Learning Outcomes

This article explains the SRA Accounts Rules 2019 requirements for keeping records of bills and financial transactions, including:

- Purpose and format of client ledgers, and how they link to cash books and client bank accounts

- Rules for documenting receipts, payments, transfers, and mixed receipts, with accurate double‑entry postings in the correct columns

- Process for recording, delivering, and reducing bills, maintaining a central bill record, and distinguishing profit costs from VAT

- Double‑entry (journal) postings for common SQE1 scenarios, such as billing, cash receipts, disbursements, client‑to‑business transfers, and error correction

- Five‑weekly reconciliation requirements, preparation and sign‑off of reconciliation statements, and follow‑up of unexplained differences

- How to build a reliable audit trail linking ledgers, cash books, bank statements, bills, invoices, and client instructions

- Core accounting records firms must retain, the six‑year retention period, and how to present records effectively on inspection

- Typical breaches of the Accounts Rules, exam‑relevant red flags, and practical compliance techniques to avoid common SQE1 pitfalls

SQE1 Syllabus

For SQE1, you are required to understand the record-keeping obligations imposed by the SRA Accounts Rules 2019, with a focus on the following syllabus points:

- the requirement to keep accurate, contemporaneous, and chronological accounting records for all client and business transactions

- the format and content of client ledgers and cash books

- the rules for recording bills, receipts, payments, and transfers

- the need for regular reconciliations and maintaining a clear audit trail

- the retention and accessibility of accounting records for inspection and compliance

- how to record VAT and profit costs when delivering and reducing bills, and the correct journal entries for cash receipts and transfers

- the prohibition on using a client account to provide banking facilities, and prompt correction of breaches on discovery

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What information must be included on a client ledger to ensure it is identifiable?

- How often must a firm reconcile its client account balances with bank statements under the SRA Accounts Rules 2019?

- Which records must be kept to provide an audit trail for client money transactions?

- True or false? A firm may destroy its accounting records after four years.

Introduction

Accurate record-keeping is essential for all solicitors and law firms regulated by the SRA. The SRA Accounts Rules 2019 set out strict requirements for documenting all financial transactions, including receipts, payments, bills, and transfers. These records protect client money, support regulatory compliance, and provide evidence in the event of an audit or investigation. For SQE1, you must know what records are required, how they should be kept, and the consequences of failing to maintain them. Central to these obligations are robust double‑entry bookkeeping, well‑kept client and cash ledgers, a reliable reconciliation process at least every five weeks, and a clear audit trail linking ledger entries to source documents such as bills, invoices, and bank statements.

The Purpose of Record-Keeping

The main aim of the SRA Accounts Rules is to keep client money safe and to ensure transparency in the handling of all financial transactions. Proper records allow firms to:

- demonstrate compliance with regulatory requirements

- identify and correct errors or breaches promptly

- provide a clear audit trail for all dealings with client and business money

- ensure the total of client ledger balances agrees with bank statements and the cash book, confirming client money is properly safeguarded

Key Term: audit trail

A complete and chronological record of all financial transactions, enabling the tracing of each step from initial receipt to final payment or transfer. Key Term: journal entries

The concise description of the debit and credit postings for a transaction, stating the ledgers affected and whether entries are in the client account or business account columns.

Core Record-Keeping Requirements

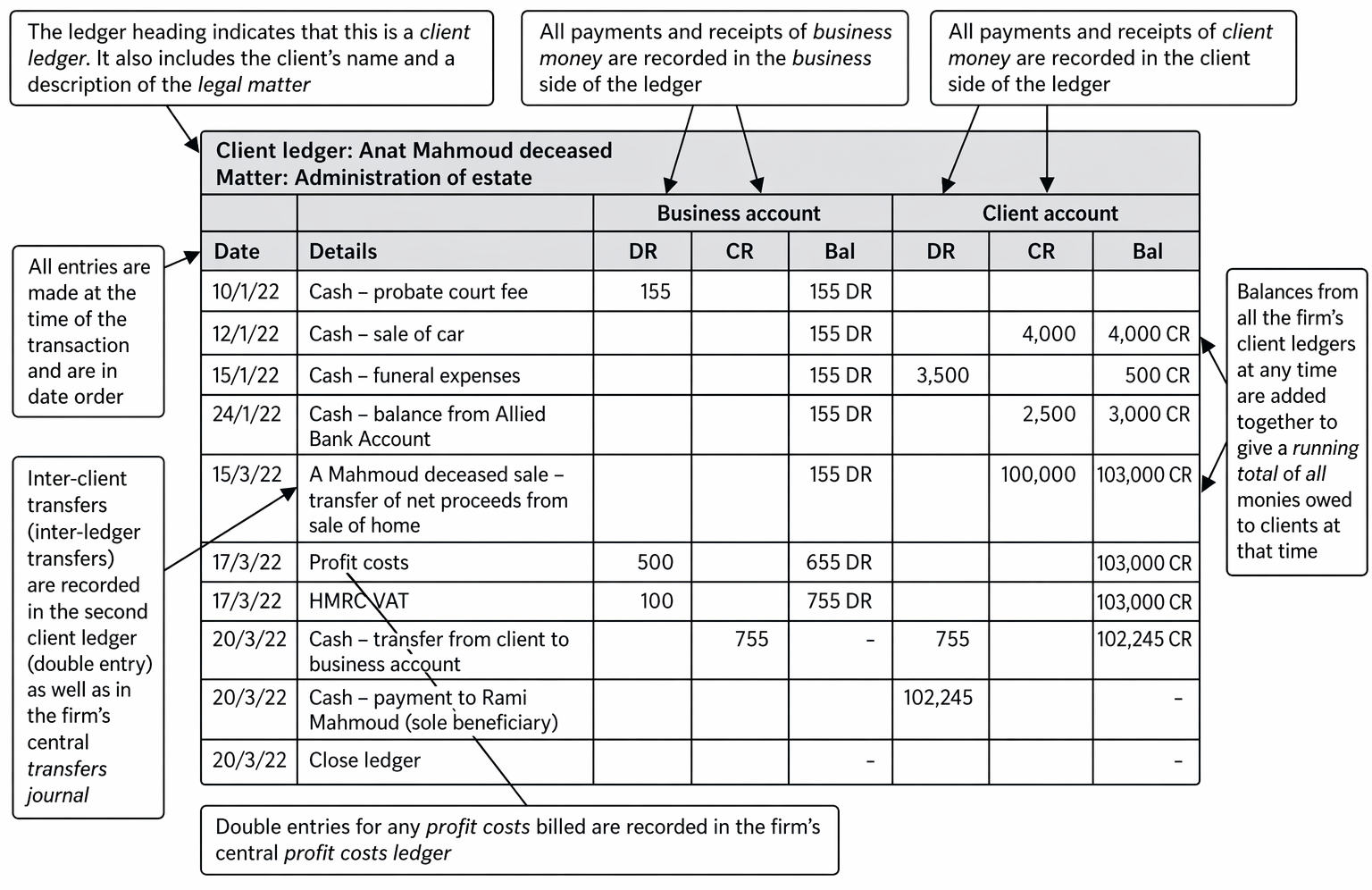

Client Ledgers

Each client (and each matter) must have a separate client ledger. This ledger records all receipts and payments of client money, as well as any business money relating to that client or matter. As a minimum the ledger should identify the client’s name, matter name/number, and show separate business and client columns with a running balance. Entries must be contemporaneous and in date order. Firms should be able to ascertain at any time the balance held for a particular client/matter and, across all client ledgers, the total owed to clients.

Office fees ledger entries presenting the opening balance, weekly fee credits and a later posting with running credit balances.

Key Term: client ledger

A record showing all financial transactions for a specific client or matter, including receipts, payments, and balances. Key Term: client account

A bank or building society account in England or Wales designated to hold client money and labelled with the firm’s name and the word “client”.

Cash Book (Cash Sheet)

Firms must keep a cash book (also called a cash sheet) for each bank account, showing all money received and paid out. The cash book must distinguish between client and business accounts. For client accounts, the balance column should always show a debit balance (the bank owes the firm funds held for clients); a credit balance would indicate an overdraft and a breach unless a narrow exception applies.

Key Term: cash book

A chronological record of all receipts and payments into and out of each bank account operated by the firm.

Recording Bills

When a bill is issued to a client, the firm must record the amount of profit costs and VAT in the business section of the client ledger. No entry is made in the cash book until the bill is paid. Under Rule 8.4, firms must also keep a central record of all bills or other written notifications of costs, readily accessible for inspection. In practice, billing requires two postings: one for profit costs and one for VAT, with corresponding credits to the profit costs ledger and HMRC‑VAT ledger.

Key Term: bill

A written notification to a client of the costs incurred for legal services, including profit costs, VAT, and disbursements. Key Term: profit costs

The firm’s professional fees charged to the client for legal services provided. Key Term: HMRC‑VAT ledger

The ledger recording VAT charged (output tax) and, where relevant, VAT paid (input tax) arising from the firm’s activities.

Receipts and Payments

All receipts and payments must be recorded promptly and accurately. For client money, the entry is made in the client ledger (client section) and the cash book (client account). For business money, the entry is made in the client ledger (business section) and the cash book (business account). The general double‑entry conventions are:

- receipts of client money: credit client ledger (client column), debit cash book (client account)

- receipts of business money: credit client ledger (business column), debit cash book (business account)

- payments of client money: debit client ledger (client column), credit cash book (client account)

- payments of business money: debit client ledger (business column), credit cash book (business account)

Where disbursements are involved, note the distinction between “agency” and “principal” treatment for VAT:

- agency method (client’s name on supplier invoice): record VAT‑inclusive payment; no VAT ledger entry for the firm

- principal method (firm’s name on supplier invoice): pay VAT‑exclusive fee from business bank, debit input tax to HMRC‑VAT ledger; recharge fee and VAT to client when billing

Transfers and Corrections

Transfers between accounts (e.g., from client to business account after a bill is paid) must be recorded in both the client ledger and the cash book. For client‑to‑business transfers, post the withdrawal from client account (debit client ledger client column; credit cash book client account) and the receipt into business account (credit client ledger business column; debit cash book business account). Inter‑client transfers (paper transfers) reallocate money between client ledgers without cash movement; record a debit in the originating client ledger and a credit in the receiving client ledger (both in client columns).

Any corrections to errors must be documented with supporting evidence. Under Rule 6.1, breaches must be corrected promptly upon discovery. Typical corrections include replacing money improperly withdrawn from client account (often by a temporary business‑to‑client transfer) and moving client funds mistakenly banked to the business account into the client account immediately, with explanatory notes and source documentation retained.

Key Term: COFA

Compliance Officer for Finance and Administration—responsible for overseeing compliance with the Accounts Rules, including reconciliation sign‑off and breach remediation. Key Term: interest payable

A business expense ledger used to record sums paid to clients in lieu of interest on client money held in a general client account.

Reconciliations and Audit Trails

Firms must reconcile their client account balances with bank statements at least every five weeks. Any discrepancies must be investigated and resolved promptly. Reconciliation should compare:

- the cash book balance for each client account to the bank statement(s)

- the aggregate of client ledger balances to the reconciled client account balance(s)

The reconciliation statement should record the date, the accounts reconciled, any reconciling items, and be signed by the COFA or a manager. Keep reconciliation records, bank statements, and related evidence with the audit trail. A robust audit trail ties ledger postings to original documents (bills, invoices, receipts), bank entries, and client instructions, allowing transactions to be traced end‑to‑end.

Key Term: reconciliation statement

The record confirming that bank statements and internal cash and client ledger balances have been compared and agree (subject to documented reconciling items) at a point in time.

Worked Example 1.1

A firm receives £2,000 from Client A for a property purchase. The money is paid into the client account. Later, the firm pays £1,500 to the seller’s solicitor and issues a bill for £400 plus £80 VAT.

Question: What records must the firm keep for these transactions?

Answer:

The firm must record the £2,000 receipt in Client A’s client ledger (client section) and the cash book (client account). The £1,500 payment is recorded as a debit in the client ledger and a credit in the cash book. When the bill is issued, £400 profit costs and £80 VAT are debited in the business section of the client ledger, with corresponding credits in the profit costs and VAT ledgers. When the bill is paid from client money, the transfer is recorded in both the client ledger and the cash book.

Worked Example 1.2

A firm delivers a bill of £600 plus £120 VAT to Client B. No payment is yet received.

Question: What double‑entry postings are required to record the bill?

Answer:

Debit the client ledger (business column) £600 for profit costs and debit the client ledger (business column) £120 for VAT. Credit the profit costs ledger £600. Credit the HMRC‑VAT ledger £120. No cash book entry is made until funds are received or transferred.

Worked Example 1.3

The firm receives a £900 bank transfer from Client B comprising £720 to settle the billed fees (£600 + £120 VAT) and £180 on account of future disbursements.

Question: How should the receipt and subsequent transfer be recorded?

Answer:

Treat as a mixed receipt paid into the client account. Record a credit of £900 in the client ledger (client column) and a debit of £900 in the cash book (client account). Promptly transfer £720 from client to business: debit client ledger (client column) £720, credit cash book (client account) £720; credit client ledger (business column) £720, debit cash book (business account) £720. Leave £180 as client money on account in the client ledger (client column).

Worked Example 1.4

On reconciliation, the bank statement shows £2,800,450 across client accounts; the aggregate of client ledger balances is £2,800,650.

Question: What action should be taken?

Answer:

Investigate the £200 discrepancy promptly, checking recent postings, uncleared items, and any miscodings. Prepare a reconciliation statement documenting reconciling items. The COFA or a manager should sign the statement and ensure any errors are corrected without delay with appropriate ledger entries and supporting evidence.

Supporting Documentation and Retention

All records must be supported by documentation such as bills, receipts, invoices, and written client instructions. These records must be kept securely for at least six years and be readily accessible for inspection by the SRA or an accountant. Retained accounting records typically include client and cash ledgers, reconciliation statements and bank statements (at least five‑weekly), central bill records, transfer journals, interest calculations and postings, and working papers explaining corrections or reconciling items. Electronic records may be maintained if they are complete, tamper‑resistant, and can be reproduced promptly in printed form.

Key Term: supporting documentation

Documents that provide evidence for financial transactions, such as bills, invoices, receipts, bank statements, and client instructions.

Accessibility and Inspection

Records must be kept up to date and in a format that allows the firm to identify at any time:

- the amount held for each client

- the purpose of each transaction

- the current balance on each client ledger

The SRA and reporting accountants have the right to inspect these records and request explanations for any entries. Accurate, timely production of the central bill record, reconciliation statements, and source documentation evidencing entries is essential. If a firm has held or received client money in an accounting period, it must obtain an accountant’s report within six months of the end of the period and deliver it to the SRA if qualified (exceptions apply where the firm handles only small balances or certain Legal Aid Agency receipts). Regardless of exemptions, the core record‑keeping duties remain in force.

Worked Example 1.5

A firm is selected for an SRA audit. The auditor asks to see the client ledger and supporting documents for a recent probate matter.

Question: What must the firm provide?

Answer:

The firm must produce the client ledger for the probate matter, the cash book entries, copies of all bills issued, receipts for payments made, and any other documents (such as client instructions or invoices) that support the transactions recorded.

Common Pitfalls and How to Avoid Them

Exam Warning: Failing to keep records up to date, omitting supporting documents, or not reconciling accounts regularly are common breaches. These can lead to regulatory action and may be tested in SQE1 scenarios.

Typical pitfalls include:

- mixing client money with business money or misposting entries to the wrong account columns

- making round‑sum withdrawals from client account without a delivered bill (contrary to the Rules)

- recording a bill but failing to post both the profit costs and VAT elements, or incorrectly posting to the cash book at billing stage

- not maintaining a central record of bills or a transfers journal

- using a client account to provide banking facilities (e.g., paying personal expenses from client funds without a legal services purpose)

- delaying the movement of mixed receipts to the correct accounts, or not correcting discovery of money banked to the wrong account immediately

- failing to reconcile at least every five weeks, or not investigating discrepancies and documenting reconciling items

- not retaining reconciliation statements, bank statements and ledger records for six years, or not producing them promptly on inspection

Practical steps:

- post entries contemporaneously and cross‑reference every ledger entry to source documentation

- implement a monthly review of client ledger balances against the cash book and bank statements (with a formal five‑weekly reconciliation and COFA sign‑off)

- maintain a central bills register, and a record of internal transfers (including inter‑client transfers)

- apply standard journal entry templates for common transactions (billing, receipts, disbursements, client‑to‑business transfers) to reduce errors

- train staff on the prohibition against banking facilities, and when to treat disbursements under agency vs principal VAT rules

- document breach corrections clearly, including explanation, supporting evidence, and corrective entries

Revision Tip: Regularly review the SRA Accounts Rules and practice preparing sample client ledgers and cash book entries to consolidate your understanding.

Key Point Checklist

This article has covered the following key knowledge points:

- Firms must keep accurate, contemporaneous, and chronological records of all financial transactions.

- Each client and matter must have a separate client ledger, showing all receipts, payments, and balances, with identifiable client/matter details.

- All receipts and payments must be recorded in the cash book for each bank account, distinguishing client and business accounts.

- Bills must be recorded in the business section of the client ledger when issued, with credits to the profit costs and HMRC‑VAT ledgers; no cash entry is made at billing stage.

- Regular reconciliations (at least every five weeks) of client account balances with bank statements are required, with COFA or manager sign‑off and prompt investigation of discrepancies.

- Supporting documentation must be retained for at least six years and be accessible for inspection.

- A clear audit trail must be maintained for all dealings with client and business money, including central bill records, transfer journals, and reconciliation statements.

- Transfers between client and business accounts must be supported by a delivered bill or written notification of costs and recorded in both the client ledger and cash book.

- Breaches (e.g., money banked to the wrong account or insufficient client funds used) must be corrected promptly on discovery, with appropriate ledger postings and evidence.

- Firms must not use client accounts to provide banking facilities; payments must relate directly to the delivery of regulated legal services.

Key Terms and Concepts

- audit trail

- client ledger

- cash book

- bill

- supporting documentation

- client account

- profit costs

- HMRC‑VAT ledger

- journal entries

- COFA

- reconciliation statement

- interest payable