Learning Outcomes

This article explains the legal definition and core requirements of charitable trusts in England and Wales, with particular emphasis on the statutory framework in the Charities Act 2011. It explains how a purpose must fall within a recognised charitable head, satisfy the public benefit requirement in both its benefit and public aspects, and be exclusively charitable to achieve valid charitable status. The article explains how these tests are applied in practice, illustrating classification of trusts as charitable or non-charitable, distinctions between charitable trusts, private trusts and non-charitable purpose trusts, and typical reasoning used in single best answer MCQs. It also explains key ancillary doctrines that commonly feature in exam questions, including: the approach to fee‑charging charities and access policies, treatment of “personal nexus” beneficiary classes, the limits on political purposes and permissible campaigning, and the function and limits of the cy‑près doctrine when purposes fail or circumstances change. Finally, the article explains the distinctive enforcement, perpetuity, and regulatory features that flow from charitable status.

SQE1 Syllabus

For SQE1, you are required to understand the fundamental legal principles governing charitable trusts, particularly how they are defined and what makes them valid, including differentiating them from private trusts and non-charitable purpose trusts, with a focus on the following syllabus points:

- The statutory definition of charity under the Charities Act 2011, including the concept of an “institution” and High Court control.

- The recognised charitable purposes listed in the Charities Act 2011, including the “any other analogous purposes” and recreational provisions.

- The requirement for public benefit, including its two aspects (identifiable benefit and benefit to the public or a sufficient section).

- The requirement that the trust's purposes must be exclusively charitable, the effect of mixed wording (e.g., “charitable or benevolent”), and what counts as incidental private benefit.

- The limits on political purposes and the distinction between charitable purposes and permissible ancillary campaigning.

- The key characteristics that distinguish charitable trusts from private trusts (e.g., enforcement, beneficiary principle exemption, perpetuity rules, tax advantages).

- The cy‑près doctrine (initial vs subsequent failure, general charitable intention, statutory grounds for schemes) and how it avoids failure of charitable gifts.

- The practical issues commonly examined in charity problems (fee‑charging charities’ access policies; personal nexus classes; cloistered religious orders; research and dissemination requirements).

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which Act primarily governs the definition and regulation of charities in England and Wales?

- a) Trustee Act 2000

- b) Law of Property Act 1925

- c) Charities Act 2011

- d) Inheritance Act 1975

-

Which of the following is NOT a requirement for a trust to be charitable?

- a) It must have a charitable purpose recognised by law.

- b) It must be for the public benefit.

- c) It must have specifically named individual beneficiaries.

- d) Its purposes must be exclusively charitable.

-

A trust established to provide scholarships for the children of employees of a specific large company generally fails which test for charitable status?

- a) Certainty of intention

- b) Exclusively charitable purpose

- c) Public benefit (due to personal nexus)

- d) Charitable purpose recognition

Introduction

When establishing a trust, the settlor may intend for it to benefit specific individuals (a private trust) or to achieve a particular purpose. Trusts for purposes can be divided into non-charitable purpose trusts and charitable trusts. Charitable trusts hold a special status in law due to their aim of benefiting society. This article focuses on the definition and essential characteristics of charitable trusts as outlined by the Charities Act 2011 (CA 2011), which is the primary legislation governing charities in England and Wales. Understanding these requirements is essential for advising clients and for success in the SQE1 assessments.

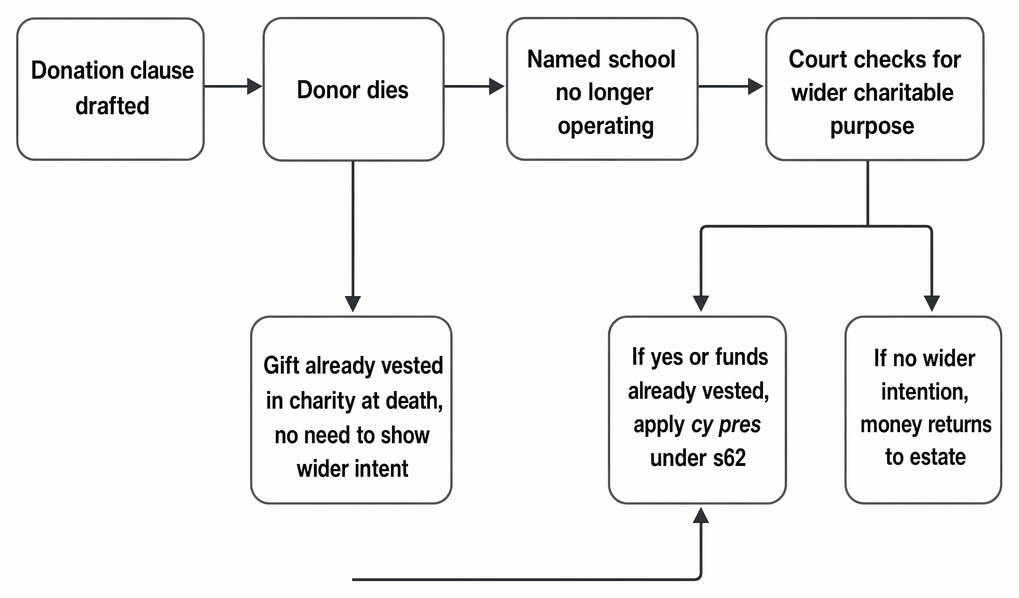

Failed testamentary gift to a named school is applied cy-près on wider intention or vesting; otherwise it returns to the estate.

Charitable trusts differ fundamentally from non-charitable purpose trusts. Private purpose trusts generally fail for lack of human beneficiaries (the beneficiary principle), subject to narrow exceptions (e.g., maintenance of particular animals or graves) and the Re Denley line, where an identifiable group can enforce the purpose. Charitable trusts are exempt from this beneficiary principle because their public purposes are supervised by the Charity Commission and enforced by the Attorney General, and they benefit from additional doctrines (notably cy‑près) that help them survive changes in circumstances.

Test Tip: In SQE-style questions on Definition and characteristics of charitable trusts, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

The Definition of a Charity

Section 1(1) CA 2011 defines a charity as an institution which is established for charitable purposes only and falls under the control of the High Court concerning charities. For a trust to be recognised as a charity, it must satisfy three key requirements:

- It must have a purpose that falls within the list of recognised charitable purposes (s 3 CA 2011).

- It must be for the public benefit (s 4 CA 2011).

- Its purposes must be exclusively charitable.

The legislation uses “institution” broadly (s 9 CA 2011) so charities can be organised as trusts, companies limited by guarantee, unincorporated associations, CIOs, or other legal forms, provided their purposes are charitable only and they fall under the High Court’s jurisdiction. Registration with the Charity Commission engages regulatory oversight (e.g., reporting obligations) but is not what makes a body charitable; status depends on meeting the purposes and public benefit tests.

Key Term: Charity

An institution established for purposes recognised by law as charitable, which benefits the public and is subject to the High Court's jurisdiction regarding charities.

Requirement 1: Charitable Purpose

A trust cannot be charitable unless its purpose is recognised as charitable under the law. Section 3(1) CA 2011 provides a list of thirteen descriptions of purposes. These include well-established heads such as:

- The prevention or relief of poverty.

- The advancement of education.

- The advancement of religion.

- The advancement of health or the saving of lives.

- The advancement of citizenship or community development.

- The advancement of the arts, culture, heritage or science.

- The advancement of amateur sport.

- The advancement of human rights, conflict resolution or reconciliation.

- The promotion of religious or racial good relations or equality and diversity.

- The advancement of environmental protection or improvement.

- The relief of those in need (due to youth, age, ill-health, disability, financial hardship etc.).

- The advancement of animal welfare.

- The promotion of the efficiency of the armed forces or emergency services.

- Other purposes recognised under existing charity law or analogous to the listed purposes.

This list is comprehensive but not exhaustive, allowing for the recognition of new charitable purposes that align with the spirit of the Act. It should be read together with the recreational charities provision (now carried into CA 2011), which treats providing recreational facilities in the interests of social welfare as charitable where it meets the statutory criteria. A few practical points:

- Education extends beyond formal schooling to include training, scholarships, provision of equipment, upkeep of educational facilities, and research. Research is charitable where it is genuinely directed to charitable ends and is disseminated for public benefit (judicial emphasis has been placed on publication and utility).

- Arts, culture, heritage, and science must still yield genuine public value. In borderline cases, questions of artistic merit, scientific utility, or wider educational value may be important in showing that the purpose produces a recognisable public benefit.

- Religion includes theistic and non‑theistic belief systems (CA 2011 recognises both), provided the organisation’s activities are open to the public or otherwise benefit the wider community (see “Public Benefit” below).

- Amateur sport must further health by involving physical or mental skill or exertion. A sport with negligible health benefit may not fit this head, but it may still be charitable under the recreational/social welfare provisions if the relevant statutory conditions are met.

- Human rights, conflict resolution, and equality heads are recognised but require care when activities verge into seeking changes in the law or government policy (see “Political Purposes” under Requirement 3).

Charity law also accepts “other purposes” analogous to the listed heads where courts or the Commission have historically treated them as charitable. The elasticity here supports recognition of evolving charitable aims, provided the purposes fall within charitable spirit and are capable of public benefit.

Requirement 2: Public Benefit

Simply having a purpose listed in s 3(1) CA 2011 is not sufficient; the purpose must also be for the public benefit (s 4 CA 2011). The concept of public benefit involves two aspects:

- Identifiable Benefit: The purpose must provide an identifiable benefit or benefits. The benefit must be clear and related to the charity's aims. Any detriment or harm resulting from the purpose must not outweigh the benefit.

- Benefit to the Public or a Section of the Public: The benefit must be available to the public at large or a sufficient section of the community.

Key Term: Public Benefit

The requirement that a charity's purpose must provide an identifiable benefit to the public in general or a sufficiently large section of it, without undue restrictions.

Determining whether the 'public aspect' is met can depend on the specific charitable purpose.

- Personal Nexus Test: For most charitable purposes (excluding the relief of poverty), if the potential beneficiaries are defined by their relationship to a specific individual or entity (e.g., employees of a particular company, members of a specific family), the trust is generally considered private and fails the public benefit test (Oppenheim v Tobacco Securities Trust Co Ltd [1951] AC 297). Uses of “my children” or “my employees” typically fail for education or other heads because the class is not a section of the public, but a closed personal nexus. This applies even if the group is very numerous.

- Poverty: Trusts for the relief of poverty are treated more leniently regarding the public aspect. A trust for one's 'poor relations' can be charitable, provided the individuals are not named. Courts have accepted that relieving poverty among a narrower class can still benefit the public, and case law has consistently tolerated personal nexus classes for poverty relief.

- Fees: Charities charging fees (e.g., independent schools, care homes) must ensure their services are accessible to a sufficient section of the public. If high fees effectively exclude those of modest means, the charity might fail the public benefit test unless it makes adequate provision for the less well‑off (e.g., scholarships, bursaries) (R (Independent Schools Council) v Charity Commission [2011] UKUT 421 (TCC)). Charging fees is not inherently inconsistent with charitable status, but trustees must adopt access policies that secure public benefit in fact, not merely in theory.

- Religion: Religious trusts generally satisfy the public aspect if worship or activities are open to the public, or if the adherents mix with the wider community. Closed or contemplative religious orders with no public interaction may fail the test (Gilmour v Coats [1949] AC 426). The law does not deny the significance of prayer, but insists on an outward community-facing benefit.

- Balancing Benefit and Detriment: The public benefit must outweigh any harm. For example, if the purpose is to end a practice that courts assess as highly beneficial to human health or science, the charity might fail the benefit limb. Courts have made this balancing explicit when assessing objects aimed at curtailing practices judged to aid medical progress.

Two additional practical points often overlooked:

- Incidental Private Benefit: A charity may confer some private benefit (e.g., wages to staff, contracts with service providers) provided those benefits are necessary and incidental to carrying out charitable purposes. If private benefit becomes a significant end in itself, it endangers charitable status.

- Geographical or Other Restrictions: Restricting a charity’s activities to a locality or to a public class defined by objective criteria (e.g., “older people living in X ward”, “children with Y condition”) is usually compatible with the public aspect; the real question is whether the restricted class is still a sufficient section of the public for the particular charitable head and whether access is not unreasonably limited.

Requirement 3: Exclusively Charitable Purpose

A trust must be established for exclusively charitable purposes. If a trust has both charitable and non-charitable purposes, it will generally fail as a charity unless the non-charitable purposes are merely incidental to the main charitable aim.

Key Term: Exclusively Charitable Purpose

The requirement that a charity must only have purposes that are legally recognised as charitable, with no non-charitable purposes unless they are purely incidental.

- Political Purposes: Trusts whose main purpose is political (e.g., advocating for a change in law, supporting a political party) cannot be charitable (McGovern v Attorney General [1982] Ch 321). This is not because political engagement is disfavoured, but because courts cannot judge whether proposed changes would deliver public benefit in the necessary charitable sense. However, engaging in political activities that are ancillary to achieving a charitable purpose (e.g., campaigning related to poverty relief, environmental protection, or educational awareness) is generally permissible, provided these activities are means to the charitable end rather than ends in themselves.

- Mixed Purposes: If a trust includes both charitable and non-charitable purposes, and the trustees can choose between them (e.g., a trust for 'charitable or benevolent purposes'), the trust will fail for not being exclusively charitable (Chichester Diocesan Fund v Simpson [1944] AC 341). The solution is careful drafting: “charitable purposes” is safe; “benevolent” or “philanthropic” is not, as such words extend beyond the legal definition of charity. Severance may sometimes be possible if the funds for charitable and non-charitable purposes are clearly delineated and the charitable parts are separable, but in many cases ambiguous wording will invalidate the gift.

If a non-charitable element is truly incidental or subsidiary to the main charitable aim, it does not defeat charitable status. Similarly, where the wording genuinely creates distinct severable charitable and non-charitable limbs, the court will preserve the charitable part if the language permits rather than striking down the whole gift.

Two further drafting cautions:

- Vagueness vs Charitable Spirit: Charitable purposes can be described in general language and remain valid if they are anchored to recognised charitable heads (e.g., “for the advancement of education by scholarships and educational resources”). Purpose clauses that combine charitable heads with non-charitable aims, or that direct funds to private activities without public benefit, risk invalidity.

- Private Benefit Dominating: Even if purposes are described in charitable terms, if the structure delivers a significant private benefit (e.g., profits to members or owners), charitable status is jeopardised. Where activities generate surpluses, profits must be ploughed back into the charitable objects.

Worked Example 1.1

A wealthy individual leaves £1,000,000 in their will to trustees 'to provide educational bursaries for the children of the employees of my company, Tech Giant Ltd'. Tech Giant Ltd employs 50,000 people worldwide. Is this likely to be a valid charitable trust?

Answer:

This trust is unlikely to be valid as a charity. Although the advancement of education is a recognised charitable purpose, the trust likely fails the public benefit requirement. The beneficiaries are defined by their personal connection (employment relationship) to a specific entity (Tech Giant Ltd). Following Oppenheim, this creates a 'personal nexus' that prevents the group from being considered a sufficient section of the public, regardless of the large number of potential beneficiaries.

Worked Example 1.2

A testatrix leaves “£500,000 to be applied for the relief of poverty among my poor relations.” The will contains no list of named individuals. Is the gift charitable?

Answer:

Yes. Relief of poverty is a recognised charitable head, and for poverty relief the public aspect is applied more leniently. A personal nexus (relations) does not prevent charitable status when the object is poverty relief, provided individuals are not specifically named and trustees can identify eligible persons by objective criteria of poverty.

Worked Example 1.3

An independent school charity charges high fees but has a published access strategy and awards means‑tested bursaries that open places to pupils who could not otherwise afford attendance. Does the charity meet the public benefit test?

Answer:

Generally yes, if the bursary provision and access arrangements are real and significant. Fee‑charging charities can be charitable if trustees ensure that benefits are not restricted to the wealthy and there is genuine accessibility for a sufficient section of the public. This approach reflects the reasoning in R (ISC) v Charity Commission.

Worked Example 1.4

A trust is set up “to support the spiritual life of a cloistered religious community whose members do not engage with the public.” Is this charitable?

Answer:

Not ordinarily. While advancement of religion is a recognised charitable head, the public aspect requires outward-facing benefit. A closed contemplative order with no public interaction or accessible activities typically fails the public aspect, as in Gilmour v Coats.

Worked Example 1.5

A legacy reads: “£200,000 to trustees to be applied for charitable or benevolent purposes at their discretion.” Valid charitable gift?

Answer:

No. The words “benevolent” (or “philanthropic”) extend beyond legally charitable purposes. Because trustees could choose non‑charitable benevolent purposes, the gift is not exclusively charitable and fails, as in Chichester Diocesan Fund v Simpson. Careful drafting restricted to “charitable purposes” would have been valid.

Characteristics and Advantages of Charitable Trusts

Charitable trusts possess several distinct characteristics and enjoy significant advantages compared to private trusts:

- Enforcement: They are enforced by the Attorney General (representing the Crown as parens patriae) and regulated by the Charity Commission, rather than by specific beneficiaries. The beneficiary principle does not apply in the usual way because supervision and enforcement are public responsibilities.

- Certainty of Objects: They are not required to have the same certainty of objects as private trusts. A trust for 'the relief of poverty in London' is valid, even though specific beneficiaries are not ascertainable. The focus is on purposes and on meeting public benefit.

- Perpetuity: They are exempt from the rule against inalienability that applies to non‑charitable purpose trusts, meaning they can potentially last indefinitely. Transfers between charities are also treated favourably in relation to remoteness of vesting (charitable gifts over from one charity to another are not defeated by the perpetuity rules).

- Cy‑près Doctrine: If the original charitable purpose becomes impossible or impractical, the court or Charity Commission can apply the funds cy‑près (as near as possible) to a similar charitable purpose, preventing the trust from failing completely. This may occur at the outset (initial failure) if a general charitable intention can be found, or after the charity has operated for a time (subsequent failure), when a scheme can be made without needing general charitable intention because the property has already been dedicated to charity. CA 2011 now sets out statutory grounds for cy‑près application, including changes in social or economic circumstances, redundancy of purposes, or merger/reorganisation of charities.

- Tax Advantages: Charities benefit from substantial tax reliefs, including exemptions from income tax, capital gains tax, and inheritance tax on donations and assets used for charitable purposes. These fiscal advantages, combined with the ability to continue indefinitely and apply cy‑près if needed, make charitable trusts a robust vehicle for public benefit.

Cy‑près operates to preserve charitable intent. Illustrations include:

- Initial Failure: If a specific charitable object cannot be carried out from the start, courts look for a general charitable intention (e.g., relief of the poor of a locality). If present, funds are applied cy‑près to that general intention.

- Subsequent Failure: If a valid charity later ceases to exist or its purposes become inappropriate, a scheme can redirect funds to similar charitable purposes without needing to establish general charitable intention, because the dedication to charity is already clear.

- Appropriate Considerations: Modern statutory schemes require consideration of the spirit of the gift and contemporary social and economic circumstances to ensure funds are put to effective charitable use.

Common statutory situations in which a cy‑près scheme may be appropriate include:

- the original purpose has been fulfilled or can no longer be carried out

- only part of the available property is needed for the original purpose, leaving a surplus

- property from similar charitable gifts can be applied together more effectively

- the original area or class of beneficiaries has ceased to be suitable or relevant

- changes in social or economic circumstances mean the original method has ceased to be charitable or is no longer a suitable and effective way to use the property

Exam Warning: A common error is to confuse the requirements for charitable status. Remember that all three elements – charitable purpose, public benefit, and exclusive charitable purpose – must be present. Also, be mindful that the public benefit test can apply differently depending on the specific charitable head being considered (e.g., poverty vs education). Another recurrent mistake is overlooking the effect of wording: “charitable purposes” is safe; “charitable or benevolent” is not. Finally, do not assume fee‑charging is incompatible with charitable status; trustees must show genuine public access.

Key Point Checklist

This article has covered the following key knowledge points:

- A charitable trust must be for a purpose recognised as charitable under the Charities Act 2011.

- The trust must satisfy the public benefit requirement, which has two elements: identifiable benefit and benefit to the public or a sufficient section thereof.

- The 'personal nexus' test often prevents trusts for employees or family members (except for poverty relief) from being charitable.

- Fee‑charging charities must ensure their services do not unduly exclude the poor; real access strategies (e.g., bursaries) are important.

- A charitable trust's purposes must be exclusively charitable; political purposes or significant non‑charitable objects will invalidate it, though ancillary campaigning to advance a charitable aim is permitted.

- Charitable trusts are enforced by the Attorney General/Charity Commission, are exempt from the beneficiary principle and perpetuity rules, and benefit from tax advantages and the cy‑près doctrine.

- Cy‑près may apply on initial or subsequent failure of charitable gifts, with modern statutory grounds guiding how schemes are constructed to honour the spirit of the gift and present circumstances.

Key Terms and Concepts

- Charity

- Public Benefit

- Exclusively Charitable Purpose