Learning Outcomes

This article outlines the equitable remedy of tracing, explaining how beneficiaries can identify and follow trust property that has been misapplied, substituted or mixed with other assets in breach of trust. It sets out the preconditions for tracing in equity, the need for a fiduciary relationship and an equitable proprietary interest, and the distinction between following at law and tracing in equity. It details the rules for tracing into clean substitutions and mixed funds, including mixed bank accounts, and demonstrates how presumptions such as Re Hallett and Re Oatway operate alongside the lowest intermediate balance rule. It also reviews tracing where multiple innocent contributors are involved, the use of pari passu and the possible displacement of Clayton’s Case. The article analyzes key limitations on tracing, including dissipation, bona fide purchaser defences, change of position, inequitable results and laches, and explains the beneficiary’s election between a constructive trust and an equitable lien. It finally applies these principles to SQE1-style problem questions, strengthening your ability to select the most appropriate proprietary or personal remedy in FLK2 assessments.

SQE1 Syllabus

For SQE1, you are required to understand the practical application of equitable tracing as a remedy for breach of trust, including identifying the circumstances in which tracing is available, the necessary preconditions, and the various rules and limitations that apply, particularly in relation to mixed funds, with a focus on the following syllabus points:

- The distinction between common law and equitable tracing, focusing on the requirements for tracing in equity.

- The requirement for a fiduciary relationship and an equitable proprietary interest, and the debate about these requirements.

- The process of following property and tracing value into substitute assets and mixed funds (including the claimant’s election between remedies).

- The specific rules applicable to tracing into mixed bank accounts (Re Hallett, Re Oatway, Roscoe v Winder, Clayton’s Case) and when they may be displaced (e.g., by pari passu).

- Limitations on tracing, including dissipation, the defence of bona fide purchaser for value without notice, change of position, and laches.

- How “lowest intermediate balance” constrains bank-account claims, and the potential for “backward tracing” where there is a coordinated scheme (Federal Republic of Brazil v Durant International).

- The relationship between tracing and other equitable responses, including constructive trusts, equitable liens, and personal claims such as knowing receipt and Re Diplock claims against volunteers.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is a prerequisite for tracing in equity?

- a) A contractual relationship between the claimant and defendant.

- b) The property must remain in its original form.

- c) The existence of a fiduciary relationship.

- d) The claimant must have suffered a quantifiable financial loss.

-

A trustee mixes £10,000 of trust money with £5,000 of their own money in their personal bank account. They then withdraw £5,000 and spend it on a holiday. According to the rule in Re Hallett's Estate, which money is presumed to have been spent?

- a) The trust money.

- b) The trustee's own money.

- c) A proportionate mix of both.

- d) The money deposited last.

-

Against which party is an equitable tracing claim least likely to succeed?

- a) The wrongdoing trustee.

- b) An innocent volunteer who received the property as a gift.

- c) A bona fide purchaser for value without notice.

- d) A person who dishonestly assisted the breach of trust but did not receive the property.

Introduction

When trust property is misapplied by a trustee in breach of trust, beneficiaries may seek remedies to recover the loss. While a personal claim against the trustee for compensation is available, it may be ineffective if the trustee is insolvent. Equity provides a more powerful set of remedies through the process of tracing, allowing beneficiaries to follow the trust property or its proceeds into the hands of the trustee or even third parties. This article explores the availability and limitations of tracing in equity.

Key Term: Tracing

A process by which a claimant demonstrates what has happened to their property (or its value), identifies its proceeds or substitutes, and justifies a claim that the proceeds or substitute can properly be regarded as representing their property. Tracing is not a remedy itself but a preliminary step to establish a proprietary claim. Key Term: Following

The process of locating the very same asset as it moves from hand to hand. By contrast, tracing identifies a new asset that represents the value of the old. Key Term: Election

The claimant’s choice between alternative proprietary remedies (typically a constructive trust or an equitable lien) once tracing has identified a substitute asset.

Tracing in equity differs significantly from tracing at common law. Common law tracing requires the property to remain identifiable and unmixed. Equity, however, can trace property even when it has been mixed with other property or has changed form, provided certain conditions are met. Equitable tracing is closely linked to equitable proprietary rights and is frequently invoked alongside claims for breach of trust, knowing receipt, and other proprietary or personal claims.

Test Tip: In SQE-style questions on Availability and limitations of tracing in equity, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Availability of Tracing in Equity

To trace property in equity, two main prerequisites must usually be satisfied:

-

A Fiduciary Relationship: Historically, equity required a fiduciary relationship (e.g., trustee-beneficiary) to exist between the claimant and the person who misapplied the property. This requirement has been questioned in modern commentary, but in the SQE1 context it remains a conventional jurisdictional basis. The fiduciary link is commonly present in trust cases and is also recognised in contexts such as bribes held on constructive trust and certain mistaken transfers once conscience is engaged.

-

An Equitable Proprietary Interest: The claimant must have a pre-existing equitable proprietary interest in the property being traced. A beneficiary under a trust clearly satisfies this requirement. Where the claimant holds only a personal right, tracing will not generally be available.

Key Term: Fiduciary Relationship

A relationship where one party (the fiduciary, e.g., a trustee) owes special duties of loyalty, trust, and confidence to another party (the principal or beneficiary) and must act in that party's best interests. Key Term: Equitable Proprietary Interest

An interest in property recognised and enforced by equity, such as the interest of a beneficiary under a trust. It allows the interest holder to assert rights against the property itself. Key Term: Bona fide purchaser for value without notice

A person who acquires legal title to property for value, in good faith, without actual, constructive, or imputed notice of any prior equitable interest. Equity will not allow a prior equitable claimant to recover the property from this purchaser.

Two additional equitable constraints often arise: tracing must not lead to an inequitable result (especially against an innocent volunteer) and it must be pursued with due expedition (delay may trigger laches). These are considered under “Limitations.”

Once these prerequisites are met, tracing can proceed, allowing the claimant to follow the trust property through various substitutions and mixtures and then elect the most advantageous proprietary response.

The Process of Tracing in Equity

Equitable tracing allows beneficiaries to follow trust property even when it changes form or becomes mixed with other assets. The specific rules applied depend on how the property has been dealt with.

Key Term: Equitable Lien

A non-possessory equitable charge over property imposed to secure a monetary claim. It gives priority over unsecured creditors and may lead to an order for sale to satisfy the debt. Key Term: Constructive Trust (in tracing context)

An equitable mechanism by which the holder of a substitute asset is required to hold it (or part of it) for the claimant. It enables the claimant to capture any increase in value attributable to the asset.

Clean Substitution

If the trustee uses trust property exclusively to acquire a new asset (a “clean substitution”), the beneficiaries can choose either:

- To take the substitute property itself by way of constructive trust (advantageous if the asset has increased in value).

- To take a charge (an equitable lien) over the substitute property for the amount of trust money used (advantageous if the asset has decreased in value).

The modern approach (endorsed in leading authority) recognises the beneficiary’s election to choose the proprietary response that best serves their interests once the substitute is identified. If a constructive trust is chosen, the claimant will share in increases and decreases in value proportionately. If an equitable lien is chosen, recovery is capped at the amount misapplied (plus any appropriate interest), without exposure to subsequent fluctuations in value.

Tracing into Mixed Funds

Tracing becomes more complex when trust property is mixed with other money, typically the trustee’s own funds or funds from another trust or a volunteer.

Mixing Trust Funds with Trustee's Own Funds

If a trustee mixes trust funds with their own money in an asset or a bank account, equity applies protective presumptions against the wrongdoer, but allows claimants to displace those presumptions where fairness demands.

Equitable tracing claims are presented across clean substitutions, mixed funds and mixed accounts, including priorities and presumptions applicable to withdrawals.

-

Purchasing Assets with Mixed Funds: Where the trustee uses a mixed fund to purchase an asset, the beneficiaries can elect:

- A proportionate share (via constructive trust) in the asset, thereby taking a slice of any increase in value.

- An equitable lien for the amount of trust money contributed, useful where the asset has fallen in value. The claimant’s choice will be respected to protect their position.

-

Withdrawals from a Mixed Bank Account:

- The Rule in Re Hallett's Estate (1880): The trustee is presumed to spend their own money first. This presumption allows the beneficiaries to assert that what remains in the account (or what has been invested) is trust money, insofar as needed to protect the beneficiaries.

- The Rule in Re Oatway (1903): Where applying Re Hallett would be unfair (for example, if the trustee’s early withdrawal was invested in a recoverable asset and later withdrawals were dissipated), the beneficiaries may assert a first claim on the asset purchased, as if trust money had been used to acquire it. Equity presumes against the wrongdoer and allows the beneficiary to take the most favourable route.

- Lowest Intermediate Balance (Roscoe v Winder (1915)): The claimant’s maximum claim against a mixed bank account is limited to the lowest balance in the account between the time the trust money was paid in and the time of the claim, ignoring any later “replenishment.” Later deposits by the trustee are not presumed to restore the trust funds, unless there is clear evidence of an intention to do so for the trust (rare in practice). If the account is overdrawn, payments into it are typically treated as meeting the overdraft (dissipation), leaving nothing to trace unless a coordinated scheme exception applies.

- Backward Tracing (Limited): Traditionally, a claimant could not trace into an asset acquired before trust money was paid in (for example, where a loan financed the asset and later trust money repaid the loan). However, where there is a close and deliberate interconnection between the acquisition and the later misuse of trust funds—forming a coordinated scheme—equity may allow “backward” tracing to the acquired asset. The Privy Council in Federal Republic of Brazil v Durant International Corporation (2015) recognised that where steps are part of a seamless, orchestrated arrangement, the two can be linked for tracing purposes.

Key Term: Lowest Intermediate Balance

The maximum sum recoverable out of a mixed bank account is capped at the lowest balance reached between the deposit of trust funds and the date of the claim, ignoring later deposits unless clearly earmarked to restore the trust. Key Term: Backward Tracing

Tracing into an asset acquired prior to the misapplied funds entering the relevant account. Allowed only in exceptional circumstances where a coordinated scheme connects the transactions.

Mixing Funds from Two Trusts or Trust and Innocent Volunteer

If a trustee mixes funds from two different trusts, or mixes trust funds with money belonging to an innocent volunteer (a recipient for no value and without notice), the rules aim at fairness between innocent contributors.

- Purchasing Assets with Mixed Innocent Funds: The contributors share proportionately (pari passu) according to the value they injected. They share any gain or loss rateably.

- Withdrawals from a Mixed Innocent Bank Account:

- Clayton’s Case (1816): The default FIFO rule applies (“first in, first out”), so the earliest deposit is treated as the source of the earliest withdrawal.

- Pari Passu and Other Pragmatic Methods: FIFO can be artificial and unjust in many modern contexts (e.g., pooled investment schemes). Courts often displace Clayton’s Case and prefer a pari passu distribution of remaining funds (or a rolling charge) that better reflects fairness among many small claimants (Barlow Clowes International v Vaughan (1992)).

Key Term: Pari passu

A method of distribution where all contributors share losses or assets proportionately to their contributions. Key Term: FIFO (Clayton’s Case)

A presumption that withdrawals from a mixed bank account are attributed to the earliest deposits first. Now frequently displaced where unsuitable.

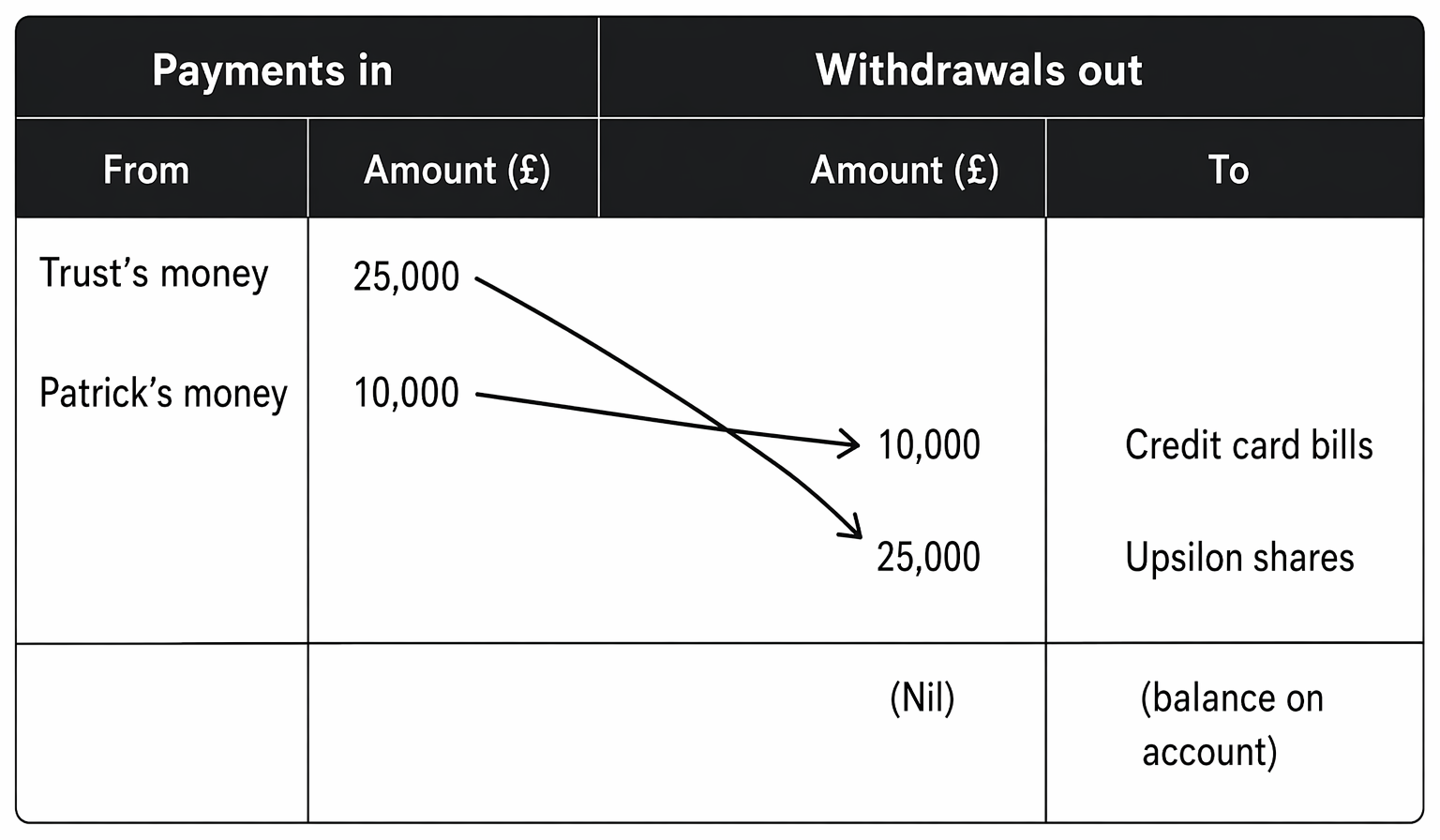

Worked Example 1.1

Tariq, a trustee, misappropriates £20,000 from the Smith Trust. He pays this into his personal bank account, which already contains £10,000 of his own money. He then withdraws £15,000 to buy shares in XYZ plc. Later, he withdraws the remaining £15,000 and spends it on a luxury holiday (dissipation). The shares are now worth £18,000. What proprietary claim can the beneficiaries of the Smith Trust make?

Answer:

The trustee mixed trust funds (£20,000) with his own (£10,000). Applying the rule in Re Hallett’s Estate, the trustee is presumed to spend his own money first. However, this would mean the £15,000 shares were bought partly with personal money and the dissipation was largely at the trust’s expense. Equity does not allow the trustee to benefit from this. Under Re Oatway, the beneficiaries may treat the shares as representing the trust money and claim them by constructive trust (worth £18,000), reflecting the protective presumption against the wrongdoer. Alternatively, they could elect an equitable lien for their misapplied £20,000 against the shares (useful if the shares had fallen), but here election of the constructive trust is more advantageous.

Worked Example 1.2

A trustee mistakenly pays £5,000 of trust money to Fiona, an innocent volunteer who believes it is a legacy she was expecting. Fiona uses the £5,000, along with £1,000 of her own savings, to install a new bathroom in her house. The installation does not increase the market value of her house. Can the beneficiaries trace the £5,000?

Answer:

Fiona is an innocent volunteer. The money was used on improvements that did not increase value and are inseparable from her property. Forcing a sale would likely be inequitable, and the defence akin to Re Diplock (change of position) is engaged. Tracing is unlikely to succeed into the bathroom works. The beneficiaries may pursue a personal claim against the trustee (and, subsidiarily, the limited Re Diplock-style personal claim against Fiona if appropriate and other remedies are exhausted).

Worked Example 1.3

A trustee pays £30,000 of trust money into a personal account with a nil balance. Over time, the balance fluctuates: it drops to £5,000, then later rises to £25,000 due to the trustee’s own deposits. The trustee then withdraws £10,000 to buy a car now worth £12,000. How much can the beneficiaries claim?

Answer:

Under the lowest intermediate balance rule, the maximum claim against the account is capped at £5,000 (the lowest point). Later deposits are not presumed to restore trust money. However, the £10,000 car purchase was made after the balance rose. Applying the mixed-purchase principles, the trust can assert a proportionate interest in the car to the extent any surviving traceable funds are used. On these facts, the strict cap implies only £5,000 of the account can be treated as trust money. The beneficiaries may elect an equitable lien for £5,000 over the car or claim a constructive trust proportion to that contribution (which would also capture a proportion of the increase to £12,000). If they elect a lien, recovery is £5,000 plus appropriate interest; if they elect a constructive trust, they would share the uplift pro rata.

Worked Example 1.4

Two trusts are affected by the same dishonest trustee. He deposits £40,000 from Trust A into his personal account, then £60,000 from Trust B. He spends £50,000 on a commercial van (now worth £30,000) and the remainder is dissipated. How should the van be apportioned between A and B?

Answer:

Between two innocent contributors, the court can apply Clayton’s Case (FIFO), but it is often displaced. A proportionate (pari passu) division is fair: Trust A contributed 40% and Trust B 60% to the mixed pool; they share the asset’s current value rateably. Trust A would take 40% of £30,000 (£12,000) and Trust B 60% (£18,000). The court is likely to prefer a pari passu approach to avoid the arbitrary effects of FIFO.

Worked Example 1.5

A fraudster purchases an apartment for £500,000 using a short-term loan, planning to clear the loan days later with trust funds misapplied from a company. The trust money arrives after completion and is immediately used to discharge the loan. Can the beneficiaries trace into the apartment?

Answer:

This scenario raises backward tracing. If the evidence shows a coordinated scheme linking the acquisition and the later misuse of trust funds (as in Brazil v Durant), equity may allow tracing into the apartment, treating the loan repayment with trust funds as part of a single orchestrated transaction. Provided a sufficiently close connection is proved, the beneficiaries can claim a proprietary interest by constructive trust or an equitable lien over the apartment.

Limitations on Tracing in Equity

The right to trace in equity, while powerful, is not absolute and can be lost or restricted in several circumstances.

Dissipation

If the trust property or its proceeds have been dissipated without leaving any substitute asset, tracing is impossible. Examples include money spent on general living expenses, payment of unsecured debts, services already consumed, or assets that have been destroyed.

Key Term: Dissipation

The spending or destruction of property such that it leaves no traceable product or substitute asset.

Bona Fide Purchaser for Value Without Notice

Tracing cannot be pursued against a person who acquires legal title to the property for valuable consideration in good faith and without notice of the pre-existing equitable interest. Often called “equity’s darling,” such a purchaser takes free of the prior equitable claim, thereby extinguishing the claimant’s proprietary route.

Inequitable Result and Change of Position

Tracing is an equitable process, and the court will not permit it where it would lead to an inequitable result, particularly against innocent volunteers. The Re Diplock line of authority recognises that where trust funds were paid by mistake and received by a volunteer, a proprietary claim may be barred if tracing would unfairly prejudice that volunteer (e.g., where the money was spent improving land without increasing its value, or where restitution would be oppressive). In parallel, the modern defence of change of position (developed in unjust enrichment) protects an innocent recipient who, relying on the receipt, changed their position in good faith so that repayment would be unjust.

Key Term: Change of position

A defence available to an innocent recipient who has, in good faith, altered their position in reliance on the receipt, making full restitution inequitable.

Doctrine of Laches and Delay

Equitable relief is discretionary. Undue delay may bar or limit a tracing claim if it would be unfair to the defendant to permit relief (e.g., where delay has prejudiced the defendant’s ability to resist or to mitigate the claim). Where an equitable proprietary claim is pursued, there is no fixed limitation period as such; instead, laches and acquiescence principles apply. However, personal claims for breach of trust may be subject to statutory limitation rules, with important exceptions for fraud and the recovery of trust property from a trustee.

Worked Example 1.6

Trust money is mistakenly paid to Omar, an innocent volunteer, who uses it to settle non-refundable university tuition instalments for his child that he would not otherwise have incurred. The benefits of the tuition have been received. Can the trust trace and recover?

Answer:

No identifiable substitute asset exists; the payments have been consumed and there is nothing to trace. Further, Omar would likely succeed with a change of position defence to any personal claim because he irreversibly altered his position in good faith. The beneficiaries must pursue the trustee personally for the loss.

Election Between Remedies and Practical Strategy

Having located a substitute asset, the claimant must elect an appropriate proprietary remedy:

- A constructive trust is attractive where the asset has increased in value, as it gives a proportionate share and captures uplift.

- An equitable lien is preferable where the asset has fallen in value or where the claimant wishes to prioritise a fixed monetary recovery secured against the asset.

The election is made in light of practicality, marketability of the asset, competing creditors, and any risks of further fluctuation. Election is not normally required at the outset of litigation; courts allow claimants to frame their remedies as the facts emerge and to avoid double recovery.

Revision Tip: When faced with a tracing problem, always identify: 1. Is there a fiduciary relationship and equitable interest? 2. Has the property been mixed or substituted? 3. Who currently holds the property or its proceeds (trustee, volunteer, purchaser)? 4. Apply the correct tracing rules based on the parties involved. 5. Consider if any defences (dissipation, bona fide purchaser, change of position, inequitable result, laches) apply. 6. Decide the most advantageous election between constructive trust and equitable lien.

Key Point Checklist

This article has covered the following key knowledge points:

- Tracing in equity is a process for identifying and claiming substitute assets representing misapplied trust property; it is distinct from following the original asset.

- Prerequisites typically include a fiduciary relationship and an equitable proprietary interest held by the claimant.

- Once a substitute asset is identified, the claimant may elect to pursue a constructive trust (capturing value increases) or an equitable lien (securing repayment).

- Tracing is possible into substitute assets and mixed funds. Equity maintains protective presumptions against wrongdoers (Re Hallett) and allows displacement where fairness requires (Re Oatway).

- Specific rules apply to mixed bank accounts, including the lowest intermediate balance cap (Roscoe v Winder). FIFO (Clayton’s Case) can be displaced by pari passu where appropriate (Barlow Clowes).

- Backward tracing may be permitted if transactions are part of a coordinated scheme (Brazil v Durant).

- Tracing is defeated by dissipation of the property or transfer to a bona fide purchaser for value without notice.

- Tracing against innocent volunteers is constrained by equitable principles where restitution would be inequitable; change of position can operate as a defence.

- Delay may bar equitable relief under the doctrine of laches, though personal claims for breach of trust are subject to separate limitation rules with key exceptions.

- Tracing interacts with broader equitable responses, including knowing receipt (recipient liability), dishonest assistance (accessory liability), and Re Diplock-style personal claims against volunteers.

Key Terms and Concepts

- Tracing

- Following

- Fiduciary Relationship

- Equitable Proprietary Interest

- Election

- Equitable Lien

- Constructive Trust (in tracing context)

- Lowest Intermediate Balance

- Backward Tracing

- Bona fide purchaser for value without notice

- Change of position

- Dissipation

- Pari passu

- FIFO (Clayton’s Case)