Learning Outcomes

This article explains nominated property and statutory nominations, including:

- what is meant by nominated property, the statutory framework for nominations, and where they commonly arise in practice

- how statutory nominations operate in contrast with testamentary gifts and intestacy, and why they cause assets to pass outside the estate

- the formal requirements for creating a valid nomination, typical scheme caps or limits, and methods for variation or revocation

- the inheritance tax consequences of nominated property, including aggregation with the estate and practical funding issues for PRs

- the treatment of nominated property under the Inheritance (Provision for Family and Dependants) Act 1975 and its inclusion in the “net estate”

- the distinction between binding statutory nominations and non-binding pension expressions of wishes in discretionary schemes

- how conflicts between nominations and wills or intestacy are resolved, including the role of express revocation clauses and statutory rules

- common validity challenges (capacity, undue influence, non-compliance with scheme rules) and the effect of lapse or disclaimer by the nominee

- application of these principles to SQE1-style problem questions, enabling accurate analysis of exam scenarios involving nominated assets and pension death benefits.

SQE1 Syllabus

For SQE1, you are required to understand the concept of nominated property and how it passes outside the estate, with a focus on the following syllabus points:

- the definition and operation of statutory nominations (especially in friendly societies, National Savings, and certain pension schemes)

- the legal effect of a valid nomination and how it differs from gifts by will or intestacy

- the requirements for making, revoking, or varying a nomination

- the treatment of nominated property for inheritance tax and estate administration purposes

- practical scenarios where nominations may conflict with a will or intestacy

- how nominated property is treated under the Inheritance (Provision for Family and Dependants) Act 1975 as part of the “net estate” available for family provision orders

- how pension “nominations” differ where trustees have discretion, and the circumstances in which benefits must be paid to personal representatives

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the effect of a valid statutory nomination on the distribution of the nominated asset after death?

- Can a nomination override a contrary provision in a later will?

- How can a nomination be revoked or changed during the nominor’s lifetime?

- Is nominated property included in the deceased’s estate for inheritance tax purposes?

Introduction

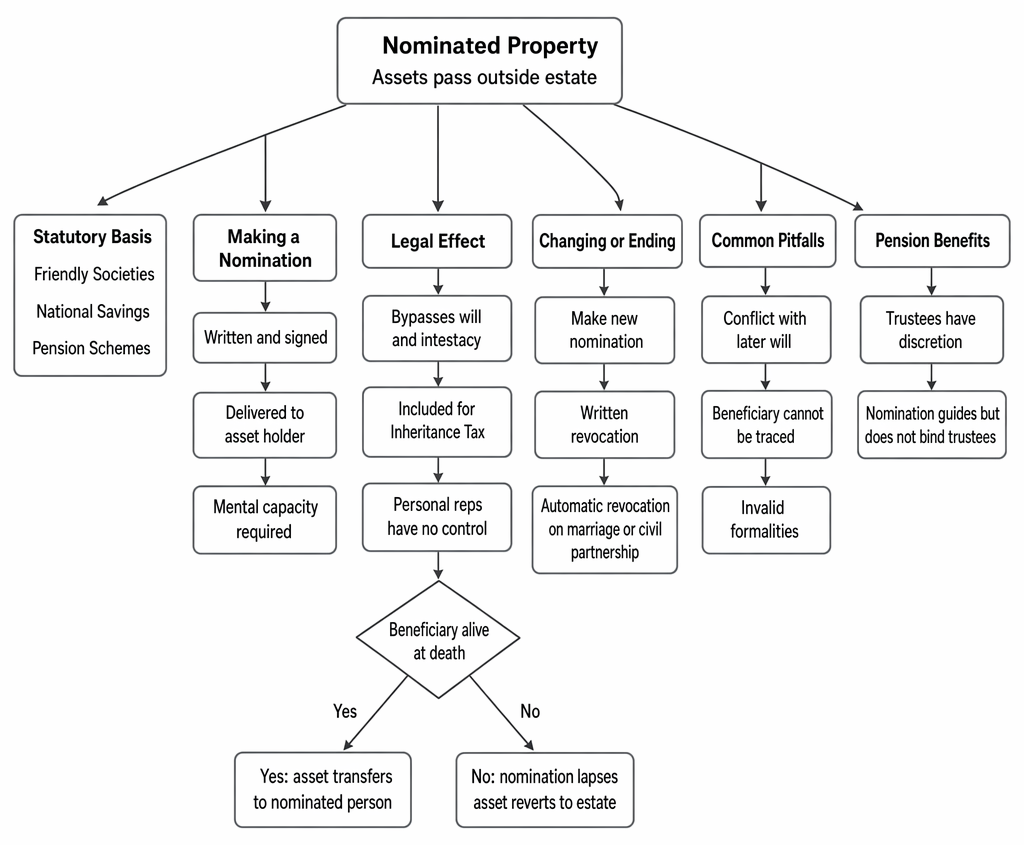

When a person dies, most of their assets pass according to their will or, if there is no will, under the intestacy rules. However, some assets are subject to a statutory nomination, which allows the owner to direct that a specific person will receive the asset on their death, regardless of the terms of any will or the intestacy rules. These assets are known as nominated property and pass outside the estate.

Nominated property passing outside the estate is summarised by reference to statutory basis, formal requirements, legal effect, revocation, and pension nominations.

Key Term: nominated property

Property that passes directly to a nominated beneficiary on death under a statutory nomination, rather than under a will or intestacy.

Nominated property is distinct from other assets that pass outside the estate for different reasons (such as survivorship on joint tenancies or proceeds of life assurance written into trust). A nomination operates because a statute or scheme rules confer a power on the owner to name a person to take the asset on death, and the institution then pays directly to that nominee.

Statutory nominations: overview

Certain statutes allow the owner of specific assets to nominate a beneficiary to receive the asset on their death. The most common examples are:

- funds held with friendly societies

- National Savings Bank accounts and certificates (including some NS&I products)

- some workplace pension schemes and death-in-service benefits

The effect of a valid nomination is that the nominated person is entitled to the asset on the owner’s death, and the asset does not fall into the estate for distribution by will or intestacy. In friendly societies and some National Savings products, scheme-specific provisions often limit the types of assets that can be nominated and may cap the value that can be transferred by nomination (statutory caps commonly apply in this sphere and have historically been set around small-asset limits—always check the up-to-date scheme rules or statutory instruments).

For pensions, it is critical to distinguish between statutory nominations that bind the administrator and non-binding “expressions of wishes.” Many modern schemes operate discretionary trusts for lump sum death benefits; they may invite a nomination but retain discretion over the payee.

Key Term: statutory nomination

A written direction made under statute by the owner of an asset, specifying who is to receive the asset on their death.

Requirements for a valid nomination

To be effective, a statutory nomination must comply with the requirements set out in the relevant statute or scheme rules. Typically, these include:

- the nomination must be in writing and signed by the owner (the nominor)

- the asset and the beneficiary must be clearly identified (e.g. account or certificate number, full name of nominee)

- the nomination must be delivered to and recorded by the society, bank, or scheme administrator (if required by the scheme)

- in some schemes, conditions relating to age, witnessing, or use of prescribed forms must be satisfied

Nominations are usually revocable and can be changed at any time before death by making a new nomination or by written revocation. In practice, the latest valid nomination on the institution’s records at the date of death will take effect. A nomination made but never received or recorded by the institution may be ineffective, even if signed and placed with the testator’s will; the scheme rules typically require lodgement with the institution.

Some institutions restrict nomination to certain products, require renewal or re-confirmation periodically, or only permit nominations up to a specified financial limit. If the asset value exceeds the cap, any excess generally passes under the will or intestacy or is dealt with under small payments provisions rather than the nomination. The precise outcome depends on the governing instrument.

Key Term: nominor

The person who owns the asset and makes the nomination.

Legal effect of a nomination

A valid nomination takes effect on the death of the nominor. The nominated property passes directly to the nominated beneficiary, outside the estate. The personal representatives have no right to the asset, and it is not available for distribution under the will or intestacy rules.

Key Term: nominated beneficiary

The person named in a statutory nomination to receive the nominated property on the nominor’s death.

If the nominated beneficiary dies before the nominor, the nomination usually lapses, and the asset will pass under the will or intestacy unless a new nomination is made. Some schemes allow substitution or naming of multiple nominees; others do not. If the nominee survives the nominor but later disclaims the benefit, the funds will be redirected according to the statutory or scheme provisions (often to the nominor’s estate or to a default payee).

Importantly, a nomination prevails even if the will has contrary terms, unless the relevant statute allows revocation by will and the will expressly revokes the nomination. In the absence of an express revocation that satisfies the statutory requirements, the nomination stands and the will cannot affect the nominated asset.

Worked Example 1.1

Amira has £4,000 in a National Savings account and makes a valid statutory nomination in favour of her friend, Leo. Amira later dies, leaving a will that leaves her entire estate to her sister.

Answer:

The £4,000 passes directly to Leo as the nominated beneficiary. It does not form part of Amira’s estate and is not available for distribution under her will.

Worked Example 1.2

Rae holds a friendly society bond which the society allows to be nominated up to a scheme cap. Rae nominates Kai to receive “the bond.” On death, the bond is worth £8,500; the scheme cap is £5,000.

Answer:

Subject to the exact scheme wording, £5,000 passes to Kai under the nomination. The remaining £3,500 is dealt with under the will or intestacy, or under the scheme’s small payments provisions if applicable. Always check the current cap and the scheme rule that governs excess amounts.

Revocation and variation of nominations

A nomination can be revoked or changed at any time before death, provided the nominor has mental capacity. Revocation is usually achieved by:

- making a new nomination (which automatically revokes the earlier one)

- giving written notice of revocation to the society, bank, or scheme administrator

A nomination is automatically revoked by marriage or civil partnership (unless the relevant statute provides otherwise), and may also be revoked by a later will if the will expressly refers to the nomination.

Divorce or dissolution of a civil partnership does not necessarily revoke a nomination; the nominor must take positive steps under the scheme to change or revoke it if they wish. Where the scheme is a pension with discretionary payment powers, changing an expression of wishes is advisable after major life events, but the trustees’ discretion remains.

A valid nomination requires capacity at the time of making; undue influence or lack of capacity may invalidate a nomination. If a nomination is successfully challenged, the asset will form part of the estate and pass under the will or intestacy.

Exam Warning: A nomination is not revoked by a later will unless the will expressly refers to the nomination or the relevant statute so provides. Always check the statutory rules and scheme documents.

Worked Example 1.3

Maya nominated her spouse under a friendly society nomination five years ago. She later enters a civil partnership with a different person, and her will leaves everything to that civil partner, stating “I revoke all previous nominations under my friendly society account.” On Maya’s death, the friendly society holds both the earlier nomination and the will clause.

Answer:

If the governing statute for the friendly society provides that marriage or civil partnership automatically revokes prior nominations, the earlier nomination is revoked by the civil partnership. Even if automatic revocation does not apply, the will’s explicit revocation of the friendly society nomination should be effective if the statute permits revocation by will. The asset will then pass under the will to the civil partner. If the statute requires revocation by notice to the society, the will clause alone may not suffice; scheme compliance is critical.

Nominated property and the estate

Although nominated property passes outside the estate for distribution purposes, it may still be relevant for other purposes:

- It is included in the estate for inheritance tax calculations where the deceased remained beneficially entitled immediately before death. The PRs must declare it on the IHT return and the value will be aggregated with other assets for IHT.

- The personal representatives may need to arrange funding to pay IHT even though nominated property does not pass through their hands. In practice, they might ask the nominee (or another beneficiary) to lend funds to the estate or consider a short-term facility with a bank or building society.

- Under the Inheritance (Provision for Family and Dependants) Act 1975, nominated property forms part of the “net estate” available for provision (section 8). The court can, where appropriate, order payment or settlement from nominated assets to meet reasonable financial provision claims.

- If the nominated property is not claimed within a certain period, it may revert to the estate under scheme rules. Many friendly societies have a long-stop claim period (often up to 10 years), but the exact period depends on the statute and scheme documents.

Worked Example 1.4

Jaspreet dies with a friendly society account of £3,000, nominated to her cousin, Sam. Sam does not claim the money for several years.

Answer:

The money remains available to Sam as the nominated beneficiary. If Sam fails to claim within the statutory period (often 10 years), the money may revert to Jaspreet’s estate and be distributed under her will or intestacy. The PRs must still include the value of the account for IHT purposes.

Worked Example 1.5

Nadia died leaving a valid nomination of £5,000 in National Savings to her partner. Her will left the rest of her estate to her adult child. The partner brings a claim under the 1975 Act alleging the will does not make reasonable financial provision.

Answer:

The nominated property forms part of the “net estate” for 1975 Act purposes and can be taken into account when the court assesses provision. If the partner is successful, the court could make an order that affects the distribution of assets within the net estate, which may include sums otherwise passing by nomination.

Practical issues and conflicts

Nominations are often overlooked or forgotten. Problems can arise if:

- the nomination is inconsistent with the will or intestacy

- the nominated beneficiary cannot be traced or has died

- the nomination is invalid due to failure to comply with statutory requirements

- the value of the asset exceeds a scheme cap, leaving an un-nominated balance that must be administered under the will or intestacy

- the nomination is out of date following marriage, civil partnership, divorce, or the birth of children

To avoid conflicts, ensure clients review nominations regularly and understand that a will does not typically revoke a nomination unless the statute allows and the will expressly revokes it. If a client intends a will to replace nominations, ensure compliance with the scheme’s revocation mechanism (often a written notice to the institution). Keep records of nominations with the will file and, where appropriate, include an express statement in the will identifying and revoking specific nominations.

Where a nominee predeceases the nominor, most nominations lapse unless a substitute nominee is provided in the scheme or statute. The asset will then fall into the estate and be distributed under the will or the intestacy rules.

Some institutions and schemes require identification documents from the nominee at claim stage; delays may occur if the nominee is abroad or difficult to contact. In such cases, PRs and beneficiaries should liaise early with the institution to confirm requirements and timelines.

Revision Tip: Always advise clients to review and update nominations when their circumstances change, and to keep a copy of the nomination with their will.

Worked Example 1.6

Olivia nominates her brother under a friendly society account. Years later, Olivia marries and dies without changing her nomination. Her will leaves all assets to her spouse. The society’s statute provides automatic revocation of nominations on marriage.

Answer:

The nomination is revoked automatically on marriage. The friendly society account does not pass to the brother; it falls into Olivia’s estate and is distributed under her will to her spouse.

Nominations and pension death benefits

Many modern pension schemes allow members to nominate a beneficiary to receive lump sum death benefits. However, the trustees or administrators of the scheme may have discretion as to who receives the benefit, and are not always bound by the nomination. Always check the scheme rules.

Common arrangements:

- Discretionary schemes: trustees have power to select a beneficiary (e.g. dependants and nominees), often guided by but not bound to a member’s expression of wishes. Payments from such schemes typically do not belong to the deceased during lifetime and pass outside the estate for succession and, in many cases, are not part of the IHT estate.

- Mandatory payment schemes: in a minority of schemes, the rules require payment to the personal representatives, making the sum part of the estate for distribution by will or intestacy and for IHT.

When advising, determine whether the pension nomination is binding or merely indicative. Where trustees have discretion, a nomination helps evidence the member’s wishes but does not create an enforceable right in the nominee. The trustees will consider the circumstances (e.g. financial dependence, family situation) and may pay to someone other than the nominated person.

Worked Example 1.7

Omar is a member of a workplace pension scheme and nominates his partner, Alex, to receive any lump sum death benefit. The scheme rules give the trustees discretion to pay the benefit to any of Omar’s dependants or nominees.

Answer:

The trustees will consider Omar’s nomination but are not legally bound to follow it. They may pay the benefit to Alex or to another dependant, depending on the circumstances and the scheme rules. Tax treatment also differs: discretionary lump sums generally fall outside the deceased’s IHT estate, whereas sums payable to the personal representatives under the scheme form part of the estate for IHT and succession.

Key Point Checklist

This article has covered the following key knowledge points:

- Nominated property is property that passes outside the estate under a valid statutory nomination.

- Statutory nominations must comply with the requirements of the relevant statute or scheme.

- A valid nomination overrides the will or intestacy for the nominated asset unless expressly revoked in accordance with the statute or scheme.

- Nominations are usually revocable and can be changed at any time before death; automatic revocation may occur on marriage or civil partnership depending on the statute.

- Nominated property is included in the estate for inheritance tax where the deceased was beneficially entitled immediately before death, even though it does not pass via the PRs for distribution.

- Nominated property is part of the “net estate” available for family provision orders under the 1975 Act.

- Scheme-specific caps may apply to nominations in friendly societies and National Savings; excess amounts are dealt with under the will or intestacy or small payments provisions.

- Pension nominations may not be binding on scheme trustees—always check the scheme rules and whether trustees have discretion or must pay the PRs.

Key Terms and Concepts

- nominated property

- statutory nomination

- nominor

- nominated beneficiary