Learning Outcomes

This article explains the fundamental principles of double-entry bookkeeping as applied to solicitors' accounts, focusing on asset accounts like cash accounts and client ledgers. It outlines how debits and credits are used to record receipts and payments involving both business and client money. It also clarifies how entries are posted across the business and client columns of the cash account and client ledgers, how the direction of entries reflects the asset or liability change, and how to avoid common posting errors (e.g., confusing DR/CR effects on cash versus client-ledger liability). The discussion ties each posting to the permissions and requirements in the SRA Accounts Rules 2019 (including separation of client and business money, prompt banking of client funds, availability on demand, and permitted withdrawals), enabling you to interpret ledger entries, determine the correct double entries for typical transactions, and identify and rectify breaches (such as overdrawn client accounts or payment out without sufficient funds) for SQE1 assessment purposes.

SQE1 Syllabus

For SQE1, you are required to understand the practical application of accounting principles within the framework of the SRA Accounts Rules 2019. This includes correctly identifying and recording transactions involving client and business money using the double-entry system, with a focus on the following syllabus points:

- The core principles of double-entry bookkeeping.

- The distinction between debit (DR) and credit (CR) entries and their effect on different types of accounts, particularly asset accounts.

- How receipts and payments of both client and business money are recorded in the cash account and client ledgers.

- Ensuring compliance with the SRA Accounts Rules when making accounting entries.

- Separation of client money and business money (Rule 4.1), and prompt allocation of mixed receipts to the correct account (Rule 4.2).

- Client money banking requirements (Rules 2.3, 3.1–3.2), availability on demand (Rule 2.4), and prompt repayment when no longer properly needed (Rule 2.5).

- Conditions for withdrawals from the client account (Rule 5.1), authorisation/supervision (Rule 5.2), and the requirement to have sufficient funds for that specific client (Rule 5.3).

- How typical transactions appear in the business versus client columns of the cash account and client ledgers (e.g., payments of disbursements by agency or principal method, transfers to pay bills after delivery, and inter-client transfers).

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following statements about double-entry bookkeeping is correct?

- a) Every transaction requires only a single entry in one ledger.

- b) For every debit entry, there must be a corresponding debit entry in another ledger.

- c) For every credit entry, there must be a corresponding debit entry in another ledger.

- d) Debit entries always decrease asset accounts.

-

A law firm receives £5,000 from a client on account of costs. How should this receipt be recorded in the client ledger?

- a) Debit (DR) £5,000 in the business account column.

- b) Credit (CR) £5,000 in the business account column.

- c) Debit (DR) £5,000 in the client account column.

- d) Credit (CR) £5,000 in the client account column.

-

A firm pays a court fee of £150 on behalf of a client using business money, as no client funds are currently held. How is this payment recorded in the cash account?

- a) Debit (DR) £150 in the business account column.

- b) Credit (CR) £150 in the business account column.

- c) Debit (DR) £150 in the client account column.

- d) Credit (CR) £150 in the client account column.

Introduction

Understanding how financial transactions are recorded is fundamental to complying with the SRA Accounts Rules 2019. The system used by all businesses, including law firms, is double-entry bookkeeping. This system provides a structured way to record the financial activities of the firm accurately and ensures that the accounts remain balanced. For SQE1, you need to understand how this system applies specifically to the management of client and business money within a law firm, particularly concerning asset accounts like cash and client ledgers.

The SRA Accounts Rules require law firms to keep client money separate from business money (Rule 4.1), bank client money promptly into a client account held at a bank or building society in England and Wales and named to include the firm and the word “client” (Rules 3.1–3.2), ensure client money is available on demand unless otherwise agreed in writing (Rule 2.4), and repay client money promptly when there is no longer any proper reason to hold it (Rule 2.5). Withdrawals from the client account are permitted only for specified reasons (Rule 5.1) and must be authorised and supervised appropriately (Rule 5.2); crucially, withdrawals can only be made if there are sufficient funds held for that specific client or third party (Rule 5.3). In practice, these Rules map directly to how entries are posted in the cash account and client ledgers and when particular postings are permissible.

Key Term: double-entry bookkeeping

An accounting system where every transaction is recorded with two entries: a debit in one account and a corresponding credit in another account, ensuring the accounts always balance.

Double-Entry Bookkeeping Explained

The core idea behind double-entry bookkeeping is that every financial transaction has two equal and opposite effects on a firm’s accounts. To reflect this duality, every transaction is recorded with two entries: a debit (DR) in one account and a credit (CR) in another account.

In solicitors’ accounts, those two entries will sit in two places that reflect the nature of the transaction. For example:

- A receipt of money is recorded in the cash account as a debit in the relevant bank column (business or client), and the corresponding credit is posted to the appropriate column of the relevant client ledger.

- A payment out of the bank is recorded in the cash account as a credit in the relevant bank column, and the corresponding debit is posted to the appropriate column of the relevant client ledger.

These postings align with the classification of accounts: cash is an asset of the firm (even the client bank account is a firm asset in accounting terms) and therefore increases on a debit and decreases on a credit; the client ledger’s client column represents a liability owed to the client, so credits increase the amount owed and debits reduce it. Meanwhile, the client ledger’s business column is the firm’s record of the client’s debt to the firm (a receivable from the client’s point of view); debits increase that receivable, credits reduce it.

Debits and Credits

In accounting, 'debit' and 'credit' simply refer to the left and right sides of an account, respectively. Their effect depends on the type of account:

- Assets (e.g., cash, amounts owed by clients): Debits increase the account balance; Credits decrease it.

- Liabilities (e.g., amounts owed to clients, loans): Debits decrease the account balance; Credits increase it.

- Income (e.g., profit costs): Debits decrease the account balance; Credits increase it.

- Expenses (e.g., rent, wages): Debits increase the account balance; Credits decrease it.

Key Term: debit (DR)

An accounting entry typically recorded on the left side of an account. It increases asset and expense accounts and decreases liability, equity, and income accounts. Key Term: credit (CR)

An accounting entry typically recorded on the right side of an account. It increases liability, equity, and income accounts and decreases asset and expense accounts.

For SQE1 purposes, focusing on asset accounts (like cash) and liability accounts (like the client side of a client ledger, representing money owed to the client) is important.

A practical way to avoid mistakes is to anchor each posting in what is happening to the asset or liability:

- Cash account (asset): DR for receipts; CR for payments.

- Client ledger client column (liability): CR when the firm receives client money (liability increases), DR when the firm pays out client money or transfers it to business account (liability decreases).

- Client ledger business column (receivable): DR to record amounts the client owes the firm (e.g., fees and VAT when a bill is delivered, or disbursements paid from business money), CR to reduce amounts owed (e.g., when the client pays a bill).

Core Accounting Records

Law firms maintain various records. For recording day-to-day transactions involving client and business money, the two key records are the cash account (often called the cash sheet or cash book) and client ledgers.

Cash Account

The cash account records all money flowing into and out of the firm's bank accounts. Because firms must keep client money separate from their own business money (Rule 4.1, SRA Accounts Rules 2019), the cash account typically has two sets of columns: one for the business bank account and one for the client bank account.

Double-entry postings for receipts and payments of client and firm money in solicitors' accounts are allocated between cash-account and client-ledger columns.

Key Term: cash account

A ledger that records all receipts and payments of money through the firm's bank accounts, usually separated into business and client account columns. (Also referred to as cash sheet or cash book).

- Receipt of money: Always results in a DR entry in the relevant (business or client) cash account column.

- Payment of money: Always results in a CR entry in the relevant (business or client) cash account column.

As part of sound controls, client bank accounts must be reconciled regularly (at least every five weeks under the SRA Accounts Rules), and firms must ensure client money is available on demand unless a written alternative arrangement is in place (Rule 2.4). The client-account balance within the cash account should not be overdrawn; a CR balance in the client-account balance column indicates an overdrawn position and is a breach that must be rectified immediately.

Client Ledger Account

A separate ledger account must be maintained for each client, and often for each matter for that client (Rule 8.1(a), SRA Accounts Rules 2019). This ledger tracks the financial position between the firm and that specific client. Like the cash account, it usually has dual columns:

- Business account columns: Record transactions affecting the amount the client owes the firm or the firm owes the client regarding business money (e.g., billed costs, disbursements paid from business money). A DR balance means the client owes the firm; a CR balance would indicate a reduction or reversal of that debt.

- Client account columns: Record transactions involving client money held for that client (e.g., money received on account, payments made from client funds). A CR balance means the firm holds client money for the client; a DR balance indicates money has been paid out exceeding funds held, which is a breach of the Rules unless specific exceptions apply and must be remedied immediately.

Key Term: client ledger

An accounting record maintained for each individual client, showing dealings with both business money and client money related to their matters.

Maintaining accurate narratives in the details column—e.g., identifying mortgage advances, stakeholder deposits, or disbursements—helps ensure compliance and supports reconciliation and review. For instance, where firms act for both borrower and lender, receipts of mortgage advances should be clearly identified as being held on behalf of the lender until completion, even if recorded within the buyer’s client ledger.

Recording Receipts and Payments

Understanding how debits and credits affect the cash account and client ledgers is essential for recording transactions correctly.

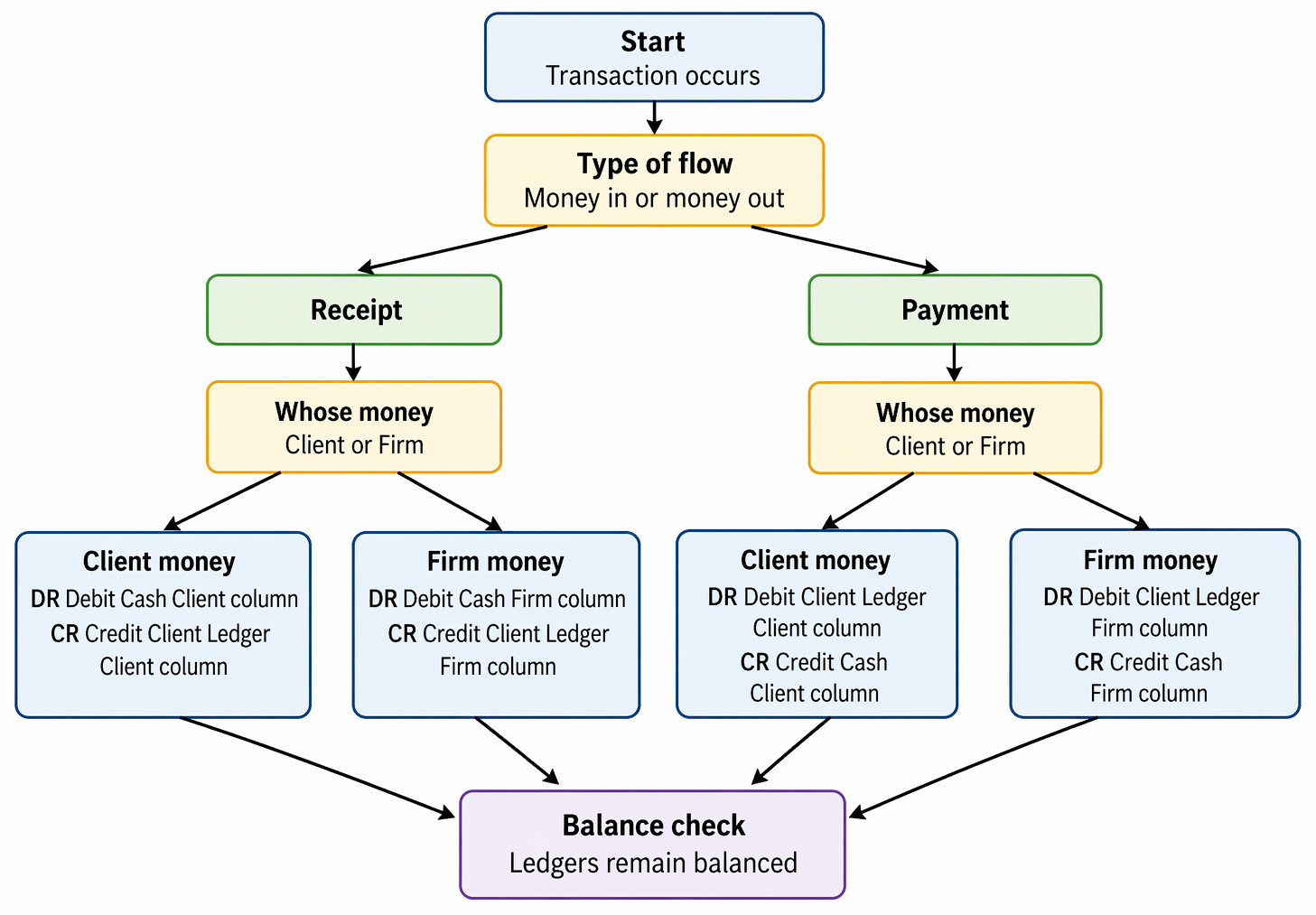

Receipts of Money

When a firm receives money, you must first identify whether it is client money or business money.

-

Receiving Client Money (e.g., money on account of costs):

- DR Cash account (Client column) - Cash asset increases.

- CR Client ledger account (Client column) - Liability to the client increases.

-

Receiving Business Money (e.g., payment of a bill after delivery):

- DR Cash account (Business column) - Cash asset increases.

- CR Client ledger account (Business column) - The client’s debt to the firm (receivable) decreases.

Worked Example 1.1

A firm receives a cheque for £500 from client Priti Patel generally on account of costs. What are the correct double entries?

Answer:

This is client money. The receipt increases the firm's cash held in the client bank account and increases the amount the firm owes to Priti Patel.

- DR Cash account (Client column) £500

- CR Priti Patel client ledger (Client column) £500

Worked Example 1.2

The firm has previously delivered a bill to Client A for £360 (£300 fees + £60 VAT). Client A pays £360 by bank transfer, which is received into the business bank account. What are the correct double entries?

Answer:

This is business money because a bill has been delivered. The receipt increases business-bank cash and reduces the client’s debt on the business side of the client ledger.

- DR Cash account (Business column) £360

- CR Client A client ledger (Business column) £360

Payments of Money

When a firm pays money out, you must decide whether to use client money (if sufficient funds are held for that specific client and the payment is permissible under Rule 5) or business money.

-

Paying Using Client Money (e.g., a disbursement paid from funds held on account):

- DR Client ledger account (Client column) - Liability to the client decreases.

- CR Cash account (Client column) - Cash asset decreases.

-

Paying Using Business Money (e.g., paying an expense for a client when no client money is held):

- DR Client ledger account (Business column) - Amount owed by the client increases (a receivable).

- CR Cash account (Business column) - Cash asset decreases.

Worked Example 1.3

The firm holds £800 for Priti Patel in the client account. The firm pays a £150 court fee (a disbursement) on her behalf using client money. What are the correct double entries?

Answer:

This is a payment of client money for a purpose for which it is held. It decreases the firm's cash held in the client bank account and decreases the amount the firm owes to Priti Patel.

- DR Priti Patel client ledger (Client column) £150

- CR Cash account (Client column) £150

Worked Example 1.4

No client funds are held. The firm pays a court fee of £150 for Client B from the business bank account. What are the correct double entries?

Answer:

Because there is no client money, the firm uses business money to pay a disbursement. This creates a debt due from the client to reimburse the firm.

- DR Client B client ledger (Business column) £150

- CR Cash account (Business column) £150

Transfers between client and business accounts after a bill

Once a bill has been delivered, money held in the client account for that client can be transferred to the business account to pay that bill (subject to Rule 5 and Rule 4.3). This movement comprises two pairs of double entries:

- The withdrawal from the client account (client-money side): DR Client ledger (Client column); CR Cash account (Client column).

- The receipt into the business account (business-money side): DR Cash account (Business column); CR Client ledger (Business column).

Worked Example 1.5

Client C has £800 on the client side of their ledger. A bill for £360 (£300 fees + £60 VAT) is delivered and then paid from funds held. What are the correct double entries across both accounts?

Answer:

First withdraw from client account; then record receipt into business account.

- Withdraw from client account: DR Client C client ledger (Client column) £360; CR Cash account (Client column) £360

- Receive into business account: DR Cash account (Business column) £360; CR Client C client ledger (Business column) £360

Mixed receipts and prompt allocation

Mixed receipts (containing both client money and business money) must be promptly allocated to the correct bank account (Rule 4.2). In practice, firms may pay the entire mixed receipt into one bank account and then promptly transfer the element belonging to the other account.

Worked Example 1.6

The firm receives £750 into the client bank account comprising £550 to settle a delivered bill and £200 on account of future costs. How should entries be made?

Answer:

Record the full receipt as client money, then promptly transfer £550 to business account to clear the bill.

- Receipt into client account: DR Cash account (Client column) £750; CR Client D client ledger (Client column) £750

- Transfer out of client account for the billed element: DR Client D client ledger (Client column) £550; CR Cash account (Client column) £550

- Receipt into business account: DR Cash account (Business column) £550; CR Client D client ledger (Business column) £550

The remaining £200 stays as client money (liability to the client) until used for permitted withdrawals or returned.

Inter-client transfers

Sometimes funds must be reallocated within the client account between matters or between clients (e.g., from an estate ledger to a beneficiary’s ledger). As the money remains within the client bank account, no cash-account entry is made; instead, an equal and opposite pair of entries are recorded on the client ledgers.

Worked Example 1.7

The firm holds £600 on the client ledger for Client E’s sale proceeds. Client E instructs the firm to move £600 to their separate will-drafting matter as money on account. What are the correct double entries?

Answer:

This is an inter-client transfer within the client account. No cash-account entry is made.

- DR Client E sale matter ledger (Client column) £600

- CR Client E will-drafting matter ledger (Client column) £600

Dishonoured cheques and breaches

A common breach arises if a payment is made from the client account before an incoming cheque clears and the cheque later bounces, leaving insufficient funds held for that client. If client money has been used without sufficient funds (contrary to Rule 5.3), it must be rectified immediately by transferring business money into the client account to restore the balance and eliminate any overdrawn client position.

Worked Example 1.8

Client F sends a £2,000 cheque on account. The firm pays a £500 disbursement from the client account the next day. The cheque is then dishonoured. What must the firm do, and what entries are needed to rectify the breach?

Answer:

The firm must immediately transfer business money into the client account to cover the shortfall until cleared funds are available.

- DR Cash account (Client column) £500

- CR Cash account (Business column) £500

The firm should then seek replacement funds from the client and reverse any temporary rectification transfer once cleared client money is received.

Stakeholder deposits

When holding a buyer’s deposit as stakeholder on a sale, it is held jointly for buyer and seller until completion. The deposit is recorded as client money, but must be clearly identified as stakeholder funds. On completion, it is transferred to the seller’s client ledger (an inter-client transfer).

Worked Example 1.9

A £25,000 deposit is received on exchange to be held as stakeholder for Seller G and Buyer H. How should it be recorded, and what happens on completion?

Answer:

On exchange, record stakeholder receipt as client money; on completion, transfer to the seller’s client ledger.

- On exchange: DR Cash account (Client column) £25,000; CR Stakeholder ledger (Client column) £25,000

- On completion (inter-client transfer, no cash-account entry): DR Stakeholder ledger (Client column) £25,000; CR Seller G client ledger (Client column) £25,000

Mortgage advances

If acting for both borrower and lender on a purchase, mortgage advances are client money held on behalf of the lender until completion. Record the receipt as client money, with clear identification in the ledger narrative.

Worked Example 1.10

A building society sends £100,000 as a mortgage advance for Buyer J’s purchase. What are the entries on receipt?

Answer:

The mortgage advance is client money; record it in the client bank columns and identify the lender and nature of funds in the details column.

- DR Cash account (Client column) £100,000

- CR Buyer J client ledger (Client column) £100,000

Exam Warning: A common error is confusing the effect of debits and credits on different account types. Remember: for asset accounts like Cash, DR increases and CR decreases. For liability accounts like the client ledger (client column), CR increases (more money held for client) and DR decreases (less money held for client). Mixing these up leads to incorrect recording and potential breaches of the SRA Accounts Rules. Additional pitfalls to avoid:

- Posting only one side of a double entry. Every transaction must have equal and opposite entries.

- Using the wrong bank column. Receipts into the client bank account must not be recorded in the business bank column, and vice versa.

- Paying out of client account when there are insufficient funds held for that specific client (Rule 5.3). Always check the client ledger client-column balance first.

- Failing to promptly allocate mixed receipts to the correct bank account (Rule 4.2) and failing to repay client money promptly when no longer properly needed (Rule 2.5).

- Using the client account to provide banking facilities (Rule 3.3). Every payment into or out of the client account must relate to regulated legal services and a proper purpose.

Revision Tip: Think of the client column on the client ledger like your personal bank statement from the firm's point of view: a CR balance means the firm owes the client money (funds available), while a DR balance means the client owes the firm money (or money has been paid out). The cash account is like the firm's own bank statement: DR means money came in, CR means money went out. Before posting any entry, ask three quick questions:

- Which bank is involved (client or business)?

- Is the movement a receipt (cash DR) or a payment (cash CR)?

- Which side of the client ledger is impacted (client column—liability; business column—receivable), and is it a DR or a CR there?

Key Point Checklist

This article has covered the following key knowledge points:

- Double-entry bookkeeping ensures every transaction has equal and opposite debit (DR) and credit (CR) entries.

- Debits increase asset accounts (like cash) and decrease liability accounts (like money owed to clients).

- Credits decrease asset accounts and increase liability accounts.

- The cash account records money movement in the firm's bank accounts (business and client). Receipts are DR; payments are CR.

- The client ledger tracks the financial position with each client, separated into business and client money columns.

- Receipts of client money: DR Cash (client), CR Client Ledger (client).

- Receipts of business money (payment of a delivered bill): DR Cash (business), CR Client Ledger (business).

- Payments using client money: DR Client Ledger (client), CR Cash (client).

- Payments using business money (e.g., paying a disbursement when no client funds are held): DR Client Ledger (business), CR Cash (business).

- Transfers from client to business account after delivering a bill involve two pairs of entries (withdrawal from client account, receipt into business account).

- Inter-client transfers are recorded on client ledgers only; no cash-account entry is made because money remains within the client bank account.

- Mixed receipts must be promptly allocated and transferred to the correct account(s) in accordance with Rule 4.2.

- Accurate recording, availability on demand, and proper withdrawals are essential for compliance with the SRA Accounts Rules 2019.

Key Terms and Concepts

- double-entry bookkeeping

- debit (DR)

- credit (CR)

- cash account

- client ledger