interest and Designated Deposits

Law firms must pay a fair sum of interest on client money held (Rule 7). For pooled client accounts, the firm usually pays a sum in lieu of interest from business bank (as interest earned on the pool belongs to the firm), while for SDDCAs all actual bank interest belongs to the client.

Key Term: interest policy

A written policy setting out how the firm calculates and pays a fair sum of interest on client money, including thresholds and exclusions, and informing clients sufficiently for consent to any different arrangement.

Accounting entries for interest payable from pooled funds:

- Record the business expense: DR Interest Payable (Business ledger); CR Client Ledger (Business).

- Transfer the sum from business to client bank: DR Cash Account (Client); CR Cash Account (Business); DR Client Ledger (Business); CR Client Ledger (Client).

For SDDCAs, record transfers into and out using either separate deposit columns or deposit ledgers, and post the bank interest as a DR to deposit cash (client) and CR to deposit client ledger (client). On closure, transfer principal plus interest back to general client account.

Worked Example 1.10

The firm pays Client J £90 as a fair sum in lieu of interest from pooled client monies. Show the postings.

Answer:

Step 1 (expense): DR £90 Interest Payable (Business); CR £90 Client Ledger J (Business). Step 2 (cash transfer): CR £90 Cash Account (Business); DR £90 Client Ledger J (Business); DR £90 Cash Account (Client); CR £90 Client Ledger J (Client). Payment out of client account to Client J: CR £90 Cash Account (Client); DR £90 Client Ledger J (Client).

Returning and Allocating Client Money

Rule 2.5 requires promptly returning client money when there is no longer any proper reason to hold it. Avoid residual balances by actively closing files, reconciling ledger balances to completion statements/estate accounts, and promptly disbursing to clients/beneficiaries.

Residual balances may be paid to charity without SRA authorisation only if each balance is under £500 and reasonable attempts to trace the owner are documented; larger amounts require SRA permission. Keep a central register of such payments and retain evidence and indemnities from the charity for at least six years.

Worked Example 1.11

A conveyancing file shows a residual client balance of £32 discovered during a routine reconciliation. The client cannot be traced after reasonable efforts. What may the firm do?

Answer:

Pay the residual £32 to a suitable charity under the prescribed circumstances. Record the tracing steps, charity receipt, and entry on the central register; retain records for at least six years.

Authorisation and Sufficiency of Funds for Withdrawals

Withdrawals from client account are permitted only where:

- The firm holds sufficient funds for the specific client/matter (Rule 5.3).

- The withdrawal is for a permitted purpose (Rule 5.1).

- The payment has been appropriately authorised and supervised (Rule 5.2).

A negative client ledger balance is a breach. Replace immediately from business funds and document the breach, cause, and correction.

Worked Example 1.12

Client K’s client ledger shows £850. The solicitor pays £900 to HMCTS for an issue fee in error. What steps follow?

Answer:

Immediate replacement of the £50 shortfall from business bank to client bank; record the breach and its rectification. Correct the ledger and notify the COFA. Consider process improvements to prevent recurrence.

Misuse of Client Account and Use Restriction (Rule 3.3)

Rule 3.3 strictly prohibits use of the client account to provide banking facilities. Funds must be received, held and moved only in connection with the delivery of regulated legal services, and with a proper nexus to the legal work.

Key Term: client account (use restriction)

The client account must never be used to process payments unconnected with regulated services. Convenience, speed or the client’s banking difficulties do not justify use of client account as a banking facility.

Worked Example 1.13

A client asks the firm to retain sale proceeds in client account and to pay monthly credit card bills on their behalf. What should the firm do?

Answer:

Refuse. There is no sufficient legal nexus to regulated work. Return net proceeds to the client promptly and do not operate as a banking facility.

Controls for Other Account Types and Modified Rules

Some situations require adapted rules and records.

Key Term: joint account

An account operated by the firm jointly with a client or third party (e.g., co‑executor). Obtain at least five‑weekly statements and keep a central record of bills relating to the account. Key Term: client’s own account

A bank account belonging to the client which the solicitor operates as signatory (e.g., attorney or deputy). Obtain statements and reconcile at least every five weeks; keep a central bills record. Key Term: third‑party managed account (TPMA)

An FCA-regulated payment service provider’s account used by a firm to handle client monies without the firm itself holding client money. Firms must notify the SRA, check regulation/terms, explain the arrangement to clients, and obtain/monitor statements.

When operating joint accounts or clients’ own accounts, day-to-day application of Rules 8.2–8.4 (statements, reconciliation, central bills record) applies as indicated above. For TPMAs, client money is not “held” by the firm under the Rules, but firms retain duties to safeguard clients’ interests, keep adequate internal records, and monitor TPMA statements.

Worked Example 1.14

You are a Court of Protection deputy managing a separate deputyship account for P. What reconciliations are required?

Answer:

Obtain statements at least every five weeks and prepare a five-week reconciliation. Keep a central record of bills served/notified for deputyship work, and retain records for six years.

Deposits Held as Stakeholder or Agent

Deposits on exchange in property transactions must be recorded accurately according to capacity.

Key Term: stakeholder deposit

A buyer’s deposit held on trust for both buyer and seller between exchange and completion. It does not belong to the seller until completion. Key Term: agent-held deposit

A buyer’s deposit held by the seller’s solicitor as agent for the seller. The money belongs to the seller from exchange, subject to the contract.

Stakeholder method options:

- Separate stakeholder ledger (joint names): receipt—CR stakeholder ledger (client column); DR cash account (client). On completion—DR stakeholder ledger (client); CR seller’s client ledger (client).

- Seller’s client ledger with clear stakeholder annotation: receipt—CR seller’s client ledger (client); DR cash account (client). Mark the stakeholder nature in the details to prevent misuse before completion.

Agent method:

- Receipt belongs to the seller from exchange, so record directly into seller’s client ledger: CR seller’s client ledger (client); DR cash account (client).

Worked Example 1.15

On exchange, the buyer pays a £20,000 deposit to be held as stakeholder. The firm uses a separate stakeholder ledger. What are the entries at exchange and completion?

Answer:

Exchange: CR £20,000 Stakeholder Ledger (Client); DR £20,000 Cash Account (Client). Completion: DR £20,000 Stakeholder Ledger (Client); CR £20,000 Seller’s Client Ledger (Client).

Disbursements: Agency and Principal Methods—common pitfalls

- If the invoice is addressed to the client: use agency method, make VAT-inclusive payment from client bank (if funds are held), and record only in client columns. Do not claim input VAT or charge output VAT on re‑billing.

- If the invoice is addressed to the firm: use principal method, pay from business bank, record input VAT, and recharge with output VAT on the bill.

Worked Example 1.16

Counsel’s fee £1,800 + VAT is addressed to the client. Sufficient client money is held. What is the proper treatment?

Answer:

Agency method: CR £2,160 Cash Account (Client); DR £2,160 Client Ledger (Client). No VAT postings to HMRC ledger.

Legal Aid Agency (LAA)—exception under Rule 2.3

Payments from the LAA for the firm’s costs may be paid directly into business account without first being paid into client account. Where a firm’s only client money is LAA payments for its costs (and it holds no other client money), Rule 2.2 permits not operating a client account at all (subject to informing clients about where and how their money is held).

Key Term: Legal Aid Agency (LAA)

A government body that pays solicitors and counsel for services to eligible clients. LAA payments for the firm’s costs are treated as business money under the Rules.

Worked Example 1.17

An LAA-funded criminal matter pays £1,200 (firm’s costs). How is the receipt posted?

Answer:

DR £1,200 Cash Account (Business); CR £1,200 Client Ledger (Business) or appropriate income ledger postings per internal policy. No client account involvement.

Breaches: Duty to Correct and Documentation (Rule 6.1)

Any breach (e.g., miss-posting, early withdrawal, deficit) must be corrected promptly upon discovery. For financial breaches:

- Replace missing client money immediately from business bank.

- Reverse any incorrect entries and post correct ones.

- Record full details: what happened, amount, matters affected, date discovered, date corrected, cause, remedial steps, and process changes.

The COFA should maintain a breaches log and report material breaches promptly to the SRA.

Worked Example 1.18

A mixed receipt of £4,000 (including £600 business money) was paid into the business bank by mistake. What is the correction?

Answer:

Immediate cash transfer of the £3,400 client element to client bank: DR £3,400 Cash Account (Client); CR £3,400 Cash Account (Business); CR £3,400 Client Ledger (Client); DR £3,400 Client Ledger (Business) if a temporary misposting occurred there as well. Document the breach and correction.

Reconciliations—practical pointers

- Three-way reconciliation must tie (bank statement balance vs cash book vs total of all client ledger balances).

- Show and explain outstanding cheques, lodgements in transit, or bank errors explicitly.

- A manager or COFA must sign off each reconciliation.

- Investigate and resolve differences immediately (not in the next cycle).

- Keep a schedule of suspense items with resolution plans and target dates.

Worked Example 1.19

At month end, client bank statement shows £1,206,800; cash book shows £1,204,800; client ledger aggregate shows £1,204,800. Two cheques totalling £2,000 are outstanding. Is the reconciliation balanced?

Answer:

Yes. Bank statement balance £1,206,800 less outstanding cheques £2,000 equals £1,204,800, which matches both the cash book and aggregate client ledger balances.

Bad debts and VAT relief—business ledgers only

Where a billed debt becomes irrecoverable and is written off after six months, the firm may reclaim the VAT element under VAT rules. These are postings entirely in business ledgers (bad and doubtful debts, HMRC-VAT) and do not touch client money. Ensure the original output VAT was declared and the write-off complies with HMRC rules.

Worked Example 1.20

A bill of £1,200 + £240 VAT is irrecoverable and written off 7 months later. What VAT action is available?

Answer:

Claim VAT bad debt relief for £240. Post CR Client Ledger (Business) £1,440 to reverse out the receivable, DR Bad Debts £1,200 and DR HMRC-VAT £240 (relief). No client account entries.

Handling mortgage advances—single or dual ledger method

If acting for both borrower and lender:

- Separate ledgers method: Receipt of mortgage advance is recorded in the lender’s ledger and inter‑client transfer on completion to borrower’s ledger.

- Single (borrower) ledger method: Record the mortgage advance in borrower’s ledger, with details identifying the lender and labelling the receipt as “mortgage advance”.

In both methods, ensure mortgage funds are not used before completion; the lender’s money should remain clearly identifiable until the completion moment.

Worked Example 1.21

Mortgage advance £150,000 is received. The firm uses the single borrower ledger method. What is the entry?

Answer:

DR £150,000 Cash Account (Client); CR £150,000 Borrower’s Client Ledger (Client), with details naming the lender and identifying “mortgage advance”.

Reconciling stakeholder/agent deposits at completion

At completion:

- Stakeholder deposit: transfer from stakeholder ledger (or annotated stakeholder amount) into seller’s client ledger before disbursing to the seller.

- Agent-held deposit: already in seller’s ledger; ensure the completion statement incorporates it and pay balances accordingly.

Worked Example 1.22

A £25,000 stakeholder deposit was recorded in a separate stakeholder ledger. On completion, £400,000 completion monies arrive. What steps occur?

Answer:

Receipt of £400,000: DR Cash Account (Client); CR Seller’s Client Ledger (Client). Transfer of deposit: DR Stakeholder Ledger (Client); CR Seller’s Client Ledger (Client). Then pay the net balance to the seller and disburse mortgage redemption/fees as per the completion statement.

Policies, procedures and evidence—Rule 8 in practice

A robust system includes:

- Written policy on mixed receipts (allocation/ timescales).

- Written interest policy (thresholds, calculation method).

- Withdrawal authorisation matrix (who may authorise what, and evidence required).

- Daily posting procedures with segregation of duties between fee earners and accounts where possible.

- Five-week reconciliations and monthly COFA review.

- Breaches log with root-cause analysis and process fixes.

- Central register of bills.

- Data retention policy (six years minimum for accounting records).

Worked Example 1.23

The firm’s policy states all mixed receipts must be allocated within one working day. A sample reveals two instances allocated on day three. What should follow?

Answer:

Record minor breaches, correct without delay, notify the COFA, and strengthen training/process controls. If delays suggest widespread issues, escalate remedial measures (e.g., staffing backup, diary alerts).

Preventing and detecting misuse of client account

Risk indicators include:

- Frequent requests to pass funds through client account unconnected to legal work.

- High‑value transfers with limited documentation or unclear instructions.

- Persistent residual balances with little movement.

- Use of client account after matters are complete.

- Client without a UK bank insisting on onward payments to third parties.

Controls:

- Insist on documented instructions linked to a current legal matter.

- Decline to accept funds unrelated to legal work.

- Verify sources and purposes in higher‑risk matters (consistent with anti‑money laundering obligations).

- Return funds promptly at completion/closure.

Worked Example 1.24

A corporate client asks you to receive monthly supplier payments and re‑route them to overseas vendors to “save time.” There is no ongoing legal work. What do you do?

Answer:

Decline. Using client account for commercial payment processing, without a legal nexus, would breach Rule 3.3 and create money‑laundering risk.

Documentation and narrative—make postings self‑evident

Each ledger entry should state:

- Date, payee/payer, amount;

- Purpose (e.g., “HMCTS issue fee,” “Bill 12345,” “Counsel invoice ref ABC”);

- Whether the payment/receipt is client or business money;

- Cross‑references to supporting documents (bill number, invoice ref, completion statement/estate account).

Good narratives accelerate audits, complaint resolution, and internal checks. Poor narratives undermine compliance evidence.

Worked Example 1.25

Which narrative is preferable for a client account payment?

Answer:

“CR £255 HM Land Registry Title and OS1 fees (Inv 45678, agency), Matter 1234-1” is superior to “Land Registry fee,” as it states the nature (agency), identifies the invoice and matter, and clarifies permitted purpose.

Residual client balances—tracing steps

Reasonable steps may include:

- Checking the file and correspondence for updated details.

- Contacting by email, telephone, last known address.

- Using an affordable tracing service/letter‑forwarding scheme where justified by the balance.

- Considering electoral roll search or other proportionate search.

- Documenting all attempts and decisions.

Key Term: residual client balance

Money left in client account after matter closure where the rightful owner cannot be traced or no longer requires the funds. Under prescribed conditions, sub‑£500 balances may be paid to charity with documented attempts to trace the owner.

Worked Example 1.26

A residual balance of £480 has been held for four years. Searches and a letter‑forwarding service failed. What postings apply on payment to charity?

Answer:

CR £480 Cash Account (Client); DR £480 Client Ledger (Client). Add central register entry, retain the charity’s receipt/indemnity and tracing records for six years.

Authorising withdrawals—practical safeguards

- Require two signatories (or dual electronic authorisation) for client account payments over a threshold.

- Mandate support documentation (bill, completion statement, client written authority).

- Review sufficient funds on the client ledger immediately before authorising.

- Periodically sample‑check authorisations vs supporting documents.

Worked Example 1.27

A partner authorises a client account payment of £12,000 to “ABC Ltd” without a completion statement or instructions on file. Is this compliant?

Answer:

No. Withdrawals must be for a permitted purpose and appropriately authorised with supporting evidence. Require proper documents before authorising and investigate why they were absent.

Accountants’ reports and record retention

Firms that at any time during the accounting period held/received client money, or operated a joint account or a client’s own account as signatory, must obtain an accountant’s report within six months of the period end. Only qualified reports (indicating risk to client money) must be delivered to the SRA; however, firms must still obtain the report unless exempt (e.g., only LAA money, or balances below set thresholds).

All accounting records (including reconciliations, statements, bills registers, breach records) must be securely stored and retained for at least six years.

Worked Example 1.28

A small firm held only LAA payments for its costs during the year and no other client money. Does it need an accountant’s report?

Answer:

No, provided it falls within the exemption criteria and has informed clients appropriately. If it subsequently holds other client money, the exemption may cease to apply.

Putting it all together—end‑to‑end posting flow (property sale)

- Receive buyer’s funds (stakeholder deposit or completion monies) into client bank: DR cash (client); CR seller’s client ledger (client) or stakeholder ledger (client) as appropriate.

- On completion, transfer stakeholder deposit to seller’s ledger (if applicable).

- Pay mortgage redemption and other disbursements from client bank (agency items VAT‑inclusive where invoices are in the client’s name).

- Deliver the firm’s bill for fees and VAT and transfer costs from client bank to business bank under Rule 4.3.

- Pay net proceeds to the client promptly.

- Close the ledger with a zero client balance; return any residual amount promptly; document and file closure.

Worked Example 1.29

Show the sequence for a simple sale: deposit £20,000 (stakeholder), completion receipt £380,000, mortgage redemption £200,000, the firm’s bill £2,400 (£2,000 + £400 VAT), net to client thereafter.

Answer:

Exchange: DR £20,000 Cash (Client); CR £20,000 Stakeholder Ledger. Completion receipt: DR £380,000 Cash (Client); CR £380,000 Seller’s Client Ledger (Client). Transfer stakeholder: DR £20,000 Stakeholder; CR £20,000 Seller’s Client Ledger (Client). Pay mortgage: CR £200,000 Cash (Client); DR £200,000 Seller’s Client Ledger (Client). Bill issue: DR £2,000 and £400 to Client Ledger (Business); CR Profit Costs £2,000; CR HMRC-VAT £400. Transfer costs: CR £2,400 Cash (Client); DR £2,400 Client Ledger (Client); DR £2,400 Cash (Business); CR £2,400 Client Ledger (Business). Pay net to client: CR £197,600 Cash (Client); DR £197,600 Seller’s Client Ledger (Client).

Worked Example 1.30

A mixed receipt of £3,000 arrives by bank transfer: £2,100 to settle a delivered bill and £900 for future disbursements. Firm policy is to bank to client account and transfer the business element promptly. Complete the postings.

Answer:

Receipt: DR £3,000 Cash (Client); CR £3,000 Client Ledger (Client). Transfer business element: CR £2,100 Cash (Client); DR £2,100 Client Ledger (Client); DR £2,100 Cash (Business); CR £2,100 Client Ledger (Business). £900 remains as client money to fund future disbursements.Revision Tip: When you are unsure where to post, ask these three questions in order:

- Which two ledgers are affected (cash sheet and client ledger, or two client ledgers for inter‑client transfers)?

- Is the movement client or business money?

- Which side is DR and which is CR? (Money in: DR cash; Money out: CR cash; Client money held increases as a CR on the client column; Business receivable increases as a DR on the business column.)

Key Point Checklist

This article has covered the following key knowledge points:

- Client and business money must be kept separate, both in banking and in ledgers; use dual column ledgers and cash accounts to preserve segregation and clarity.

- Double‑entry bookkeeping applies to every transaction; map DR/CR to cash and to client/business columns consistently.

- Record receipts and payments promptly; handle mixed receipts under Rule 4.2 according to firm policy and allocate within one working day as best practice.

- Transfer client money to business bank only after a bill or written notification under Rule 4.3, and only for the specific sum billed.

- Inter‑client and inter‑matter transfers are ledger‑only (no cash entries) and require written authority and audit trail.

- Authorise withdrawals properly (Rule 5.2); check sufficiency of client‑specific funds before paying (Rule 5.3); replace any deficit immediately (Rule 6.1).

- Reconcile client account at least every five weeks; investigate and resolve differences immediately; keep signed reconciliation records.

- Maintain a central register of all bills (Rule 8.4) and retain accounting records and breach logs for at least six years.

- Calculate and post interest correctly: pooled client account—sum in lieu from business; SDDCAs—interest belongs to the client.

- Do not use client account as a banking facility (Rule 3.3); only receive/hold/move funds connected to regulated legal services.

- Operate joint accounts, clients’ own accounts and TPMAs with modified controls; obtain statements and reconcile as required; notify the SRA when using TPMAs.

- Prevent residual balances; where unavoidable, manage charitable payment protocol under prescribed conditions and keep a central register.

- Understand disbursement VAT: agency vs principal methods; pay agency disbursements from client bank and principal disbursements from business bank.

- Meet accountant’s report obligations unless exempt; secure storage and retention of records for six years.

Key Terms and Concepts

- SRA Accounts Rules

- double-entry bookkeeping

- debit (DR)

- credit (CR)

- journal entries

- business money

- client money

- client account

- ledger

- cash account

- dual column ledger

- client ledger

- client account reconciliation

- Compliance Officer for Finance and Administration (COFA)

- central record of bills

- interest policy

- inter-client transfer

- separate designated deposit client account (SDDCA)

- client account (use restriction)

- mixed receipt

- stakeholder deposit

- agent-held deposit

- joint account

- client’s own account

- third‑party managed account (TPMA)

- Legal Aid Agency (LAA)

- residual client balance