Learning Outcomes

This article outlines funding of the initial Inheritance Tax (IHT) payment before a grant of representation and related legal and practical considerations, including:

- HMRC requirements for IHT payment before a grant and the portion payable at that stage, enabling identification of which liabilities must be settled immediately and which can be deferred

- The Direct Payment Scheme (DPS): forms, scope, limitations, and distinction from National Savings direct payments and small payment releases, with emphasis on how exam questions test eligibility and procedural sequencing

- Practical funding alternatives: beneficiary and third‑party loans, life insurance proceeds, and assets realisable without a grant, including the impact of interest, security, and undertakings on estate residue

- The instalment option for qualifying assets: amount due before the grant, interest implications, and effect of early asset sale, together with recognition of which assets qualify and how elections are made in IHT400

- Procedural steps and timing: forms IHT400, IHT421, IHT422, IHT423, and the impact of excepted estates on funding needs, focusing on the interaction between HMRC receipts and issue of the grant

- Risks and consequences for personal representatives (PRs): interest accrual, undertakings, and personal liability for premature distributions, equipping candidates to spot when PRs have breached their duties in problem-style MCQs

- Application of these rules to typical SQE1-style scenarios involving cash‑poor estates, joint property, and business or agricultural assets

SQE1 Syllabus

For SQE1, you are required to understand the legal and practical framework for funding the initial Inheritance Tax (IHT) payment before a grant of representation is issued, with a focus on the following syllabus points:

- statutory requirement that IHT must be paid (in whole or part) before a grant is issued

- mechanisms to fund payment: Direct Payment Scheme, national savings and small payments, loans, insurance proceeds, realisation of accessible assets, and instalments

- limitations and consequences of each method, including interest, timing, undertakings, and personal liability

- interaction between IHT funding, HMRC receipt procedures, and the grant of representation process

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Why is it necessary to pay Inheritance Tax before a grant of representation is issued?

- Name two methods by which personal representatives can fund the initial IHT payment if the estate is cash-poor.

- What is the Direct Payment Scheme and what are its main limitations?

- In what circumstances can IHT be paid by instalments, and what are the implications for the grant of representation?

Introduction

When a person dies leaving an estate liable to Inheritance Tax (IHT), the personal representatives (PRs) must pay the tax due before the grant of representation (probate or letters of administration) is issued. This can create a practical problem: PRs often need access to estate assets to pay the tax, but cannot access those assets until the grant is obtained. This article explains the main legal and practical methods available to fund the initial IHT payment, the statutory framework, and the implications for estate administration.

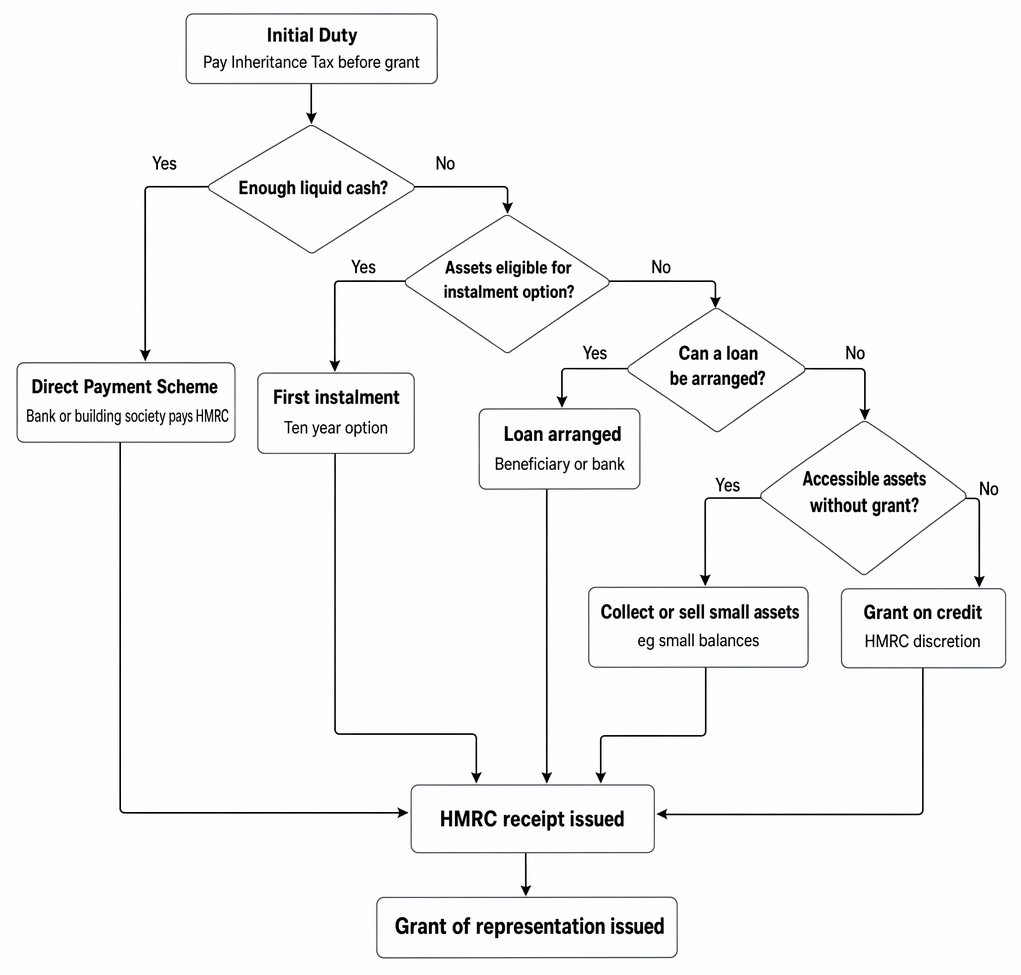

Routes for funding initial IHT before a grant of representation, culminating in HMRC receipt and issue of the grant.

IHT on transfers on death is generally due six months after the end of the month in which the death occurred. Interest accrues after that date on unpaid amounts. However, in order for the Probate Registry to issue the grant, HMRC must confirm that the tax due at that stage has been paid. For estates where IHT is payable, this means paying the full IHT attributable to non‑instalment property and, if the instalment option is used for qualifying assets, paying the first annual instalment attributable to those assets. Where the estate is excepted and no IHT is due, this funding issue does not arise.

Key Term: grant of representation

The legal document (probate or letters of administration) confirming the authority of the personal representatives to administer the estate.

The Statutory Requirement: IHT Payment Before Grant

Under the Inheritance Tax Act 1984, IHT on the death estate is generally due six months after the end of the month in which the deceased died. However, HM Revenue & Customs (HMRC) will not issue the necessary receipt for the grant of representation until the tax due on non-instalment option property has been paid. This is a strict requirement: without evidence of payment, the Probate Registry will not issue the grant, and the PRs cannot collect or sell most estate assets.

The practical mechanism is HMRC’s probate summary (IHT421) being sent to the Probate Registry after HMRC accepts the account and that the appropriate amount of tax has been paid. PRs obtain an IHT reference (IHT422) to make payments, file the full account (usually IHT400 with schedules), and where using bank/building society releases complete form IHT423. In excepted estates (where no IHT is payable), PRs complete the simplified route and the funding issue is avoided.

The amount payable before the grant:

- full IHT attributable to non‑instalment property

- the first annual instalment on property for which the PRs have validly elected to pay by instalments (for qualifying assets only)

Key Term: Direct Payment Scheme

A scheme allowing banks and building societies to transfer funds directly from the deceased’s account to HMRC to pay IHT before the grant is issued.

Practical Methods for Funding Initial IHT Payment

PRs must find a way to pay IHT before they have full access to the estate. The main methods are:

1. Direct Payment Scheme (DPS)

The Direct Payment Scheme is an arrangement between HMRC and most UK banks and building societies. Under the DPS, PRs can instruct the deceased’s bank or building society to pay IHT directly from the deceased’s account to HMRC before the grant is issued.

- PRs obtain an HMRC reference (IHT422) and submit the IHT400 (with schedules) to HMRC, together with the IHT421 probate summary.

- PRs complete form IHT423 for each UK bank/building society account from which payment is requested and send it to the institution.

- The bank/building society pays the approved amount directly to HMRC under the DPS.

- HMRC issues a receipt to the Probate Registry (via IHT421), enabling the grant to be issued.

Additional practical points:

- The DPS is voluntary; not all institutions participate. Overseas banks with no UK presence generally do not.

- Joint accounts pass by survivorship; the institution will usually not release joint monies directly to PRs, but the surviving holder may choose to lend funds to the PRs (see loans).

- Funds may also be released via DPS for funeral expenses in analogous fashion.

Limitations:

- Only funds held in UK banks/building societies participating in the scheme can be used.

- Each account requires its own IHT423; processing can be slow.

- If the estate is cash‑poor or the deceased’s accounts are insufficient, other methods are needed.

National Savings and certain government investments can also be used to pay IHT direct to HMRC in appropriate cases. Where relevant, PRs can request payment from National Savings products (for example, National Savings Bank accounts, Certificates, or registered government stock) be made direct to HMRC for IHT due.

2. Using Liquid Assets

If the estate contains sufficient cash in accessible accounts, PRs can use these funds to pay IHT directly. However, most institutions will not release funds to the PRs without a grant, except under the DPS. In limited circumstances, some small balances may be released without a grant under the Administration of Estates (Small Payments) Act 1965, but:

- the limit is low per asset (commonly up to £5,000)

- releases are discretionary

- the approach varies between institutions

Small payments can help meet part of the initial liability but are rarely sufficient in larger taxable estates.

3. Loans from Beneficiaries or Third Parties

If the estate lacks sufficient liquid assets, PRs may borrow funds to pay IHT:

- Beneficiaries who have received assets outside the estate (e.g., joint accounts passing by survivorship, life insurance written in trust) may lend money to the PRs.

- Alternatively, PRs may obtain a loan from a bank or building society, usually secured against estate assets. The loan is repaid from the estate once the grant is issued and assets are realised.

Professional practice points:

- Lenders commonly require a “first proceeds” undertaking, i.e., repayment from the first liquid assets realised post‑grant.

- If the PRs’ solicitor gives an undertaking, it should be carefully framed to limit it to funds received into the solicitor’s client account for the estate and not be a personal guarantee.

- Interest and arrangement fees are payable and reduce the net residue. In practice, PRs should aim to repay loans as early as possible.

- Interest paid on a separate loan account for IHT on personalty vesting in the PRs may be deductible for estate income tax calculations during administration, typically for up to one year.

Key Term: personal representatives

Executors or administrators responsible for collecting in the estate, paying debts and liabilities, and distributing assets to beneficiaries.

4. Life Insurance Policies Written in Trust

If the deceased had a life insurance policy written in trust, the proceeds are paid directly to the trust or nominated beneficiaries and do not form part of the estate for IHT. These funds are available immediately and can be used to pay IHT.

Where the policy proceeds are payable to the estate (rather than held in trust), some insurers may be willing to release funds directly to HMRC to settle IHT, similar in practice to DPS releases.

5. Realising Assets Not Requiring a Grant

Some assets can be accessed or realised without a grant, such as:

- National Savings accounts (subject to the specific product rules and limits)

- Certain chattels (personal possessions) that can be sold without formal proof of title

- Small balances in building societies (subject to their discretion)

Care is needed, as most securities (including quoted shares) will usually require the grant to transfer or sell. While occasional practice exceptions exist, PRs should generally expect brokers and registrars to ask for a grant.

6. Payment by Instalments

In certain cases, IHT on specific assets can be paid in up to ten annual instalments. Only the first instalment is due before the grant is issued; the remainder is paid annually, with interest, or in full if the asset is sold. The instalment option is designed for assets that are not readily realisable without undue delay or disadvantage, including:

- land (including agricultural land)

- a business or interest in a partnership

- shares/securities giving control of a company (and some unquoted shareholdings)

The election is made in the IHT400 account. Practical effects:

- Only the first instalment of the IHT attributable to the qualifying asset is payable before the grant; the IHT on non‑instalment property must be paid in full.

- Interest accrues on unpaid instalments after the due date (six months after the end of the month of death), at HMRC’s prevailing rates.

- If the asset is sold or otherwise disposed of before all instalments have been paid, the outstanding IHT balance becomes immediately payable.

Key Term: instalment option

The statutory right to pay IHT on certain assets (e.g., land, business interests, controlling shareholdings, some unquoted shares) in up to ten annual instalments, with only the first instalment due before the grant is issued.

- PRs must indicate on the IHT400 that they wish to pay by instalments and identify the qualifying assets.

- The Probate Registry will issue the grant once the first instalment is paid and HMRC has issued the receipt.

Worked Example 1.1

The deceased’s estate includes a house worth £600,000 and cash of £50,000. The total IHT due is £100,000. The PRs wish to pay IHT by instalments on the house.

Question: How much IHT must be paid before the grant is issued? Answer:

The PRs must pay IHT in full on the cash (£50,000), plus the first instalment (10%) on the house. If £60,000 of the £100,000 IHT is attributable to the house, the first instalment will be £6,000. The remaining IHT on the house can be paid in nine further annual instalments, with interest.

7. Exceptional Cases: Grant on Credit

In rare cases, if PRs can show it is impossible to pay IHT in advance (e.g., all assets are illiquid and no loan is available), HMRC may allow the grant to be issued on credit. This is exceptional and requires strong evidence. The estate will still be liable for IHT and interest, and HMRC will expect prompt payment once the PRs are empowered to realise assets post‑grant.

In very particular cases, taxpayers may offer heritage property in lieu of tax under the acceptance in lieu scheme where assets are of pre‑eminent national, scientific, historic, or artistic interest. While this can discharge tax liabilities, it is seldom a rapid solution for securing a grant and is not usually a practical route for initial funding.

Worked Example 1.2

The deceased’s estate consists of a house (£400,000), quoted shares (£200,000), and cash (£20,000). The IHT due is £60,000. The cash is insufficient to pay IHT. What options do the PRs have?

Answer:

The PRs can use the Direct Payment Scheme to pay IHT from the cash account. For the balance, they may:

- Arrange a loan from a beneficiary or bank, secured on the house or shares, to pay the remaining IHT.

- Elect to pay IHT by instalments on the house, paying only the first instalment before the grant is issued.

- Sell the quoted shares after obtaining the grant to repay any loan.

Worked Example 1.3

The estate includes farmland valued at £900,000, unquoted trading company shares (but not a controlling interest) valued at £120,000, and no significant cash. After exemptions and reliefs, the total IHT attributable to the farmland is £180,000 and £12,000 is attributable to the shares. The PRs elect for instalments for the farmland.

Question: What amount must be paid before the grant? Answer:

The PRs must pay the first instalment on the farmland (£18,000, being 10% of the £180,000 attributable IHT) plus the full IHT on the non‑instalment property (the £12,000 attributable to the unquoted shares that do not qualify). The total payable before the grant is £30,000, after which the grant can issue. Nine further annual instalments (with interest) remain due on the farmland.

Worked Example 1.4

PRs obtain a bank loan to pay £75,000 of initial IHT and give a first‑proceeds undertaking. After the grant, they sell quoted shares for £150,000 and repay the loan. Interest of £2,500 accrued on the loan during administration.

Question: What is the impact of the loan interest? Answer:

The interest and arrangement fees reduce the residue available for beneficiaries. Interest on a separate loan account used solely to pay IHT on personalty vesting in the PRs may be deductible in calculating the estate’s taxable income during the administration (typically for up to one year). This deduction mitigates the income tax burden but does not change the capital reduction of residue.

Consequences and Limitations

- The Probate Registry will not issue the grant until HMRC confirms that IHT due on non‑instalment property has been paid and (if elected) the first instalment on qualifying instalment property has been paid.

- Interest accrues on unpaid IHT after the statutory due date (six months after the end of the month of death); PRs should plan payments to minimise interest.

- Loans and fees reduce the estate available for beneficiaries. Undertakings to lenders must be honoured.

- If IHT is paid by instalments, interest accrues on the unpaid balance, and any disposal of the asset triggers immediate payment of outstanding IHT.

- If PRs distribute the estate before all IHT is paid, they may be personally liable for any unpaid tax. PRs should also be alert to IHT that may arise on lifetime transfers (PETs that become chargeable or chargeable lifetime transfers) discovered after death; HMRC can pursue PRs if primary obligors fail to pay.

Exam Warning: In the SQE1 exam, pay close attention to which assets qualify for the instalment option and which do not. Only certain assets (land, businesses, controlling shareholdings, some unquoted shares) are eligible. IHT on cash, quoted shares, and most investments must be paid in full before the grant is issued.

Revision Tip: Where the estate is cash‑poor, consider the Direct Payment Scheme first. If DPS is insufficient, evaluate loans (beneficiary or bank), and whether an instalment election can be used for qualifying assets. Obtain the HMRC reference (IHT422) and initiate DPS requests (IHT423) early to minimise delay.

Key Point Checklist

This article has covered the following key knowledge points:

- IHT on the death estate must generally be paid before the grant of representation is issued; this applies to the full IHT on non‑instalment assets and the first instalment on instalment assets.

- The Direct Payment Scheme allows PRs to pay IHT directly from the deceased’s bank/building society accounts using IHT423; National Savings may also pay IHT direct in appropriate cases.

- If the estate lacks sufficient liquid assets, PRs may use loans from beneficiaries or banks; interest and fees reduce residue and should be managed carefully.

- Some assets (land, businesses, controlling shareholdings, some unquoted shares) qualify for payment of IHT by instalments; only the first instalment is due before the grant, with interest accruing thereafter.

- Realising chattels and small balances may help but are usually insufficient; most securities and larger assets require the grant for sale.

- HMRC may exceptionally permit a grant on credit where it is impossible to pay IHT in advance, but this is rare and evidence‑heavy.

- PRs must ensure all IHT is paid and consider the impact of lifetime transfers becoming chargeable; premature distributions risk personal liability.

- Procedural steps and forms: IHT422 (reference), IHT400 (account), IHT421 (probate summary), IHT423 (DPS requests); excepted estates follow a simplified route with no IHT funding need.

Key Terms and Concepts

- grant of representation

- Direct Payment Scheme

- personal representatives

- instalment option