Learning Outcomes

This article outlines VAT considerations in property transactions for SQE1 candidates, including:

- VAT classification of residential and commercial property transactions, distinguishing between new and existing properties, sales, premiums, and leases.

- Differences between standard-rated, zero-rated, reduced-rated, and exempt supplies, and the consequences for input tax recovery.

- Rules on the option to tax, how to identify when it has been exercised, and its impact on landlords, tenants, and buyers.

- Treatment of new and existing commercial buildings, TOGC conditions for let property portfolios, and scenarios where VAT on transfers is disapplied.

- VAT registration thresholds and tests, deregistration rules, time of supply (tax points), and core VAT invoicing and record-keeping requirements.

- Partial exemption calculations, apportionment of overheads, and cash flow implications where both taxable and exempt property supplies are made.

- Interaction of VAT with SDLT/LTT, including the effect of VAT-inclusive consideration on purchase prices, rent, and exam-style computational questions.

- Drafting and interpretation of sale and lease documentation, focusing on VAT clauses, VAT-inclusive versus VAT-exclusive pricing, and risk allocation if the contract is silent on VAT.

- Common SQE1-style pitfalls and distractors, such as assuming all property is exempt, overlooking TOGC treatment, or misreading whether VAT should be added to the agreed price or rent.

SQE1 Syllabus

For SQE1, you are required to understand the VAT implications of property transactions, including the correct VAT treatment of residential and commercial sales and leases, and the practical impact of VAT on clients, with a focus on the following syllabus points:

- The VAT treatment of residential and commercial property transactions

- The meaning and effect of zero-rated, exempt, and standard-rated supplies

- The option to tax and its consequences

- VAT recovery and partial exemption rules

- The impact of VAT on sale and lease documentation

- Practical issues for buyers and sellers, including VAT registration and cash flow

- Transfers of a going concern (TOGC) in property rental businesses

- Time of supply (tax point), VAT invoices, returns, penalties, and record-keeping

- SDLT interactions with VAT (VAT-inclusive amounts)

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following property transactions is usually zero-rated for VAT?

- a) Sale of a new residential dwelling

- b) Sale of an existing residential dwelling

- c) Lease of an existing commercial property (no option to tax)

- d) Sale of a new commercial property

-

What is the effect of a property owner exercising the option to tax on a commercial property?

-

True or false? A landlord who has opted to tax a commercial property can recover VAT on related expenses, but this may make the property less attractive to VAT-exempt tenants.

-

Which VAT rate applies to most construction services for new residential dwellings?

Introduction

VAT is a key consideration in property transactions and can have a significant financial impact for both buyers and sellers. For SQE1, you must be able to identify the correct VAT treatment for different types of property, explain the effect of the option to tax, and advise on VAT recovery and documentation issues. This article covers the essential VAT rules for residential and commercial property, including practical examples and common pitfalls.

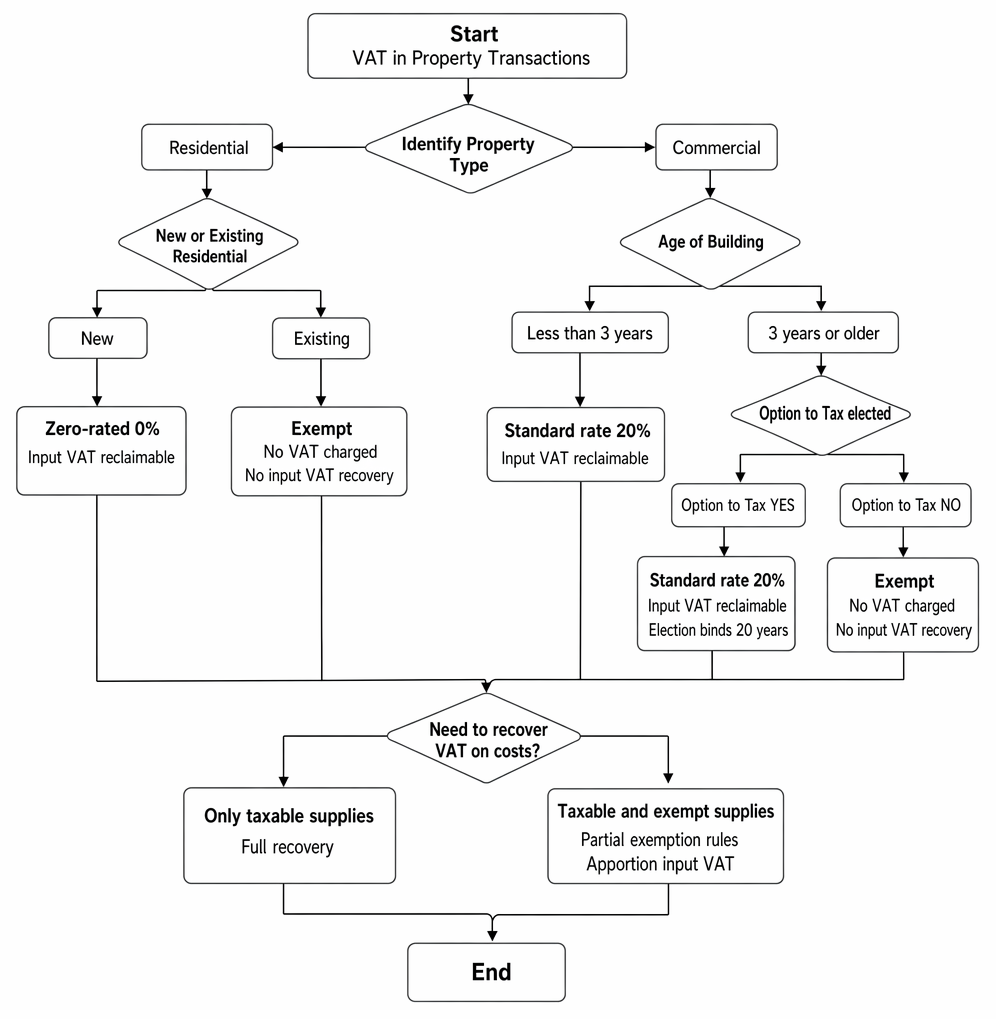

VAT treatment of residential and commercial property transactions is set out by reference to building age, option to tax, and VAT recovery.

VAT in Property Transactions: Core Principles

VAT is a tax on supplies of goods and services made in the UK by taxable persons in the course of business. The VAT treatment of property transactions depends on the type of property, the nature of the supply, and whether the supplier has opted to tax. VAT can be a substantial cost for buyers/tenants who are unable to recover input tax, and failure to handle VAT correctly in documentation can leave sellers/landlords out of pocket.

Key Term: VAT

Value Added Tax is a tax charged on the supply of goods and services in the UK by taxable persons in the course of business. Key Term: Taxable person

A person or business registered (or required to register) for VAT, usually because their taxable turnover exceeds the VAT registration threshold (£90,000 per annum from 1 April 2024, raised from £85,000; figures are updated periodically — check gov.uk/vat-registration-thresholds). Key Term: Input tax

VAT paid by a business on supplies to it (e.g. construction works, professional fees). Input tax is recoverable only to the extent it is incurred in making taxable supplies (standard-rated or zero-rated). Key Term: Output tax

VAT charged by a business on supplies it makes (e.g. rent under an opted commercial lease, sale of a new commercial building). Output tax is accounted for to HMRC, net of any recoverable input tax. Key Term: Tax point (time of supply)

The date a supply is treated as taking place for VAT accounting. For services, the basic tax point is when services are performed; earlier invoicing/payment can create an earlier tax point.

VAT Rates and Property

There are three main VAT rates relevant to property transactions:

- Standard rate (20%): Applies to most goods and services, including new commercial property and opted commercial property.

- Zero rate (0%): Applies to the first sale or long lease of new residential dwellings.

- Exempt: Applies to most sales and leases of existing residential property and most commercial property unless the option to tax has been exercised.

Key Term: Zero-rated supply

A taxable supply charged at 0% VAT. The supplier can recover input VAT on related costs. Key Term: Exempt supply

A supply not subject to VAT. The supplier cannot recover input VAT on related costs.

VAT status determines whether input tax on associated costs (construction, refurbishment, professional fees, ongoing property costs) is recoverable. Zero-rated supplies allow input tax recovery; exempt supplies do not.

Residential Property and VAT

New Residential Property

The sale or long lease (over 21 years) of a new residential dwelling is zero-rated. This allows developers to recover VAT on construction costs and professional fees. Zero-rating applies to the first grant of a major interest in the dwelling by the person constructing it. The purchaser/tenant pays no VAT on the price/premium.

Zero-rating materially affects cash flow and pricing: developers should keep robust records and VAT invoices for construction and professional services so they can reclaim input tax. If housing is built as part of a mixed-use scheme, careful planning is required to segregate costs attributable to residential (zero-rated outputs) and commercial (standard-rated or exempt outputs) elements.

Existing Residential Property

The sale or lease of an existing residential property is exempt from VAT. No VAT is charged to the buyer or tenant, but the seller or landlord cannot recover VAT on related expenses (e.g. repairs, improvements). The exemption generally covers dwellings; most private sales by individuals are not made in the course of business, but where a landlord sells a buy-to-let dwelling the supply is usually exempt (not standard-rated).

Note that certain types of short-term holiday accommodation are not exempt; they are usually standard-rated. In residential portfolios with mixed uses (e.g. some units used as holiday lets), suppliers should check whether any supplies are taxable to avoid inadvertent input tax restriction.

Construction Services

Most construction services for new residential dwellings are zero-rated. Contractors typically zero-rate supplies of construction services and building materials (incorporated) for new dwellings. Some qualifying conversions and renovations may be eligible for the reduced rate (5%), for example, converting a non-residential building into dwellings or works to long-term empty homes. Professional services (such as architects and solicitors) are generally standard-rated, but developers making zero-rated first grants can recover that input tax.

Commercial Property and VAT

New Commercial Property

The sale or lease of a new commercial property (less than three years old) is standard-rated (20%). VAT is charged on the sale price or rent. Developers and sellers benefit from input VAT recovery on construction and development costs because the output is taxable.

Existing Commercial Property

The sale or lease of an existing commercial property is usually exempt from VAT. However, the owner may choose to charge VAT by exercising the option to tax.

Key Term: Option to tax

A formal election by a property owner to charge VAT on supplies of commercial property that would otherwise be exempt. Once made, it generally lasts for 20 years and applies to future supplies of that land/building.

Opting is personal to the owner and is made on a property-by-property basis. It must be notified to HMRC (typically within 30 days of the decision). The option applies to the whole building and does not transfer with the property; a new owner must opt in their own right if they wish to charge VAT on future supplies.

Key Term: Transfer of a going concern (TOGC)

A transfer of a business (e.g. a tenanted property rental business) as a going concern, where conditions are met so that no VAT is charged on the transfer. Both parties must be VAT registered, and the buyer must opt to tax and continue the same kind of business.

Effect of the Option to Tax

If the option to tax is exercised, the supply of the property becomes standard-rated (20%). This allows the owner to recover VAT on related expenses, but may make the property less attractive to tenants or buyers who cannot recover VAT (e.g. charities, banks, insurance companies). When a landlord purchases a new commercial building, opting to tax then renting it out converts the otherwise exempt rental into a taxable supply and preserves input tax recovery on the acquisition and future costs (e.g. heating, cleaning, repairs).

Opting does not apply to residential land and buildings. A contract to construct a commercial building is standard-rated; sale of a commercial building less than three years old is also standard-rated. An option to tax can be revoked within six months if it has not been put into practice, and otherwise may be revoked after 20 years with HMRC consent.

Transfers of a Going Concern (TOGC)

Where a tenanted commercial property (new or old) is sold and the buyer will continue the property rental business, the sale can be treated as a TOGC, so no VAT is charged on the consideration if:

- Both seller and buyer are (or will be) VAT-registered at transfer

- The buyer has opted to tax (and notified HMRC) before the tax point

- The buyer intends to continue the same letting business

TOGC treatment removes the immediate VAT cost and cash flow disadvantage for buyers and avoids SDLT being calculated on a VAT-inclusive price due solely to output VAT. If TOGC conditions are not met, VAT must be charged where the output would otherwise be standard-rated (e.g. sale of a new commercial building, or sale of opted property).

VAT Recovery and Partial Exemption

A VAT-registered business making only taxable supplies (standard or zero-rated) can recover input VAT on related costs. If the business makes both taxable and exempt supplies (e.g. a landlord with both opted commercial units and non-opted exempt leases or residential lets), it must apportion input VAT using the partial exemption rules.

Key Term: Partial exemption

The method by which a business that makes both taxable and exempt supplies determines how much input VAT it can recover. Typically involves a pro-rata calculation based on taxable turnover vs total turnover, with an annual adjustment.

In practice:

- Inputs directly attributable to taxable supplies are recoverable

- Inputs directly attributable to exempt supplies are irrecoverable

- Residual inputs (overheads) are apportioned under the partial exemption method

Businesses should monitor de minimis thresholds and carry out annual adjustments. Non-business activities (e.g. purely private use) do not give rise to recoverable input tax.

VAT Registration

A business must register for VAT if its taxable turnover exceeds the registration threshold. From 1 April 2024 the threshold is £90,000 (raised from £85,000); thresholds are updated periodically and should be verified at gov.uk/vat-registration-thresholds. There are two tests, applied simultaneously:

- Historic test: has taxable turnover exceeded the threshold in the past 12 months?

- Future test: will taxable turnover exceed the threshold in the next 30 days alone?

Zero-rated and reduced-rate supplies count towards the threshold; exempt supplies do not. Voluntary registration is possible below the threshold; this allows recovery of input tax but requires charging VAT on taxable outputs. A business must cancel registration (deregister) within 30 days of stopping taxable supplies; deregistration is also permitted if taxable turnover falls below the cancellation threshold (£88,000 from 1 April 2024, raised from £83,000).

For landlords, registration is often necessary if they opt to tax (because they must charge VAT on rent and recover input tax). Businesses supplying only exempt rents cannot register and cannot recover input tax.

VAT and Documentation

The VAT status of the transaction must be reflected in the sale contract or lease. For commercial property, the contract should state whether the price is inclusive or exclusive of VAT, and whether the seller has opted to tax. Under the Standard Conditions of Sale, the price is deemed inclusive of VAT unless a special condition allows the seller to add VAT to the price. If the contract is silent and VAT is due, the seller must account for VAT out of the agreed price, reducing the net proceeds received.

Key Term: VAT invoice

A document issued for taxable supplies that includes the supplier’s VAT number, tax point, description/value of the supply, and VAT rate/amount. VAT invoices are required for input tax recovery.

Important drafting points:

- Include a special condition enabling the seller to charge VAT in addition to the price where VAT is or may be payable (e.g. sale of new commercial buildings, opted land)

- For leases, state whether rent is VAT-exclusive (if the landlord has opted to tax) and oblige the tenant to pay VAT in addition

- Consider TOGC wording where a let property is being sold and TOGC treatment is intended

- Remember SDLT: SDLT/LTT is calculated on VAT-inclusive consideration for purchases and on VAT-inclusive rent for the net present value calculation on leases. Opting to tax therefore increases SDLT/LTT liabilities.

VAT is accounted for by reference to the tax point (time of supply). Registered persons must issue VAT invoices for taxable supplies, file periodic VAT returns electronically, and keep adequate records. Failure to comply may lead to penalties and interest.

Worked Example 1.1

A developer sells a new residential flat for £300,000. What is the VAT treatment, and can the developer recover VAT on construction costs?

Answer:

The sale is zero-rated. The developer charges 0% VAT on the sale price and can recover input VAT on construction costs.

Worked Example 1.2

A landlord owns an existing office building and opts to tax. They lease the building to a VAT-registered business. What is the VAT treatment of the rent, and can the landlord recover VAT on repairs?

Answer:

The rent is standard-rated (20% VAT). The landlord can recover input VAT on repairs and related costs.

Worked Example 1.3

A charity leases an office in a building where the landlord has opted to tax. What is the impact for the charity?

Answer:

The landlord charges 20% VAT on the rent. As the charity is not VAT-registered and makes exempt supplies, it cannot recover the VAT, increasing its costs.

Worked Example 1.4

A let office building (more than three years old) is sold. Both seller and buyer are VAT-registered. The buyer will continue the letting business and has opted to tax and notified HMRC before completion. Should the seller charge VAT?

Answer:

No. The sale should be treated as a TOGC, so no VAT is charged. The buyer continues the same property rental business and meets the conditions.

Worked Example 1.5

A new commercial building is sold for £750,000. The contract is silent on VAT. The seller must charge VAT. How does this affect the seller’s net proceeds?

Answer:

If the price is silent, it is treated as VAT-inclusive. The seller must account for VAT out of £750,000. At 20%, the VAT element is £125,000, leaving net proceeds of £625,000. A special condition should have allowed VAT in addition to the price.

Worked Example 1.6

A landlord with a mixed portfolio incurs £40,000 VAT on shared overheads. Taxable turnover (opted commercial rent) is £200,000; exempt turnover (residential rent) is £300,000. How much of the residual input VAT is recoverable under a simple partial exemption apportionment?

Answer:

Apportion based on taxable vs total turnover: 200,000/500,000 = 40%. Recoverable residual input VAT is £16,000. Inputs directly attributable to taxable supplies remain fully recoverable; inputs directly attributable to exempt supplies remain irrecoverable.

Worked Example 1.7

A landlord grants a 10-year lease of an opted shop for a £100,000 premium and rent of £60,000 per year. What taxes does the tenant face on completion?

Answer:

VAT at 20% applies to both the premium and the rent (if opted). SDLT is calculated on the VAT-inclusive premium and on the VAT-inclusive rent’s net present value. The tenant faces higher SDLT because VAT is included in the consideration.

Worked Example 1.8

An owner opted to tax an office but never charged VAT on any supply. Four months later, they decide not to proceed. Can they revoke the option?

Answer:

Yes. Within six months, HMRC will revoke the option provided it has not been put into practice (e.g. no VAT-charged rent). Otherwise, revocation generally requires 20 years and HMRC consent.Exam Warning: For SQE1, always check whether the property is new or existing, residential or commercial, and whether the option to tax has been exercised. The VAT treatment depends on these factors. Do not assume all property transactions are exempt from VAT. Consider whether TOGC treatment applies. If a contract is silent, prices are deemed inclusive of VAT.

Revision Tip: If a contract is silent, the price is deemed to be inclusive of VAT. Always specify in the contract whether VAT is to be added to the price, especially for commercial property. Remember SDLT on VAT-inclusive amounts can materially increase the buyer’s cost.

Summary

| Property Type | Sale/Lease VAT Status | VAT Rate | Input VAT Recovery |

|---|---|---|---|

| New residential (first sale) | Zero-rated | 0% | Yes |

| Existing residential | Exempt | N/A | No |

| New commercial (less than 3 years old) | Standard-rated | 20% | Yes |

| Existing commercial (no option) | Exempt | N/A | No |

| Existing commercial (opted) | Standard-rated | 20% | Yes |

Where a let property business is transferred and TOGC conditions are met, no VAT is charged on the transfer. SDLT/LTT is calculated on VAT-inclusive consideration and VAT-inclusive rent where VAT applies.

Key Point Checklist

This article has covered the following key knowledge points:

- VAT treatment depends on property type (residential/commercial) and whether the property is new or existing.

- The sale or long lease of a new residential dwelling is zero-rated; existing residential property is exempt.

- The sale or lease of new commercial property is standard-rated; existing commercial property is exempt unless the option to tax is exercised.

- The option to tax allows VAT recovery on related costs but may affect the marketability of the property, particularly to VAT-sensitive buyers/tenants.

- TOGC can disapply VAT on the sale of a let property where the rental business continues and conditions are met.

- VAT-registered businesses making taxable supplies can recover input VAT; partial exemption rules apply if both taxable and exempt supplies are made.

- VAT registration uses both historic and future tests; zero-rated supplies count toward the threshold, exempt supplies do not; deregistration is available when taxable turnover falls below the deregistration threshold or taxable supplies cease.

- The VAT status must be reflected in the contract or lease; always specify whether VAT is to be added to the price or rent. Under standard conditions, a silent price is treated as VAT-inclusive.

- SDLT/LTT is calculated on VAT-inclusive amounts where VAT is charged; opting to tax can therefore increase SDLT/LTT.

- VAT accounting requires correct tax points, VAT invoices, returns, and record-keeping; penalties apply for non-compliance.

Key Terms and Concepts

- VAT

- Taxable person

- Zero-rated supply

- Exempt supply

- Option to tax

- Partial exemption

- Input tax

- Output tax

- Tax point (time of supply)

- Transfer of a going concern (TOGC)

- VAT invoice