Learning Outcomes

This article outlines the core topics in wills and estate administration for SQE1, including:

- The statutory requirements for a valid will under the Wills Act 1837 and how exam questions typically test execution defects and witnessing issues.

- The meaning of testamentary capacity, how it is assessed under Banks v Goodfellow, and the evidential approach where capacity is disputed.

- The requirement for knowledge and approval, intention, and freedom from undue influence, and the consequences where these elements are challenged.

- The roles, powers, and fiduciary duties of personal representatives, distinguishing clearly between executors and administrators in SQE1 scenarios.

- The main stages in estate administration, from identifying assets and liabilities to obtaining the correct grant of representation and preparing estate accounts.

- The types of grants of representation, entitlement to each under the Non-Contentious Probate Rules, and when caveats or citations may be used.

- The statutory order for paying funeral expenses, administration costs, debts, and legacies in solvent and insolvent estates, including the impact of secured debts.

- Common pitfalls in will drafting and administration, such as gifts to witnesses, failure to deal with all assets, and premature distributions by PRs.

- The consequences of invalid wills and partial intestacy, together with the operation of survivorship and the commorientes rule.

- Available protections, remedies, and claims in estate administration, including rectification, construction, Trustee Act advertisements, Benjamin orders, and claims under the Inheritance (Provision for Family and Dependants) Act 1975.

SQE1 Syllabus

For SQE1, you are required to understand the legal framework and practical steps involved in estate administration, with a focus on the following syllabus points:

- the statutory formalities for a valid will under the Wills Act 1837

- the meaning and assessment of testamentary capacity

- the role and duties of personal representatives (executors and administrators)

- the process for collecting, managing, and distributing estate assets

- the consequences of invalid wills and intestacy

- the legal remedies and protections available in estate administration

- the different grants of representation (probate, letters of administration with will annexed, and letters of administration) and entitlement to each

- the duty of care applicable to personal representatives (Trustee Act 2000) and fiduciary obligations

- the statutory order for paying funeral expenses, testamentary and administration expenses, and debts in solvent and insolvent estates

- protections against unknown or missing claimants (Trustee Act 1925 s27, Benjamin orders) and steps to avoid personal liability

- rectification of wills, extrinsic evidence and construction issues (Wills Act 1837 s20; Administration of Justice Act 1982 s21)

- inheritance tax touchpoints and pre-grant requirements at a high level (IHT forms and the need to fund tax before grant)

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the four main formal requirements for a valid will under English law?

- Who can act as a personal representative, and what is the difference between an executor and an administrator?

- What is the test for testamentary capacity, and when must it be satisfied?

- What happens if a will is invalid or does not dispose of the whole estate?

Introduction

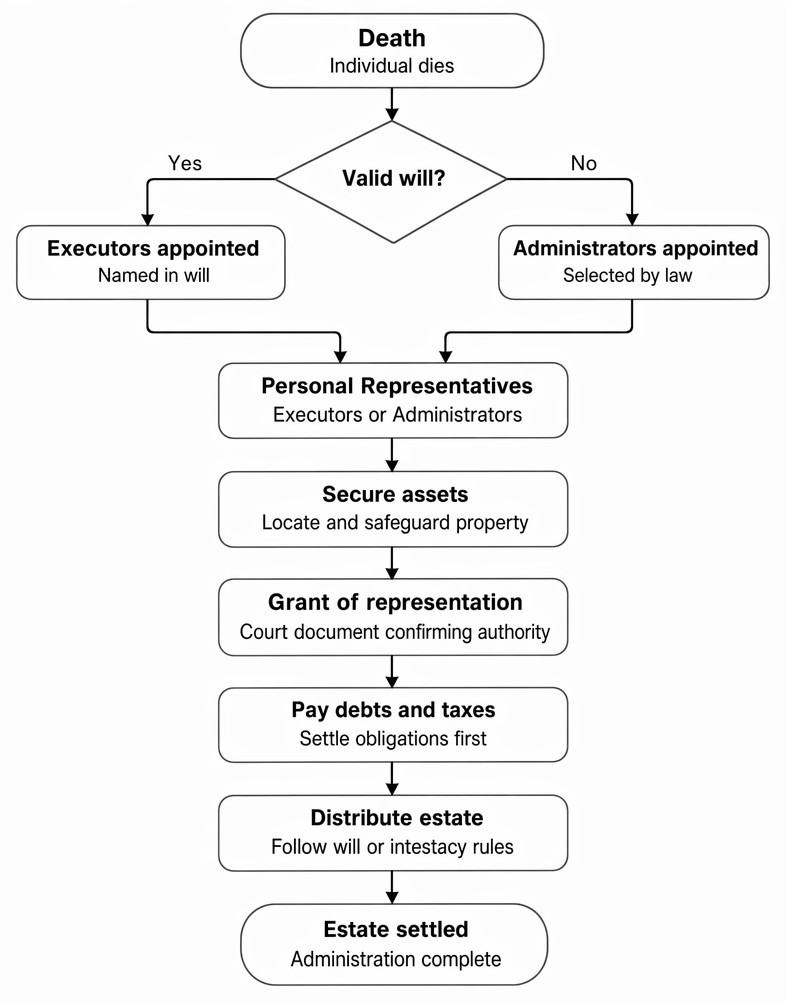

Estate administration is the legal process of managing and distributing a deceased person’s assets in accordance with their will or, if there is no valid will, under the intestacy rules. For SQE1, you must be able to identify the requirements for a valid will, understand the concept of testamentary capacity, and explain the duties and powers of personal representatives. This article provides a concise overview of these core principles and their practical application. It also addresses practical issues that commonly arise for personal representatives (PRs), such as obtaining the appropriate grant, funding inheritance tax, ordering the payment of debts, and protecting against unknown claimants.

The stages of estate administration from death to settlement, including appointment of personal representatives and distribution under a will or intestacy.

Key Term: will

A legal document by which a person (the testator) sets out how their property is to be distributed after death. Key Term: testator

The person who makes a will.Test Tip: In SQE-style questions on Overview of estate administration, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Exam Warning: Do not rely on a familiar phrase from Overview of estate administration alone; check whether the facts satisfy every condition, exception, and timing requirement.

Validity of Wills: Formalities and Capacity

A will is only valid if it complies with the statutory formalities and the testator has the necessary capacity and intention at the relevant time. In addition, the will must be interpreted against established principles, and certain defects may be remedied through rectification where appropriate.

Statutory Formalities

The Wills Act 1837 sets out the requirements for a valid will:

- The will must be in writing.

- It must be signed by the testator (or by someone else in their presence and at their direction).

- The testator’s signature must be made or acknowledged in the presence of at least two witnesses present at the same time.

- Each witness must sign or acknowledge their signature in the presence of the testator.

Key Term: attestation

The act of witnessing the testator’s signature and signing the will as a witness.

The witnesses do not need to sign in each other’s presence, but they must sign (or acknowledge their signatures) in the presence of the testator after the testator has signed or acknowledged their signature. Any person can act as a witness, but if a beneficiary or the beneficiary’s spouse/civil partner witnesses the will, the gift to that beneficiary fails (s15 Wills Act 1837); the will itself remains valid.

Practical drafting often includes an attestation clause to record compliance with formalities. Where the testator is blind, illiterate, or the will is in a language the testator cannot read, a special attestation clause is recommended to evidence that the will was read over and understood.

Key Term: attestation clause

A statement at the end of a will recording that the statutory execution requirements were observed; special forms exist for blind or illiterate testators.

A person may sign on behalf of the testator at the testator’s direction and in their presence; the witnesses must still attest. The form and placement of the signature are not rigid, but the signature must be intended to give effect to the will. If these requirements are not met, the will is invalid and the estate will be distributed under the intestacy rules.

Testamentary Capacity

The test for testamentary capacity is set out in Banks v Goodfellow (1870). The testator must:

- understand the nature of making a will and its effects

- know the extent of their property (in broad terms; exact values are not required)

- appreciate the claims of those who might expect to benefit

- not be affected by any disorder of the mind that influences their decisions

Key Term: testamentary capacity

The mental ability required to make a valid will, assessed at the time the will is executed.

If the testator lacks capacity at the time of execution, the will is invalid. Capacity is presumed unless challenged; where capacity is in doubt, contemporaneous medical evidence and careful records of instructions are advisable. The “material time” is execution, though a continuous process of planning may be relevant if the will is executed shortly afterwards and no intervening incapacity arises.

Intention

The testator must intend the document to be their will and must know and approve its contents. If the testator is unaware of the contents or is subject to undue influence, the will may be set aside. Suspicious circumstances (for example, a will drafted by or significantly benefiting the person who gave instructions) may rebut the presumption of knowledge and approval, requiring positive proof that the testator understood and agreed to the provisions.

Key Term: knowledge and approval

The requirement that the testator understands and agrees to the contents of the will at the time of execution.

Undue influence involves coercion sufficient to overbear the testator’s will; mere persuasion is insufficient. Duress, fraud, or “fraudulent calumny” (poisoning the testator’s mind against a potential beneficiary by false statements) may also defeat a will or particular gifts.

Rectification may be available if a will fails to carry out the testator’s intentions because of a clerical error or a failure to understand instructions (Wills Act 1837 s20). Ambiguities in the will can be addressed by extrinsic evidence under the Administration of Justice Act 1982 s21.

In some cases, a will may incorporate other documents “by reference” (for example, a memoranda of personal chattels), but only if the document existed at execution and is described with sufficient certainty.

Personal Representatives and Their Duties

When a person dies, their estate must be administered by personal representatives (PRs). The PRs are responsible for collecting in the assets, paying debts and liabilities, and distributing the estate to those entitled. Their duties are both fiduciary and statutory.

Key Term: personal representative (PR)

The person(s) responsible for administering a deceased person’s estate. This includes executors (appointed by will) and administrators (appointed under intestacy).

Executors and Administrators

- Executors are appointed by the will.

- Administrators are appointed by the court if there is no valid will or no executor able or willing to act.

Key Term: executor

A person named in a will to carry out the instructions of the testator and administer the estate. Key Term: administrator

A person appointed by the court to administer the estate where there is no valid will or no executor able or willing to act.

The authority of executors derives from the will and arises immediately on death. Administrators’ authority arises from the grant. Where multiple executors are named, a maximum of four can take a grant to the same estate. An appointed executor may renounce if they have not intermeddled; alternatively, “power reserved” allows a named executor to join later if needed.

PRs owe fiduciary duties to act in the best interests of the estate and beneficiaries, and a statutory duty of care under the Trustee Act 2000 s1 to act with reasonable care and skill, taking account of any special knowledge or professional status.

Key Term: executor’s year

The informal expectation that PRs will complete the core administration within 12 months of death; PRs are not bound to distribute before the end of that period (AEA 1925 s44).

PRs must avoid “devastavit” (waste or misadministration causing loss); they may be personally liable for losses resulting from breaches, though the court can relieve them if they acted honestly and reasonably (Trustee Act 1925 s61). A person who intermeddles without authority may become an “executor de son tort” and incur personal liability.

Key Term: executor de son tort

A person who, without authority, deals with estate assets as if a PR and is liable to creditors and beneficiaries to the extent of assets handled.

Main Duties

Personal representatives must:

- identify and secure all estate assets

- obtain a grant of representation (probate or letters of administration)

- pay funeral expenses, debts, and taxes

- distribute the remaining assets to beneficiaries or heirs

They should also keep estate accounts and, where appropriate, obtain professional advice (valuation, tax, investment). PRs have administrative powers akin to trustees, including powers to insure, invest (Trustee Act 2000 ss3–5), run a business, appropriate assets, advance capital (TA 1925 s32), and maintain minors (TA 1925 s31).

Key Term: appropriation

The allocation of specific assets in satisfaction of a beneficiary’s share, typically of residue; PRs can appropriate without beneficiary consent in certain circumstances, subject to safeguards.

Worked Example 1.1

Scenario: Sarah dies leaving a valid will appointing her friend Tom as executor. Her estate includes a house, savings, and personal possessions. Tom collects in the assets, pays off Sarah’s credit card debts and funeral expenses, and then distributes the remaining assets to the beneficiaries named in the will.

Answer:

Tom is acting as executor. He must follow the will’s instructions, pay debts and expenses, and distribute the estate. He is personally liable if he fails to carry out these duties properly.

Worked Example 1.2

Scenario: James dies without a valid will. His wife and two adult children survive him. His wife applies for a grant of letters of administration.

Answer:

As there is no valid will, James’s estate is administered under the intestacy rules. His wife becomes administrator and must distribute the estate according to the statutory order of entitlement.

Worked Example 1.3

Scenario: Anna is named as executor in her father’s will. She discovers that her father owed significant debts. She pays the funeral expenses and debts from the estate’s bank account before distributing the remainder to the beneficiaries.

Answer:

Anna must pay all debts and expenses before distributing the estate. If she distributes assets before settling debts, she may be personally liable to creditors.

The Estate Administration Process

Estate administration involves several key steps, each with practical considerations and legal requirements.

1. Identifying and Securing Assets

The PRs must locate and safeguard all assets belonging to the deceased, including property, bank accounts, investments, and personal belongings. They should also identify liabilities and ongoing obligations (utilities, tax, care fees). Certain assets pass outside the will or intestacy, such as:

- property owned as beneficial joint tenants (passing by survivorship)

- life assurance policies assigned or written in trust

- discretionary death-in-service pension benefits

- nominated property under statutory schemes

- trust property in which the deceased had an interest in possession (included in the IHT estate but not necessarily passing through PRs)

2. Obtaining the Grant of Representation

A grant of representation is usually required to prove the PRs’ authority to collect in assets and deal with third parties.

Key Term: grant of representation

The legal document (probate or letters of administration) confirming the PRs’ authority to administer the estate.

The appropriate grant depends on the circumstances:

- Grant of probate where there is a valid will and executors are able and willing to act.

- Letters of administration with will annexed where a valid will exists but no executor can act (for example, none appointed, predeceased, renounced, or lacking capacity).

- Letters of administration for intestacy (no valid will).

Key Term: probate

A grant issued to executors confirming their authority under a valid will. Key Term: letters of administration

A grant issued to administrators; used for intestacy or where no executor can act (with the will annexed in the latter case).

Entitlement to letters of administration follows the Non-Contentious Probate Rules 1987 (NCPR) order of priority, starting with the surviving spouse or civil partner and then issue, parents, siblings (whole blood, then half-blood), and more remote relatives; in default, the Crown may take bona vacantia.

Pre-grant procedure includes gathering information, valuing assets, and addressing inheritance tax (IHT). Excepted estates may use simplified procedures.

Key Term: excepted estate

An estate meeting criteria for reduced reporting (broadly, no IHT payable and within defined thresholds), enabling a simpler submission with the grant application.

PRs will either submit IHT205 (for excepted estates) to the Probate Registry or complete IHT400 (for chargeable estates) to HMRC. If IHT is payable before the grant, PRs can use the Direct Payment Scheme (banks/building societies pay HMRC directly) or arrange short-term funding (loan or beneficiary assistance). HMRC issues an IHT421 receipt to the Probate Registry to permit the grant.

Procedural tools include caveats (to prevent a grant, often used in disputes) and citations (to require a person to take or refuse a grant).

Key Term: caveat

A notice lodged at the Probate Registry to stop a grant issuing, typically pending a dispute or investigation. Key Term: citation

A court process compelling a person entitled to a grant to take probate/administration or renounce/refuse, enabling progress in the administration.

3. Paying Debts and Taxes

The PRs must pay the deceased’s outstanding debts, funeral expenses, and any taxes due (including inheritance tax, income tax, and capital gains tax up to the date of death) before distributing the estate.

Funeral and testamentary/admin expenses are paid first. The “statutory order” then applies to unsecured debts in a solvent estate (Administration of Estates Act 1925 s34(3), Part II Schedule 1):

- property undisposed of by will (subject to retention to meet pecuniary legacies)

- residue (subject to retention to meet pecuniary legacies)

- property specifically given for payment of debts

- property charged with payment of debts

- any fund retained to meet pecuniary legacies

- specifically devised/bequeathed property rateably by value

- property appointed under a general power rateably by value

Secured debts follow AEA 1925 s35: a beneficiary takes the asset subject to the secured debt unless the will states “free of mortgage” or otherwise shows a contrary intention. In some cases marshalling or abatement principles apply (for example, demonstrative legacies paid first from the specified fund and then from residue).

In insolvent estates, the Administration of Insolvent Estates of Deceased Persons Order 1986 sets the order of priority, broadly aligning with bankruptcy rules. PRs should not distribute anything to beneficiaries in an insolvent estate.

4. Distributing the Estate

Once debts and taxes are settled, the PRs distribute the remaining assets to the beneficiaries named in the will or, if there is no valid will, to the heirs under the intestacy rules. PRs may appropriate assets to satisfy shares, and they must ensure minors’ interests are held appropriately (often as statutory trusts).

Key Term: assent

The act by which PRs indicate that a particular asset is no longer required for administration and is transferred to the beneficiary; title passes by the will or intestacy, with the assent activating the transfer.

PRs should prepare estate accounts, obtain receipts, and take steps to protect against unknown claims before distribution.

Key Term: Benjamin order

A court order permitting distribution on the basis that a missing beneficiary is presumed dead, protecting PRs while preserving the missing person’s right to recover from recipients.

PRs can advertise under Trustee Act 1925 s27 to protect against unknown claimants.

Worked Example 1.4

Scenario: Liam’s will leaves £10,000 to his friend Nina, and the residue to his sister. Nina’s husband acts as a witness to Liam’s will. Liam dies six months later.

Answer:

The gift to Nina fails under s15 Wills Act 1837 because her spouse witnessed the will. The residue passes to Liam’s sister. The will itself remains valid.

Worked Example 1.5

Scenario: Maya’s will gives residue to her son, and a specific legacy of a painting to her daughter. The estate has insufficient residue to pay unsecured debts after funeral and administration expenses.

Answer:

Under the statutory order for solvent estates, residue bears unsecured debts before specific gifts. If residue is insufficient, PRs then apply specifically bequeathed property rateably. Unless the will directs otherwise (e.g., “free of mortgage” or contrary intention), the painting may need to be sold to meet debts.

Worked Example 1.6

Scenario: PRs cannot locate a residuary beneficiary who moved abroad 20 years ago. They have made extensive enquiries and wish to distribute to other residuary beneficiaries.

Answer:

PRs should first advertise in the London Gazette and locally under Trustee Act 1925 s27 to protect against unknown claims. For a known but missing beneficiary, they may seek a Benjamin order allowing distribution while protecting themselves. Alternatively, they may retain a reserve or obtain indemnities, though these do not fully protect PRs.

Consequences of Invalid Wills and Intestacy

If a will is invalid or does not dispose of the whole estate, the intestacy rules apply. The Administration of Estates Act 1925 and related legislation set out the order of entitlement for relatives. Cohabitants and friends have no automatic right to inherit under intestacy (though they may be able to claim under the 1975 Act if they are dependants).

Key features include:

- If there is a surviving spouse/civil partner and issue, the spouse takes personal chattels and a statutory legacy, plus a share of the remainder. If there is a spouse but no issue, the spouse typically takes the whole.

- Adopted children are treated as issue of their adoptive parents and inherit as such; modern law does not distinguish children by birth status.

- Partial intestacy can occur where only part of the estate is disposed of by the will; the undisposed part follows intestacy.

- Property passing by survivorship (beneficial joint tenancies) does not form part of the intestate estate.

- Where order of death between related persons cannot be determined, the commorientes rule presumes the older died first, affecting survivorship and entitlement.

Key Term: intestacy

The statutory regime for distributing a deceased person’s estate when there is no valid will.

Legal Challenges and Protections

Disputes Over Will Validity

A will may be challenged on grounds such as lack of capacity, undue influence, fraud, lack of knowledge and approval, or failure to comply with formalities. If a challenge succeeds, the will (or part of it) is set aside and distribution follows an earlier valid will or intestacy as appropriate.

Drafting and execution safeguards (special attestation clauses, independent advice where large gifts to a solicitor are contemplated, and careful records) reduce the risk of challenge. Ambiguities can be resolved using extrinsic evidence (AJA 1982 s21). Where a will fails to give effect to the testator’s intentions because of a clerical error or failure to understand instructions, rectification under Wills Act 1837 s20 may be ordered.

Claims Under the Inheritance (Provision for Family and Dependants) Act 1975

Certain individuals (e.g., spouses, former spouses in limited circumstances, civil partners, children, persons treated as children of the family, and dependants) can claim reasonable financial provision from the estate if the will or intestacy rules do not provide adequately for them. Applications must generally be made within six months from the date of the grant.

The court assesses claims using statutory factors (s3), including the financial resources and needs of the applicant and beneficiaries, obligations of the deceased, size and nature of the estate, any disabilities, and relevant conduct. Two standards apply: “surviving spouse” (not limited to maintenance) and the “ordinary standard” (maintenance only) for other applicants. PRs can reduce personal risk by not distributing within six months of the grant or retaining sufficient funds pending resolution.

Errors and Omissions

Mistakes in a will may be rectified by the court if they result from a clerical error or a failure to understand instructions, provided the testator’s true intentions can be established (Wills Act 1837 s20). Construction issues may permit the admission of extrinsic evidence (AJA 1982 s21). PRs can also consider post-death arrangements: disclaimers (rejecting an inheritance so it passes as though the disclaimant predeceased) and variations (redirecting entitlement), noting that variations meeting statutory conditions can be “read back” for IHT purposes (IHTA 1984 s142).

Key Term: probate

Confirms executors’ authority under a valid will; a grant is conclusive evidence of due execution and contents. Key Term: letters of administration

Confers authority on administrators; vests the estate in them to administer according to law.

Protections for PRs

To guard against unknown beneficiaries or creditors, PRs should advertise under Trustee Act 1925 s27. For missing beneficiaries, a Benjamin order can protect PRs while allowing distribution. Caveats can be lodged to prevent a grant where validity is in dispute, and citations can compel a person to accept or refuse a grant, enabling progression. PRs should maintain clear records, seek professional valuations, and document decision-making (particularly investments and asset sales) to satisfy their duty of care.

Key Term: Benjamin order

Court authority to distribute on the assumption a missing person has died, protecting PRs from later claims. Key Term: caveat

Stops a grant from issuing, typically used where validity or entitlement is disputed. Key Term: citation

Requires a person entitled to a grant to act (prove or renounce), preventing delay.

Key Point Checklist

This article has covered the following key knowledge points:

- The statutory formalities for a valid will under the Wills Act 1837, and the significance of attestation clauses.

- The test for testamentary capacity and the requirement for intention and knowledge and approval; undue influence and rectification in outline.

- The roles and duties of personal representatives (executors and administrators), including the statutory duty of care (Trustee Act 2000) and fiduciary obligations.

- The main steps in estate administration: collecting assets (including property passing outside the will), obtaining the appropriate grant, funding and paying debts and taxes, and distributing by assent and appropriation.

- The statutory order for paying expenses and debts in a solvent estate, and the position in insolvency; the effect of secured debts and “free of mortgage” directions.

- Practical protections for PRs: Trustee Act advertisements, caveats, citations, and Benjamin orders.

- The consequences of invalid wills and intestacy, including partial intestacy, survivorship, and commorientes.

- The remedies and protections available in estate administration: construction and rectification of wills, and claims under the Inheritance (Provision for Family and Dependants) Act 1975.

Key Terms and Concepts

- will

- testator

- attestation

- attestation clause

- testamentary capacity

- knowledge and approval

- personal representative (PR)

- executor

- administrator

- grant of representation

- probate

- letters of administration

- intestacy

- executor’s year

- executor de son tort

- assent

- appropriation

- caveat

- citation

- Benjamin order

- excepted estate