Learning Outcomes

This article outlines beneficial entitlement in trusts—fixed versus discretionary and vested versus contingent—and shows how these classifications affect beneficiaries’ rights, trustees’ duties, and SQE1 problem‑question analysis, including:

- Distinguishing life interests, remainder interests, and interests vested in possession versus vested in interest, and identifying them in typical exam fact patterns

- Analysing contingent interests and vesting; conditions precedent and subsequent, gifts over, and what happens on failure of a condition

- Applying tests for certainty of objects: the given postulant test for discretionary trusts and the complete list test for fixed trusts, with common pitfalls

- Understanding the rule against perpetuities, the modern 125‑year period, “wait and see,” and how perpetuity rules impact contingent gifts and powers

- Comparing beneficiaries’ rights under fixed, discretionary, and bare trusts; using Saunders v Vautier and related principles to determine when a trust can be collapsed early

- Evaluating when vested equitable interests may be transferred, assigned, disclaimed, or varied, and the formal requirements of s53(1)(c) Law of Property Act 1925

- Explaining trustees’ core duties when administering different interest types, including investment choices, periodic review of discretionary powers, and statutory powers of maintenance (s31 TA 1925) and advancement (s32 TA 1925)

SQE1 Syllabus

For SQE1, you are required to understand the types of beneficial interests that can arise under a trust and their practical implications, with a focus on the following syllabus points:

- The distinction between fixed and discretionary interests in trusts

- The difference between vested and contingent interests

- The effect of these interests on beneficiaries’ rights and trustees’ duties

- How to identify and apply the correct legal rules to trust scenarios involving these interests

- The tests for certainty of objects in fixed versus discretionary trusts (complete list vs given postulant)

- Administrative unworkability and capriciousness in discretionary trusts

- The rule in Saunders v Vautier for terminating trusts when beneficiaries are absolutely entitled and sui juris

- Statutory powers of maintenance and advancement and their impact on enjoyment and timing of interests

- The rule against perpetuities, including modern 125-year periods, “wait and see,” and gifts over

- Formalities for disposition or assignment of equitable interests (s53(1)(c) LPA 1925)

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following best describes a discretionary trust?

- a) Each beneficiary is entitled to a fixed share of the trust property

- b) Trustees must distribute all income equally

- c) Trustees have discretion over who benefits and in what amount

- d) The trust must terminate on a fixed date

-

True or false? A vested interest gives a beneficiary an immediate right to trust property, even if enjoyment is postponed.

-

In which situation does a contingent interest arise?

- a) The beneficiary is absolutely entitled

- b) The beneficiary must satisfy a condition before becoming entitled

- c) The beneficiary is a trustee

- d) The trust is charitable

-

Can a beneficiary with a vested interest transfer that interest to another person before receiving the trust property?

Introduction

Beneficial entitlement determines who benefits from a trust and on what terms. For SQE1, you must be able to identify and explain the main types of beneficial interests: fixed, discretionary, vested, and contingent. These interests affect the rights of beneficiaries, the powers and duties of trustees, and the administration of trusts. Understanding these distinctions is essential for answering exam questions and advising clients on trust matters.

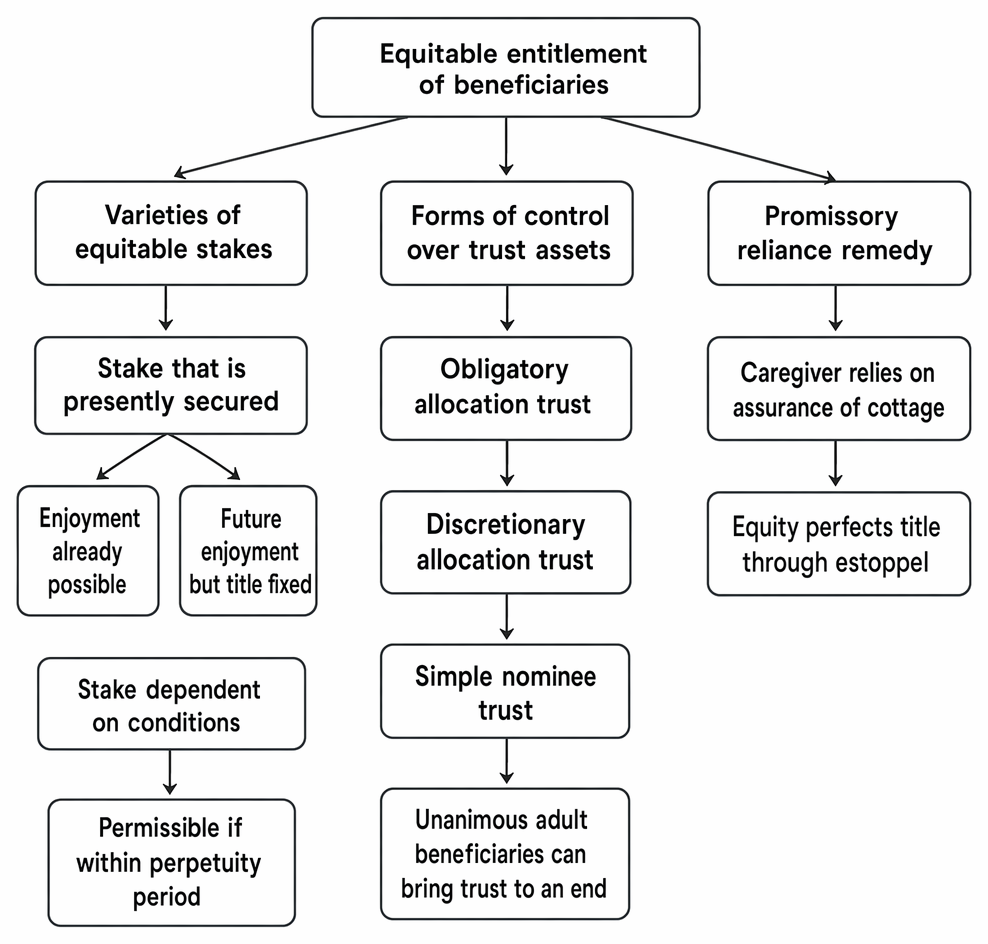

Beneficial entitlement comprises fixed and discretionary trusts, vested and contingent interests, bare trusts, Saunders v Vautier, and proprietary estoppel.

Beneficial entitlement also governs whether a beneficiary is entitled to capital, income, or both, and when. The settlor can design a trust so that one person has present enjoyment of income (for example, a life tenant) while another has future enjoyment of capital (the remainderman). This allocation of capital and income frequently interacts with statutory rules on maintenance and advancement, and with the general principles on certainty, perpetuities, and formalities.

Key Term: fixed interest

A fixed interest is where the trust instrument specifies exactly what each beneficiary is entitled to receive from the trust property. Key Term: discretionary interest

A discretionary interest is where the trustees have the power to decide which beneficiaries receive trust property, how much, and when. Key Term: vested interest

A vested interest is an immediate right to trust property, even if enjoyment is postponed until a future date. Key Term: contingent interest

A contingent interest is a right to trust property that depends on the occurrence of a specified event or condition. Key Term: interest in possession

A present right to present enjoyment of the trust property, typically an immediate right to income or use. Key Term: interest in remainder

A present right to future enjoyment of capital that will become possessory when a prior interest ends (for example, on the life tenant’s death).

Fixed and Discretionary Interests

A trust may confer either a fixed or a discretionary interest on its beneficiaries. The distinction is fundamental to the operation of the trust and the rights of those involved.

Fixed Interests

In a fixed trust, the settlor determines in advance the share or entitlement of each beneficiary. The trustees have no discretion over the division of the trust property. For example, a trust "for A and B in equal shares" gives each beneficiary a fixed entitlement.

Fixed interests provide certainty for beneficiaries and simplify the trustees’ duties. Trustees are under a duty to distribute in accordance with the terms of the trust at the correct time to the correct people. If the trust is silent on shares, equal shares are generally implied among co-beneficiaries. A beneficiary under a fixed interest has a proprietary equitable right they can enforce; where they are absolutely entitled and sui juris, they may be able to terminate the trust early (see Saunders v Vautier below).

Trustees of fixed trusts must also mind the timing and nature of enjoyment. For instance, if a minor has a vested fixed interest, trustees will hold until majority, applying statutory powers of maintenance to income where appropriate.

Discretionary Interests

In a discretionary trust, the trustees decide which beneficiaries (from a defined class) will benefit, in what amounts, and at what times. The settlor gives the trustees discretion to respond to changing needs or circumstances.

Discretionary interests allow flexibility and can protect vulnerable beneficiaries, but beneficiaries have no guaranteed right to any part of the trust property until the trustees exercise their discretion in their favour. Trustees should periodically consider whether to exercise their powers, appreciate the “width of the field,” and act impartially among potential objects. Courts will not force trustees to exercise discretion in a particular way but may intervene if power is not considered at all, is exercised capriciously, or the class is so wide that the trust is administratively unworkable.

Until the trustees exercise their discretion in favour of a particular object, no object has a proprietary right to any defined part of the trust fund. Their rights are instead rights of due administration: to have the trustees consider the power properly, within a reasonable time, for proper purposes, and within the defined class. Once trustees validly appoint income or capital to an object, that person acquires an enforceable right to the property appointed.

Key Term: given postulant test

The test for certainty of objects in discretionary trusts: for any given individual, can it be said with certainty whether they are or are not within the class? Key Term: administrative unworkability

A discretionary trust may fail if the class is so wide that the trustees cannot sensibly survey and consider its members or make rational distributions.

Worked Example 1.1

A trust states: "to my three children in equal shares." What type of interest do the children have?

Answer:

Each child has a fixed interest. The trustees must divide the trust property equally, and each child is entitled to a specific share.

Worked Example 1.2

A trust states: "to my trustees to distribute income among my grandchildren as they think fit." What type of interest do the grandchildren have?

Answer:

The grandchildren have discretionary interests. The trustees decide who receives income and how much, and no grandchild is entitled to a fixed share.

Worked Example 1.3

A will creates "a discretionary trust for any of my employees and ex-employees." Is this trust valid for certainty of objects?

Answer:

The class description is conceptually clear enough to apply the given postulant test (it is possible to determine for any given person whether they are an employee or ex-employee). However, if the class is extremely numerous relative to the fund, the trust risks being administratively unworkable; this is assessed case by case.

Worked Example 1.4

A trust says: "to be held for my friends as the trustees think fit." Is this conceptually certain?

Answer:

"Friends" is typically conceptually uncertain for a discretionary trust, so the trust would fail for lack of certainty of objects. By contrast, a condition precedent gift allowing “any friend” to take a specific benefit (for example, to purchase a painting at a discount) may be workable because each claimant proves they qualify, and the quantum others receive does not depend on that proof.

Vested and Contingent Interests

Beneficiaries’ interests may also be classified as vested or contingent, depending on whether there are conditions attached to their entitlement.

Vested Interests

A vested interest arises when a beneficiary is identified and does not need to satisfy any further condition to become entitled. The beneficiary may have to wait to receive the property (for example, until reaching a certain age or the life tenant’s death), but the right exists now. If the beneficiary dies before receiving the property, the interest passes to their estate.

Vested interests include those vested in possession (present enjoyment) and those vested in interest (future enjoyment). Both are generally transferable and may be disclaimed or assigned, subject to any express restrictions in the trust instrument and compliance with statutory formalities when disposing of an equitable interest.

A classic successive-interest arrangement is a life interest trust. The life tenant has an interest in possession in the income or use of the trust property during their lifetime, while the remainderman has the future capital interest. That remainder may itself be vested (for example, “to B absolutely after A’s death”) or contingent (for example, “to B if B survives A”).

Contingent Interests

A contingent interest arises when a beneficiary’s entitlement depends on meeting a condition (for example, reaching a certain age, surviving a named person, or qualifying in a profession). If the condition is not met within the relevant period, the interest never vests. If there is no effective gift over, the property may revert on resulting trust to the settlor or their estate.

Contingent interests are less secure and may be lost if the condition fails. They are not usually transferable before vesting, and beneficiaries cannot compel trustees to transfer capital until the condition is satisfied. Where a beneficiary with a contingent interest reaches majority, statutory maintenance rules can entitle them to income until vesting unless a prior interest subsists or the disposition is a contingent pecuniary legacy.

Worked Example 1.5

A trust states: "to my son if he reaches age 25." The son is currently 20. What type of interest does he have?

Answer:

The son has a contingent interest. He will only become entitled if he reaches age 25.

Worked Example 1.6

A trust states: "to my daughter for life, then to my grandson absolutely." The grandson is 12. What type of interest does the grandson have?

Answer:

The grandson has a vested interest in remainder. He is identified and does not need to satisfy any further condition, but his enjoyment is postponed until the daughter’s death.

Worked Example 1.7

A trust provides: "to W for life, remainder to Y if Y attains 25." Y is 22. W dies when Y is 24. What happens?

Answer:

Y’s remainder is contingent on attaining 25. Because Y did not satisfy the condition by the time the remainder would otherwise fall into possession, Y’s interest fails. The property passes in accordance with any valid gift over; if none, it reverts on automatic resulting trust to the settlor or their estate.

Worked Example 1.8

A beneficiary B has "a vested one‑third share in capital," with enjoyment postponed until they turn 21. B, aged 19, wishes to assign their vested equitable interest to C. Is this possible?

Answer:

A vested equitable interest is generally assignable. However, the disposition of B’s equitable interest must comply with s53(1)(c) Law of Property Act 1925 (writing signed by B). If formalities are met, the assignment is effective even though B’s enjoyment is postponed.

The Rule Against Perpetuities

All contingent interests must vest, if at all, within the perpetuity period to avoid tying up property indefinitely. For most modern private trusts, the Perpetuities and Accumulations Act 2009 permits an express perpetuity period of up to 125 years. If none is specified, the statutory period of 125 years applies to dispositions within scope. Earlier “lives in being plus 21 years” rules and the “wait and see” approach under the Perpetuities and Accumulations Act 1964 may be relevant for older instruments.

Key Term: rule against perpetuities

The legal rule that prevents interests in property from vesting too far in the future, requiring that they must vest within a set period (commonly 125 years under the 2009 Act for private trusts).

When considering whether a contingent interest is valid:

- Identify whether the trust instrument specifies a perpetuity period (up to 125 years).

- If not, apply the statutory default period (typically 125 years for modern trusts).

- “Wait and see” may save a gift if it does in fact vest within the period; speculative worst‑case scenarios need not invalidate it at the outset under modern rules.

Worked Example 1.9

A settlement provides: "£100,000 for the first grandchild of A to reach 21," with no period specified. A has no grandchildren at the date of the settlement. Is the gift valid?

Answer:

Under modern law, an express period of up to 125 years could have been specified. If none is specified and the statutory 125‑year period applies, trustees can “wait and see” whether the gift vests within that time. If a grandchild reaches 21 within 125 years, the gift is valid; if not, it fails at the end of the period.

Beneficiaries’ Rights and Trustees’ Duties

The type of beneficial interest affects both the rights of beneficiaries and the duties of trustees.

- Beneficiaries with fixed or vested interests can generally enforce their rights and may transfer their interests. Trustees must distribute in accordance with the terms and timing prescribed in the instrument and comply with duties of care and impartiality.

- Beneficiaries with discretionary or contingent interests have no enforceable right until the trustees exercise their discretion or the condition is satisfied. They do, however, have a right to be considered fairly and for trustees to periodically review whether to exercise their powers.

Key Term: beneficiary principle

The principle that a private trust must have identifiable beneficiaries who can enforce the trust. Key Term: certainty of objects

The requirement that the class of beneficiaries is defined with sufficient clarity so that the trustees and the court can determine who is entitled.

In administering trusts:

- For fixed trusts, trustees must identify all beneficiaries and their shares (complete list test) and distribute at the proper time.

- For discretionary trusts, trustees must apply the given postulant test to any given claimant for conceptual certainty, avoid capricious decisions, and ensure the trust is not administratively unworkable.

Trustees must also consider statutory powers impacting timing and enjoyment:

- Maintenance (s31 Trustee Act 1925, as amended) permits trustees to apply income for minor beneficiaries’ maintenance, education, or benefit, with accumulation rules and a right to income at 18 unless a prior interest exists.

- Advancement (s32 Trustee Act 1925, as amended) allows trustees to apply capital in advance for the benefit of a beneficiary entitled to capital in the future, subject to conditions and any express restrictions in the trust instrument.

Key Term: bare trust

A trust where trustees hold property for a single adult beneficiary absolutely; the beneficiary can require transfer of legal title and direct trustees’ actions. Key Term: Saunders v Vautier

The rule that if all beneficiaries are adult, of full capacity, and together absolutely entitled to the whole beneficial interest, they can require trustees to transfer the trust property to them and terminate the trust.

Worked Example 1.10

A trustee holds £150,000 on bare trust for X, who is 21. X instructs the trustee to invest the entire sum according to X’s plan. Must the trustee comply?

Answer:

Yes. In a bare trust, the adult beneficiary who is absolutely entitled can direct the trustee’s actions regarding the trust property, including investment strategy, and can require transfer of legal title.

Worked Example 1.11

A will leaves shares "on trust for P for life, remainder to Q absolutely." P and Q, both adults of full capacity, wish to terminate the trust and share capital now. Can they compel the trustees to do so?

Answer:

Yes. Together, P (life tenant) and Q (remainderman) are absolutely entitled to the whole beneficial interest. Under Saunders v Vautier, they can require trustees to transfer the property to them and end the trust, agreeing between themselves on apportionment.

Worked Example 1.12

A trust provides capital "for A if A qualifies as a solicitor." At 18, A wants the capital now and proposes ending the trust with the agreement of the settlor’s personal representatives. Is this possible?

Answer:

A’s interest is contingent and not vested. A alone cannot end the trust; however, if all persons who would be absolutely entitled in every eventuality (for example, A plus those entitled in default or on resulting trust) are adult and consent, they may collectively terminate under Saunders v Vautier. If there is no valid gift over and the settlor’s estate would take on resulting trust, agreement of the personal representatives would be needed.

Trustees’ decision‑making in discretionary trusts

Trustees exercising discretionary dispositive powers must:

- Consider periodically whether to exercise the power.

- Take relevant factors into account and ignore irrelevant ones.

- Act impartially and in good faith.

- Avoid capriciousness and ensure decisions are within the class definition and consistent with any purposes expressed.

Trustees are not obliged to give reasons for discretionary distributions, but if they volunteer reasons, courts may review those reasons to ensure proper exercise of discretion. Trustees should keep adequate records of deliberations and take advice where appropriate (for example, on tax or investment), consistent with their duty of care.

Formalities for transferring equitable interests

A beneficiary with a vested equitable interest may transfer or assign that interest. Any disposition of a subsisting equitable interest must generally be in writing signed by the person disposing (s53(1)(c) LPA 1925). A direction to transfer legal title may, in some scenarios, simultaneously transfer the equitable interest without separate written disposition, but care is needed and the orthodox route is written assignment. Disclaimers operate by avoidance and are not dispositions; protective trusts and express restrictions may limit alienation.

Exam Warning: In discretionary trusts, beneficiaries cannot compel trustees to distribute property in their favour. They only have the right to be considered. Do not confuse this with fixed trusts, where beneficiaries can enforce their entitlement.

Revision Tip: For SQE1, always check whether a beneficiary’s interest is vested or contingent, and whether the trust is fixed or discretionary. This will determine their rights and the trustees’ obligations. Remember the modern perpetuity period (often 125 years) and that statutory maintenance and advancement can affect timing of enjoyment. Where all adult beneficiaries together are absolutely entitled, consider whether Saunders v Vautier applies.

Summary

| Type of Interest | Description | Rights of Beneficiary |

|---|---|---|

| Fixed | Set share specified by trust | Enforceable right to that share |

| Discretionary | Trustees decide who benefits and in what amount | Right to be considered, not to share |

| Vested | Immediate right (may be postponed) | Transferable, passes to estate |

| Contingent | Right depends on meeting a condition | No right until condition satisfied |

Key Point Checklist

This article has covered the following key knowledge points:

- The distinction between fixed and discretionary interests in trusts, including trustees’ duties in each model

- The difference between vested and contingent interests, and how postponement versus conditionality affects entitlement

- How the type of interest affects beneficiaries’ rights (including enforcement, transfer, and early termination under Saunders v Vautier)

- The application of the rule against perpetuities to contingent interests, modern 125‑year periods, and “wait and see”

- The importance of the beneficiary principle and certainty of objects in private trusts, with tests tailored to fixed versus discretionary trusts

- The given postulant test, administrative unworkability, and capriciousness in discretionary trusts

- Statutory powers of maintenance (s31 TA 1925) and advancement (s32 TA 1925) and their impact on timing and enjoyment

- Formalities for disposition of equitable interests under s53(1)(c) LPA 1925 and the effect of disclaimers

Key Terms and Concepts

- fixed interest

- discretionary interest

- vested interest

- contingent interest

- interest in possession

- interest in remainder

- given postulant test

- administrative unworkability

- rule against perpetuities

- beneficiary principle

- certainty of objects

- bare trust

- Saunders v Vautier