Learning Outcomes

This article explains proprietary claims available to beneficiaries when a trustee misapplies trust property, including:

- Tracing of assets and identification of trust property in unmixed and mixed funds, and the distinction between following and tracing in an exam scenario

- Advantages of proprietary claims over personal claims, especially on trustee insolvency, and how to decide which route to plead on SQE1 problem questions

- Election between a constructive trust and an equitable lien over substitute assets, with emphasis on when appreciation or depreciation in value makes each remedy strategically preferable

- Key tracing rules and authorities—Re Hallett, Re Oatway, Roscoe v Winder, Clayton’s Case, and Barlow Clowes—and how these authorities modify presumptions about withdrawals from mixed accounts

- Application of tracing rules to common factual patterns, including mixed purchases, serial transactions, and mixed bank accounts involving multiple innocent parties

- Defences and limitations on proprietary relief, including bona fide purchaser, dissipation, inequitable result (change of position), and laches, and how these can defeat otherwise valid tracing

- Subrogation where trust money discharges secured debts, enabling beneficiaries to step into the lender’s security and rank ahead of unsecured creditors

- Proprietary claims against innocent volunteers and fairness-based constraints on recovery, focusing on when courts refuse to order sale or reversal of non-separable improvements.

SQE1 Syllabus

For SQE1, you are required to understand equitable proprietary remedies, tracing in equity, and related remedies and defences concerning trustees and third-party recipients, with a focus on the following syllabus points:

- The nature of equitable proprietary remedies.

- The availability of tracing in equity.

- Remedies against trustees and third parties.

- Third-party recipient liability and defences.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the fundamental difference between a personal claim and a proprietary claim against a trustee?

- Can beneficiaries trace trust money into an asset purchased entirely with that money if the asset has increased in value?

- What is the 'bona fide purchaser for value without notice' defence?

- True or false: If a trustee mixes trust funds with their own money in a bank account and makes withdrawals, the trustee is always presumed to spend the trust money first.

Introduction

When a trustee breaches their duty and misapplies trust property, beneficiaries may have recourse beyond simply suing the trustee personally for compensation. Equity provides powerful proprietary remedies that allow beneficiaries to reclaim the specific trust asset or property acquired with its proceeds. This article focuses on these proprietary claims, exploring the essential process of tracing and the rules applied when trust property becomes mixed with other assets. Understanding these concepts is essential for advising beneficiaries, particularly when a trustee is insolvent or the misapplied property has changed form or increased in value.

A proprietary claim is generally preferable where identifiable property or its traceable proceeds remain and the trustee’s solvency is uncertain. Unlike personal claims, proprietary relief is not subject to the ordinary six-year statutory limitation period for breach of trust; however, equitable bars such as laches and the risk of an inequitable result still apply. Tracing at equity is the mechanism that makes proprietary relief possible when the form of the trust property has changed or funds have been mixed.

Test Tip: In SQE-style questions on Understanding proprietary claims, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

The Nature of Proprietary Claims

A proprietary claim asserts ownership rights over specific property. Unlike a personal claim, which seeks monetary compensation from the trustee personally, a proprietary claim aims to recover the actual trust asset or its substitute.

Key Term: Proprietary Claim

An equitable claim asserting a beneficiary's ownership interest in specific trust property or its traceable proceeds, allowing recovery of the asset itself. Key Term: Personal Claim

A claim against a trustee personally to compensate the trust fund for losses caused by a breach of trust, satisfied from the trustee's own assets.

Proprietary claims offer significant advantages, especially if the trustee is bankrupt. A successful proprietary claim gives the beneficiary priority over the trustee's general creditors because the property identified belongs in equity to the beneficiary, not the trustee. Furthermore, if the trust property or its substitute has increased in value, the beneficiary can capture that increase through a proprietary claim. If the substitute asset has decreased, beneficiaries may prefer to secure repayment using a lien rather than taking the asset.

In this context, equity recognises two principal proprietary responses to misapplied assets:

- A constructive trust over the substitute asset, conferring an equitable proprietary interest and allowing the beneficiary to take the asset and any increase in value.

- An equitable lien (charge) over the asset to secure repayment of the misapplied amount, conferring priority but not a share in any increase in value.

Key Term: Constructive Trust (as a proprietary remedy)

An equitable response that treats the holder of the substitute asset as holding it for the beneficiary, entitling the beneficiary to take the asset and profit from any increase in value. Key Term: Equitable Lien

An equitable charge securing repayment of the misapplied trust value against the substitute asset; it gives priority over other interests in the asset but does not confer a proportionate share in any increase.

Choosing between a constructive trust and an equitable lien depends on whether the substitute has appreciated or depreciated. Equity permits beneficiaries to select the route that best protects the trust.

Tracing: Identifying Trust Property

Tracing is the process by which equity identifies what has happened to the trust property. It is not a remedy in itself but a mechanism to locate the value of the beneficiary's equitable interest, which may then be subject to a proprietary claim. Tracing can occur at common law or in equity, but equitable tracing is more flexible, particularly when funds are mixed.

Key Term: Tracing

The equitable process of identifying new assets as substitutes for original trust property that has been misappropriated or mixed with other funds. Key Term: Following

The process of pursuing the original trust asset as it passes from one person to another.

For equitable tracing, two prerequisites are generally required:

- A fiduciary relationship must exist (e.g., trustee and beneficiary).

- The claimant must have an equitable proprietary interest in the property being traced.

Additional equitable requirements are that the property is identifiable (traceable), tracing should not produce an inequitable result, and there is no undue delay in asserting the claim. These features distinguish equitable tracing from common law tracing, which usually fails when funds are mixed.

Key Term: Innocent Volunteer

A recipient who takes property as a gift or without giving value and without notice of the breach of trust; they are not personally liable but may be subject to proprietary claims unless such claims would be inequitable.

Proprietary claims rely on identifying the property (or its proceeds) in the hands of the trustee or a third party. If the property no longer exists or has been dissipated on general expenses, tracing fails; the beneficiaries must then rely on personal remedies against wrongdoing trustees or liable third parties.

Tracing into Unmixed Assets

If the trustee keeps the misapplied trust asset separate or uses trust money alone to buy a new asset (clean substitution), tracing is straightforward.

Key Term: Clean Substitution

Where trust property is directly exchanged for another asset, with no mixing of funds.

The beneficiaries can choose either to claim the substitute asset itself or to take an equitable charge (lien) over the asset to secure their personal claim for the value of the original trust property.

When a trustee holds the original trust asset intact, beneficiaries may simply follow and recover it without applying tracing rules. When the trustee holds a substitute acquired entirely with trust funds, beneficiaries may treat the substitute as trust property and elect to take it or secure repayment.

Worked Example 1.1

A trustee misappropriates £50,000 from a trust fund and uses it to buy shares in Company X solely with that money. The shares are now worth £60,000. What can the beneficiaries claim?

Answer:

The beneficiaries can trace the £50,000 into the shares. As the shares have increased in value, they should claim the shares themselves, thereby capturing the £10,000 profit for the trust. This is an example of clean substitution.

Worked Example 1.2

Assume the same facts as Example 1.1, but the shares are now worth only £40,000. What should the beneficiaries do?

Answer:

The beneficiaries should bring a personal claim against the trustee for the £50,000 loss. They can also assert an equitable lien over the £40,000 worth of shares. This means the shares can be sold, the £40,000 proceeds returned to the trust, and the beneficiaries can still pursue the trustee personally for the remaining £10,000 shortfall (though they would rank alongside other creditors for this personal claim).

Worked Example 1.3

A trustee pays £10,000 of trust money into their personal bank account, which already contains £5,000 of their own money (total £15,000). The trustee then withdraws £5,000 to buy shares, which are now worth £7,000. Subsequently, they withdraw the remaining £10,000 and spend it on a holiday (dissipated). What can the beneficiaries claim?

Answer:

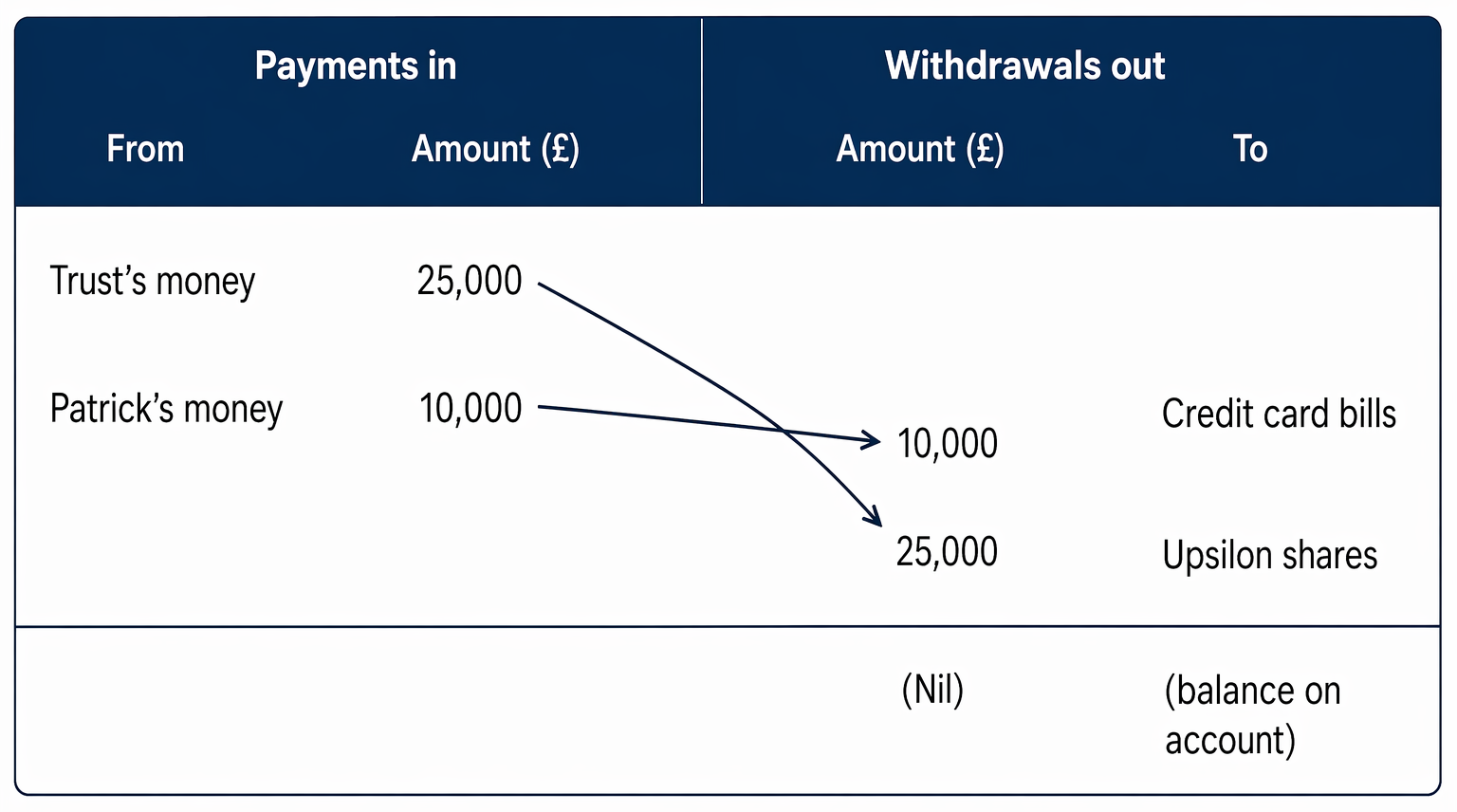

Applying Re Hallett would mean the trustee spent their own £5,000 on the shares, and the trust's £10,000 was dissipated on the holiday. This disadvantages the beneficiaries. Applying Re Oatway, the beneficiaries can assert a charge over the mixed fund and its withdrawals. They can claim the £5,000 used to buy the shares was trust money. Since the shares have increased in value, they can claim the shares themselves, now worth £7,000. The remaining £5,000 of trust money was dissipated.

Tracing into Mixed Funds

Tracing becomes more complex when a trustee mixes trust funds with their own money or with funds from another trust. Equity has developed specific rules for these situations.

Mixing Trust Funds with the Trustee's Own Money

Where trust funds are mixed with the trustee’s own money in purchasing an asset, beneficiaries can:

Trustee misapplication of trust property may generate remedies against the trustee and claims for knowing receipt, dishonest assistance, and tracing.

- Claim a proportionate share of the asset, capturing any increase in value, or

- Enforce an equitable lien for the amount of trust money used, which is often preferable if the asset has declined in value.

This election allows the beneficiaries to align the remedy with the asset’s performance. In mixed purchases, the trust’s proportion is calculated by reference to the amounts contributed.

Key Term: Pari Passu

A method of division where parties share an asset or proceeds proportionately to their respective contributions.

Withdrawals from a Mixed Bank Account

If the trustee mixes trust money with their own in a bank account and then makes withdrawals, specific rules apply to determine whose money was spent:

- Re Hallett’s Estate (1880): The trustee is presumed to spend their own money first. Any money remaining in the account (up to the value of the trust funds deposited) is presumed to be trust money.

- Re Oatway (1903): If applying Re Hallett would prejudice the beneficiary (e.g., the trustee buys an asset with the first withdrawal and dissipates the rest), the beneficiary can claim the earlier withdrawal (the purchased asset) as representing trust money to ensure recovery. This prevents a trustee from insulating valuable purchases by arguing they were funded by personal money.

Key Term: Lowest Intermediate Balance Rule

The maximum sum recoverable from a mixed bank account is capped at the lowest balance the account reached after the trust money was paid in and before any subsequent deposits intended to restore the trust funds; later deposits by the trustee do not automatically replenish the trust’s claim.

This cap from Roscoe v Winder ensures beneficiaries cannot claim more than what remained from the trust after dissipation, albeit they might still claim identifiable assets purchased while trust money remained available under Re Oatway.

Worked Example 1.4

A trustee uses £15,000 of trust money and £5,000 of personal money (total £20,000) to buy a classic car. The car is now worth £36,000. What remedies are available?

Answer:

The beneficiaries can claim a 75% proportionate share (reflecting the £15,000 contribution) of the car via a constructive trust, capturing the increase. Alternatively, they could take an equitable lien for £15,000, which is inferior here because the car’s value has risen. The trustee retains a 25% share.

Worked Example 1.5

A trustee’s personal account has £2,000. They deposit £8,000 of trust money (balance £10,000). They then spend £9,500 on general living expenses (dissipated), reducing the account to £500 (the lowest intermediate balance). A week later, they deposit £10,000 of personal money and buy a £8,000 sculpture. What can the beneficiaries recover from the account?

Answer:

The beneficiaries’ claim to the mixed account is limited by the lowest intermediate balance rule to £500. The later deposit does not replenish the trust’s claim unless clearly intended to restore trust funds. They cannot claim the sculpture using the account-based claim because the trust money had already been reduced to £500 before the sculpture purchase. If, on different facts, the sculpture had been purchased while sufficient trust money remained in the account, Re Oatway could allow a claim to the sculpture.

Mixing Funds from Two Trusts or with an Innocent Volunteer's Money

When a trustee mixes funds from two different trusts, or mixes trust funds with money belonging to an innocent third party (an innocent volunteer), the rules aim for fairness between the innocent parties.

- Mixed Asset Purchase: If funds from two trusts (or a trust and an innocent volunteer) are used to buy an asset, the beneficiaries of each trust (or the trust and the volunteer) share ownership of the asset proportionately (pari passu) to their contributions, regardless of whether the asset's value has increased or decreased.

- Mixed Bank Account:

- Clayton's Case (1816): First In, First Out (FIFO): Traditionally, the first money paid into the account is presumed to be the first money withdrawn.

- Proportionate Sharing: Courts may depart from FIFO if it is impractical or unjust, instead dividing the remaining funds or assets purchased from the account proportionately between the innocent parties (Barlow Clowes International Ltd v Vaughan (1992)).

Key Term: FIFO (First In, First Out)

A presumptive rule for mixed accounts involving multiple innocent contributors: the earliest deposit is presumed to be the first withdrawal, unless displaced for fairness.

In practice, the FIFO presumption is easily displaced where account operation is complex, beneficiaries are numerous, or strict FIFO would create arbitrary or inequitable outcomes. Courts then favour pari passu or other fair allocation methods.

Worked Example 1.6

A trustee mixes £30,000 from Trust A and £10,000 from Trust B to buy a painting for £40,000. The painting is now worth £50,000. How is ownership determined?

Answer:

Trust A and Trust B share the painting pari passu in proportion to their contributions: A has a 75% share (£37,500 of value) and B has a 25% share (£12,500 of value). Alternatively, each could take an equitable lien for the amount contributed, but the constructive trust share is preferable because the asset has increased.

Worked Example 1.7

Two trusts’ monies are mixed in a single bank account: Trust X pays in £20,000; later Trust Y pays in £30,000. The trustee then withdraws £25,000 for general expenses and later £10,000 to buy shares now worth £12,000. How should the funds be allocated?

Answer:

FIFO would treat the £25,000 withdrawal as exhausting Trust X’s £20,000 and £5,000 of Trust Y. The subsequent £10,000 withdrawal for shares would then be treated as Trust Y’s money. However, if FIFO would produce an unjust result (e.g., where withdrawals and deposits are frequent and obscure), the court can allocate pari passu. On these facts, FIFO is workable: Trust X has a personal claim for £20,000 dissipated; Trust Y can claim the £10,000 used to buy shares (and take the shares to capture the £2,000 increase). If fairness demands, the court could instead apportion the remaining balance and the shares proportionately.

Defences to Proprietary Claims

Even if trust property can be traced, a proprietary claim may be defeated by certain defences:

- Bona Fide Purchaser for Value Without Notice: A person who buys the legal title to the property for value (not as a gift), in good faith, and without actual, constructive, or imputed notice of the beneficiary's equitable interest, takes the property free from the trust. This is often termed 'equity's darling'. It bars proprietary claims to the property in their hands.

Key Term: Bona Fide Purchaser for Value Without Notice

A purchaser of the legal estate who pays value and lacks notice of any prior equitable interest; they take free of the equitable interest, defeating proprietary claims.

Notice can be actual, constructive (what a reasonable purchaser would discover from the circumstances and enquiries), or imputed (e.g., via an agent’s knowledge). Where value is not given (e.g., donees or volunteers), the defence does not apply.

- Dissipation: The claim fails if the property or its traceable product no longer exists (e.g., money spent on a holiday, general living expenses, or paying off an unsecured debt). However, if trust money is used to pay off a secured debt (like a mortgage), the beneficiaries may be subrogated to the rights of the lender.

Key Term: Subrogation

An equitable remedy that allows beneficiaries to step into the shoes of a secured creditor where trust funds discharged the secured debt, giving a charge equivalent to the lender’s former security.

- Inequitable Result: Equity will not allow tracing if it would produce an unfair result, particularly against an innocent volunteer who has changed their position based on the receipt of the property (Re Diplock). For example, tracing might be denied if an innocent volunteer used trust money for home improvements that cannot be easily separated or realised without forcing a sale of their home. In such cases, the defence of change of position may bar proprietary relief.

Key Term: Change of Position

A defence available to an innocent recipient who, in good faith, has changed their circumstances in reliance on the receipt, making it inequitable to require restoration.

- Laches (Delay): Unreasonable delay by the beneficiaries in bringing their claim, which prejudices the defendant, may bar the equitable remedy. Proprietary claims are not subject to a fixed limitation period, but equity expects timely pursuit, especially where third-party rights could be affected.

Worked Example 1.8

A trustee uses £60,000 of trust money to pay off the last tranche of a mortgage on their home. The property is in the trustee’s name. What remedy is available?

Answer:

The beneficiaries can seek subrogation to the lender’s rights, obtaining an equitable charge over the property equivalent to the discharged mortgage debt (£60,000). They cannot assert ownership of the home itself (no clean substitution), but the charge gives priority to recover the misapplied sum.

Worked Example 1.9

A trustee sells a trust-owned painting to an art dealer for £100,000. The dealer pays full market value and has no notice of the trust. Can the beneficiaries recover the painting?

Answer:

No. The art dealer is a bona fide purchaser for value without notice, taking free of the equitable interest. The beneficiaries must instead pursue a personal claim against the trustee for the loss.

Worked Example 1.10

A trustee gifts £20,000 of trust money to an elderly neighbour who, in good faith, uses it to install a wheelchair-accessible bathroom. Can the beneficiaries trace into the property?

Answer:

Likely not. The neighbour is an innocent volunteer who has changed position. Requiring reversal would be inequitable because the improvements are inseparable and a sale would be disproportionate. The beneficiaries remain entitled to personal remedies against the trustee.Exam Warning: Be careful to distinguish between the different tracing rules. The rules applied against a wrongdoing trustee (presuming against their interest) differ from those applied between innocent parties (aiming for proportionate sharing or applying FIFO). Identify the parties involved before applying the relevant rule. Additionally, do not overlook the lowest intermediate balance rule when dealing with mixed bank accounts; subsequent deposits by the trustee do not automatically restore the trust’s claim. Consider whether the beneficiaries should elect a constructive trust or equitable lien, depending on whether the asset has appreciated or depreciated. Finally, check whether a third-party recipient is ‘equity’s darling’—that will defeat proprietary relief even if tracing would otherwise identify the asset.

Key Point Checklist

This article has covered the following key knowledge points:

- Proprietary claims allow beneficiaries to recover specific trust property or its substitute, offering priority over general creditors in insolvency.

- Tracing is the process used to identify trust property or its proceeds through various transactions; it is not a remedy but a gateway to proprietary relief.

- Where a trustee mixes trust funds with their own, rules like Re Hallett (trustee spends own money first) and Re Oatway (beneficiary can claim assets purchased) apply, generally favouring the beneficiary.

- The lowest intermediate balance rule limits claims against mixed bank accounts; later personal deposits do not replenish the trust’s claim unless clearly intended to restore it.

- Where funds from two trusts or a trust and an innocent volunteer are mixed, the default rule is FIFO (Clayton's Case), but courts frequently order proportionate sharing if FIFO is unjust (Barlow Clowes).

- Beneficiaries may elect between a constructive trust (to capture increases) and an equitable lien (to secure repayment) over substitute assets.

- Proprietary claims can be defeated by defences such as the bona fide purchaser for value without notice, dissipation of the asset, the claim producing an inequitable result (change of position), or laches.

- Subrogation is available where trust money discharged a secured debt, giving beneficiaries a charge equivalent to the discharged security.

Key Terms and Concepts

- Proprietary Claim

- Personal Claim

- Tracing

- Following

- Clean Substitution

- Constructive Trust (as a proprietary remedy)

- Equitable Lien

- Lowest Intermediate Balance Rule

- Pari Passu

- FIFO (First In, First Out)

- Bona Fide Purchaser for Value Without Notice

- Innocent Volunteer

- Subrogation

- Change of Position